I. Event Recap: Four Shocks in Four Days as Tech Sovereignty Battle Intensifies

Between July 3-4, 2026, four seemingly independent yet deeply interconnected news items erupted within 48 hours, collectively painting a picture of violent reshaping in the global technology industry under geopolitical pressure.

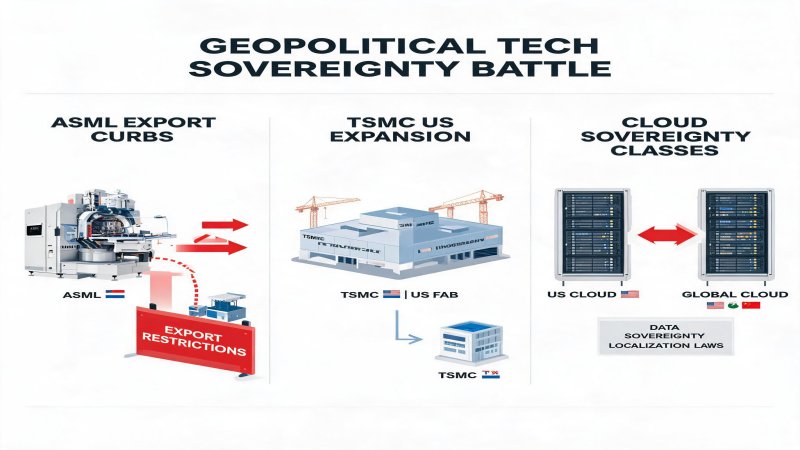

On July 4, Reuters reported that a bipartisan group of US lawmakers proposed legislation to impose new restrictions on chip manufacturing equipment exports to China. The initiative aims to prevent Chinese companies from procuring chip fabrication equipment they cannot produce domestically, preserving US leadership in artificial intelligence. ASML shares fell 2.89% in Amsterdam, after dropping 4.7% at the open. JPMorgan analysts estimated ASML could lose nearly 19% of its China revenue. China was ASML's largest market in 2025 at 33% of sales, but is expected to fall to 20% in 2026.

On July 3, Trump publicly stated that TSMC's US fab would double in scale. Taiwan's government had previously approved TSMC injecting an additional $20 billion into its US subsidiary. TSMC's US investment has expanded dramatically from the initial $12 billion, with Arizona fabs targeting 3nm and more advanced processes. While Trump's remarks carried political theater, combined with Taiwan's capital approval, they signal TSMC's US expansion has shifted from optional to mandatory.

Also on July 3, Microsoft was reported to be cutting 200-400 Azure cloud positions in China, affecting employees in Beijing and Shanghai with termination dates of July 6, 2026. The layoffs reveal the deepening conflict between Microsoft's vision of a seamless global cloud platform and China's uncompromising data sovereignty requirements. Azure China is operated by local partner 21Vianet, and Microsoft's cuts may signal transferring more operational responsibilities to this partner.

Again on July 3, Huawei's enterprise business announced that IDC data shows Huawei firewalls captured the #1 market share in China for Q1 2026. Despite sustained US pressure and Entity List restrictions, Huawei maintains domestic leadership in network security hardware, reflecting the continuous deepening of China's technology self-sufficiency drive.

The common thread is unmistakable: tech sovereignty is displacing economic efficiency as the primary determinant of global technology industry resource allocation.

II. Technical Depth: How Lithography Export Controls Reshape Global Chip Manufacturing

ASML is the world's sole EUV lithography supplier and holds dominant market share in immersion DUV lithography. JPMorgan estimates that if 65% of China equipment revenue comes from immersion DUV tools and 12.5% of installed base management revenue is tied to China immersion DUV, ASML could lose nearly 19% of China revenue.

Technically, if passed, this legislation would directly impair Chinese fabs' ability to expand advanced process capacity. Currently only SMIC has 7nm mass production capability in China, heavily dependent on ASML DUV equipment. More advanced 5nm and below theoretically require EUV, but even in the DUV realm China lacks effective domestic alternatives. SMEE's domestic lithography tools currently reach only 90nm, roughly a 15-20 year gap behind ASML.

However, export controls may also produce countereffects. Historical experience shows technology blockades often accelerate the blocked party's indigenous innovation. China already possesses strong mature process capabilities (28nm and above) and is concentrating resources on core equipment including lithography systems. While breakthroughs at EUV levels remain unlikely in the short term (3-5 years), in the DUV realm China could narrow the gap with ASML within 5-10 years through secondary equipment acquisition and accelerated domestic R&D.

Meanwhile, TSMC's US expansion raises technology transfer concerns. TSMC's Arizona fabs are planned for 3nm and more advanced processes, meaning TSMC's core process technology will be deployed on US soil. While TSMC maintains strict technology compartmentalization, long-term talent movement and technology diffusion are difficult to fully prevent.

