Technical Analysis

Samsung Electronics

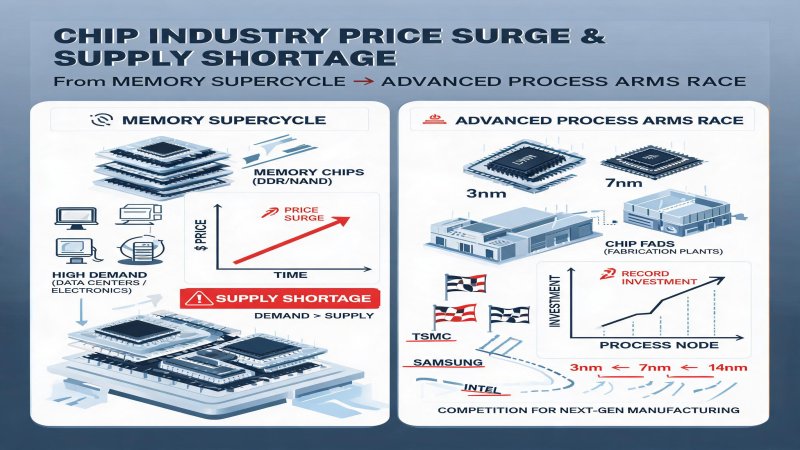

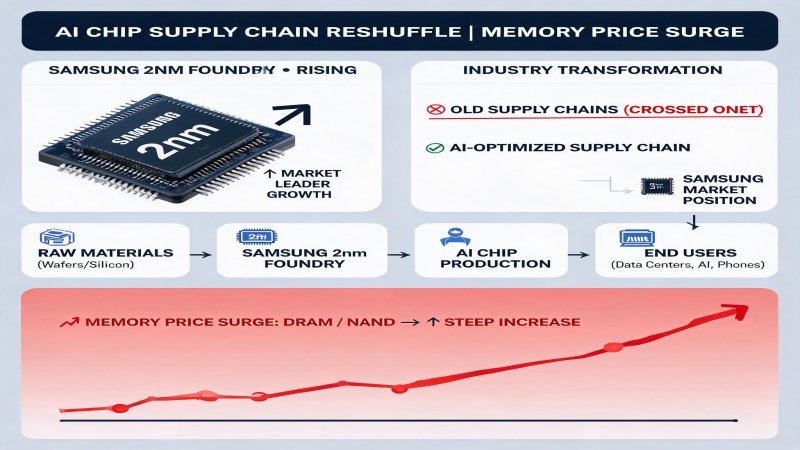

AI Chip Supply Chain Reshuffle and Memory Price Surge: Samsung's 2nm Foundry Rise and Industry Transformation

On July 3, 2026, Samsung Electronics announced up to 20% DRAM price hikes for Q3, with 4nm capacity sold out and backlog orders approaching 50 trillion KRW. Meta and Anthropic have chosen Samsung's 2nm process for custom AI chips. Intel and AMD also raised CPU/GPU prices. These events signal AI demand is fundamentally reshaping the global semiconductor supply chain, marking a strategic turning point for Samsung's foundry business.