Four-Vendor Geopolitical Risk Matrix:

| Dimension | ASML | TSMC | Microsoft Azure | Huawei |

| Direct US Control Impact | Extreme (equipment export bans) | High (forced US investment) | Medium (data sovereignty compliance) | Extreme (Entity List) |

| China Revenue Share | 33% falling to 20% | ~10-15% | ~5% | ~60% |

| Supply Chain Resilience | Low (single product dependency) | Medium (dispersed capacity) | Medium (local partner model) | High (vertical integration) |

| Technology Autonomy | Extreme (monopoly position) | Extreme (leading processes) | High (software platform) | Medium (constrained but advancing) |

| Government Subsidies/Support | EU Chips Act | US CHIPS Act + Taiwan subsidies | No significant subsidies | Strong Chinese government support |

| 3-Year Expected Change | China revenue continues falling | US capacity share rises to 15% | China team sharply reduced | Domestic share continues expanding |

III. Financial Logic: Who Bears the Cost of Controls?

Tech sovereignty battles are never cost-free. Financially, export controls, supply chain restructuring, and compliance costs are creating enormous economic burdens shared across the value chain.

For ASML, the potential ~19% China revenue loss represents roughly 6-8 billion euros in sales. While AI-driven global advanced process expansion can partially offset this (ASML just raised its 2026 revenue guidance to 36-40 billion euros), declining China revenue will directly impact its higher-margin installed base management services. The deeper concern is that losing China may impair ASML's ability to judge long-term demand growth, as China is one of the world's largest chip consumption markets.

For TSMC, the financial cost of US expansion is extraordinarily high. US fab construction costs are estimated 30-50% higher than Taiwan, driven by labor costs, construction standards, and supply chain localization requirements. TSMC previously announced $12 billion for Arizona Phase 1, plus Taiwan's approved $20 billion capital injection, bringing total investment over $32 billion. While the US CHIPS Act offers billions in subsidies, disbursement timing and amounts remain uncertain.

For Microsoft, while the Azure China layoff numbers are modest (200-400 people), the symbolism is significant. Azure China operates under a unique partner model (21Vianet), with fundamentally different commercial logic from global Azure. If Microsoft further reduces China investment, Azure China's service innovation capacity may be constrained, potentially affecting its competitiveness in China's enterprise market long-term.

For China, technological decoupling has spawned massive import substitution demand. Huawei's Q1 2026 firewall market leadership exemplifies this trend. IDC data shows China's network security hardware market growing over 15% annually, with domestic brands steadily gaining share. While this passive self-sufficiency may raise costs and create performance gaps short-term, long-term it is cultivating a parallel market independent of Western technology ecosystems.

IV. Strategic Depth: From Chips to Cloud, Tech Sovereignty Across the Full Stack

The July 3-4 events are not isolated but represent the latest manifestations of tech sovereignty battles extending across the full technology stack.

At chip manufacturing equipment, the US has constructed an export control network centered on ASML, Lam Research, and Applied Materials. The October 2022 and October 2023 control rounds already restricted key equipment for 14nm and below logic, 128-layer and above NAND, and 18nm and below DRAM. The new ASML immersion DUV proposal means controls will expand from most advanced processes to advanced processes.

At wafer manufacturing, TSMC is being forced to disperse capacity globally. Beyond Arizona, TSMC is building 28nm-12nm lines in Kumamoto, Japan, and evaluating German fabs. While this decentralization enhances supply chain resilience, it brings technology diffusion risks and management complexity. More importantly, TSMC's global layout is diluting its Made in Taiwan brand premium.

At cloud computing, data sovereignty has become legislative priority worldwide. China's Cybersecurity Law, Data Security Law, and PIPL construct the world's strictest data localization framework. The EU's Data Act and Cloud Certification Framework are pushing European cloud concepts. India, Indonesia, and other emerging markets are rolling out data localization requirements. Microsoft's Azure China layoffs are a concrete case of this global trend—when data cannot flow freely across borders, the commercial logic of a unified global cloud platform ceases to exist.

At network equipment, Huawei's case is most representative. Since its 2019 Entity List designation, Huawei has been forced to accelerate technology self-sufficiency. Its sustained firewall market leadership stems not only from technical strength but from Xinchuang (IT Application Innovation) policy promotion. China's finance, telecom, and government sectors are systematically replacing Western network equipment, creating massive substitution markets for domestic vendors.

V. Challenges and Risks: The Cost of Parallel Markets and the Fracturing of Global Innovation

While tech sovereignty battles have political rationale, they bring profound risks and challenges.

First, global semiconductor innovation efficiency is declining. The industry's decades of rapid advancement depended heavily on global division of labor—US design, Dutch equipment, Taiwan/Korea manufacturing, China packaging and testing. Forcibly fragmenting this division means each region must rebuild complete supply chains, creating massive resource waste and duplicated R&D investment. Boston Consulting Group estimates that building fully autonomous semiconductor supply chains could cost 35-65% more than globalized division of labor.

Second, standards fragmentation risk. If China and US technology camps develop independent chip architectures, operating systems, and communication protocols, global internet and digital economy interoperability faces severe threats. While this fragmentation currently mainly affects enterprise and government markets, it could spread to consumer markets long-term.

Third, uncertainty around China's technology breakthroughs. While China has strong mature process and packaging/testing capabilities, significant gaps remain in lithography, EDA software, and advanced materials chokepoint segments. If controls are too severe, they may trigger concentrated Chinese resource breakthroughs; if insufficient, they may fail to achieve desired effects. US policymakers face this dilemma.

Fourth, corporate strategic uncertainty. For multinationals like ASML, TSMC, and Microsoft, pressure to pick sides between China and the US is intensifying. Any attempt to appease both sides may alienate both. This strategic uncertainty is suppressing long-term corporate investment willingness, potentially plunging the global technology industry into a vicious cycle of low investment and low growth.

VI. Conclusion: Investment Perspective and Forward-Looking Judgments

Synthesizing the above analysis, we believe the July 3-4 events mark the global technology industry's entry into a new phase of post-globalization.

For investors, geopolitical risk has become the primary consideration in technology investing. We recommend reevaluating geopolitical Beta in portfolios: ASML, Lam Research, and equipment stocks face ongoing China revenue decline risk; TSMC faces US construction cost overruns and technology diffusion risk; Microsoft, Amazon, and other cloud providers face operational fragmentation from data sovereignty. Conversely, Chinese semiconductor equipment, materials, and EDA plays benefiting from supply chain localization, as well as Huawei ecosystem companies, may see structural opportunities.

For enterprise decision-makers, supply chain security has surpassed cost efficiency as the top priority. We recommend immediately initiating: first, mapping supply chains for critical equipment and materials to identify single-source risks; second, evaluating China+1 or US+1 diversification feasibility; third, preparing for potential technology standards fragmentation by ensuring products can adapt to different market compliance requirements; fourth, strengthening government engagement to track policy changes and secure support.

For policymakers, vigilance is needed against excessive technological nationalism. While maintaining national security and tech sovereignty is legitimate, extremism could collapse the global innovation system, ultimately harming all nations' interests. Maintaining measured competition in critical domains while preserving cooperation in non-critical areas may be the more rational choice.

Looking ahead three to five years, global technology may form two relatively independent but still intersecting ecosystems: a Western system centered on the US with European and Indo-Pacific allies, and an Eastern system centered on China with select Belt and Road countries. The two systems will likely maintain interoperability at mature processes, consumer goods, and internet application levels, but increasingly decouple in advanced processes, critical infrastructure, and militarily sensitive technologies. In this landscape, enterprises capable of navigating both systems (such as certain European and Southeast Asian players) may gain unique strategic advantages.

Why it Matters

Tech sovereignty is displacing free trade as the first principle of the global technology industry. US restrictions on ASML equipment aim to block China's access to advanced chip manufacturing capabilities. TSMC's forced core capacity relocation to the US reflects geopolitics compulsively reshaping business decisions. Microsoft's Azure China layoffs are a direct product of cloud sovereignty clashes—when data localization laws and unified global cloud visions become irreconcilable, multinationals must retrench. Meanwhile, Huawei's dominance in China's firewall market proves that technological decoupling is spawning two parallel markets.

DECISION

- Multinational CIOs: Reevaluate China cloud strategy, treat Azure China as an independent operating entity, and establish direct support channels with 21Vianet. 2. Semiconductor investors: Reduce exposure to equipment stocks with >30% China revenue dependency; increase positions in China-local equipment and materials beneficiaries. 3. Policy researchers: Track US CHIPS Act amendments and EU Chips Act implementation to anticipate next control lists. 4. Corporate compliance officers: Immediately audit China datacenter equipment supply chains, identifying alternatives and inventory buffers for restricted ASML and Lam Research equipment.

PREDICT

- Q3 2026: US China semiconductor equipment restrictions enter congressional debate, with ASML DUV export licenses to China dropping over 50%. 2. End of 2026: TSMC Arizona headcount exceeds 5,000, with US capacity share rising from 5% to 12% of total. 3. H1 2027: Microsoft Azure China operations team shrinks below 100, with 21Vianet assuming 80%+ of daily operations. 4. 2027: China's localization rate for firewalls, routers, and network equipment exceeds 75%, with Huawei, H3C, and Ruijie combining for over 80% share.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)