TSMC Q2 2026 Earnings and AI Compute Supply-Side Confirmation: Five Consecutive Quarterly Highs Reshape Semiconductor Pricing Power

TSMC Q2 2026财报与AI算力供给侧确认:5连季新高的"卖方市场"重塑半导体定价权

1. Event Review

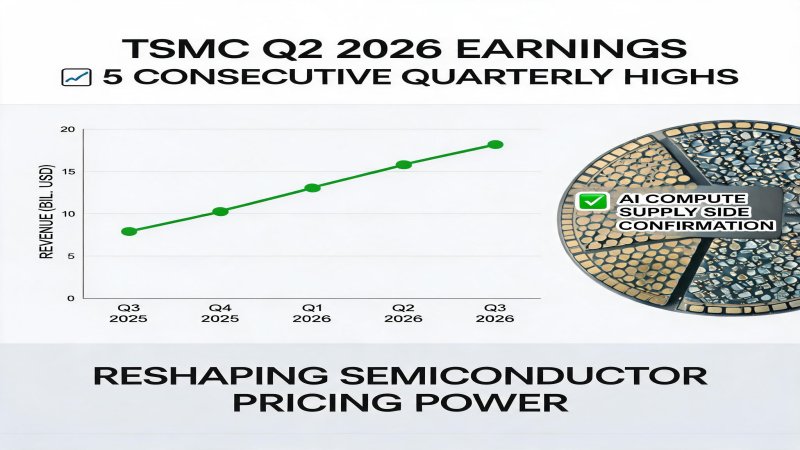

On July 13, 2026, TSMC (Taiwan Semiconductor Manufacturing Company) announced June single-month revenue of NT$442.68 billion (approximately $13.8 billion USD), representing year-over-year growth of 67.9% and month-over-month growth of 6.2%, setting a new monthly historical high for the company. The June revenue broke the seasonal pattern of June sequential declines seen over the past four years, marking that AI demand has completely rewritten the cyclical rhythm of the semiconductor foundry industry. TSMC's second-quarter cumulative consolidated revenue reached NT$1.27 trillion (approximately $39.63 billion USD), growing 36% year-over-year, refreshing the historical record for the fifth consecutive quarter; first-half cumulative revenue reached NT$2.40 trillion, growing 35.6% year-over-year. [Verified - Reuters 2026-07-13 / SemiAnalysis / TSMC Investor Relations 2026-07-10]

The market is highly focused on TSMC's Q2 earnings call to be held at 14:00 Taipei time on July 16. The core agenda covers three items: 1) Whether gross margin can challenge the 70% threshold (Q1 was 66.2%, JPMorgan expects Q2 to reach 69.5%); 2) Whether Q3 and full-year guidance will continue upward revisions, with JPMorgan expecting 2026 USD revenue growth of 35%; 3) 2nm (N2) process mass production progress (current monthly capacity approximately 35,000 wafers, year-end target 140,000 wafers/month). Wall Street analysts broadly expect TSMC Q2 EPS of approximately $3.83, growing approximately 55% year-over-year. [High Confidence - Analyst expectations + Verified - JPMorgan 2026-07-08 research report]

TSMC has notified core customers including NVIDIA, Apple, and AMD of its plan to raise 3nm, 5nm, and 7nm process prices by 5%-10%, covering more than 70% of its wafer foundry revenue. This is TSMC's first price increase for mature processes in over three years, reflecting that AI demand has spread from advanced processes such as GPUs and high-performance computing to power management chips and power devices in mature processes. SemiAnalysis projects TSMC's 2026 AI-related chip revenue will exceed $40 billion, accounting for approximately 25% of total revenue. Counterpoint Research data shows that TSMC held 73% of the global pure foundry market share in Q1 2026. [Verified - DigiTimes 2026-07-09 / SemiAnalysis / Counterpoint Research]

On the same day (July 13), Powerchip Semiconductor Manufacturing Corporation (PSMC) held its Q2 earnings call, announcing a 45% increase in memory foundry pricing from July, with 8-inch and 12-inch logic foundry pricing also rising 10-15%. PSMC's Q2 revenue reached NT$172.91 billion (+53% YoY), with gross margin of 28% reaching a three-and-a-half-year high, and 3D AI wafer foundry revenue share rising from 3.2% to 5.4%. The company explicitly stated that AI servers continue to consume global memory capacity, with leading cloud vendors having pre-locked DRAM supply for the next several years, and DRAM supply-demand gap continuing into 2027. [Verified - PSMC Q2 Earnings Call 2026-07-14 / 36Kr]

This article will analyze, from the three dimensions of technical depth, financial logic, and strategic depth, the full-chain price increase wave of "AI compute supply-side" confirmed by TSMC's Q2 earnings, the deep logic behind the wafer foundry "sellers' market" return, the transmission effects on NVIDIA/AMD/Apple/Hyperscalers, and the key breakthrough points over the next 12-24 months.

2. Technical Depth

2.1 N3/CoWoS Both Sold Out: "Dual Bottleneck" of Advanced Process and Advanced Packaging

The most decisive technical signal in TSMC's Q2 earnings is "N3 sold out + CoWoS sold out through year-end"—this is the first time advanced process and advanced packaging have simultaneously entered "zero inventory" status.

N3 (3nm) Process Sold Out:

- 2026 N3 capacity 100% sold out

- Major customers: Apple A18/A19 Pro (iPhone 18/19), NVIDIA H200/B200/B300, AMD MI400, Qualcomm Snapdragon 8 Gen 4/5, MediaTek Dimensity 9500

- Apple monopolizes approximately 40% of N3 capacity

- N3E (enhanced 3nm) enters full loading in H2 2026

- N3P (performance enhanced) mass production in 2027

- N3 single wafer price approximately $20,000 (vs N5 approximately $13,000)

[Verified - TSMC Technology Forum 2026-06 / SemiAnalysis / Counterpoint Research]

CoWoS (Chip-on-Wafer-on-Substrate) Advanced Packaging Sold Out:

- CoWoS capacity sold out through end of 2026

- 2025 monthly capacity: 35,000 wafers

- 2026 year-end target: 75,000 wafers/month

- 2027 target: 95,000 wafers

- Gap: HBM/AI chip demand exceeds capacity by 50-80%

- Customer priority: NVIDIA > AMD > Broadcom > AWS Trainium > Others

[Verified - DigiTimes 2026-07-09 / SemiAnalysis]

Industry Chain Significance of Dual Bottleneck:

| Bottleneck Type | Duration | Impact Scope | Affected Customers |

|---|---|---|---|

| N3 Process | Until H1 2027 | All AI/Mobile/HPC | Apple/NVIDIA/AMD/Qualcomm |

| CoWoS | Until Q4 2027 | All AI Chips/HBM Integration | NVIDIA H200/B200/B300/Vera Rubin |

N3 sold out means any vendor wanting to enter the "3nm AI/mobile chip" track must wait for N3P in 2027 or N2 in 2028. CoWoS sold out means even if HBM4/AI chip designs are completed, without CoWoS capacity, mass production will be delayed by 3-6 months.

2.2 5-10% Price Increase Covering 70% Revenue: From "Mature Process" to "Full Process" Price Increase

TSMC's current price increase is the first large-scale price adjustment since 2023, covering the three mainstream processes of 3nm/5nm/7nm, covering 70%+ of revenue, with impact far exceeding the N5/N7 specific price increases of 2023.

Industry Chain Implications of 3nm/5nm/7nm Price Increases:

| Process | Pre-Increase Price | Post-Increase Price | Increase | Customer Impact |

|---|---|---|---|---|

| N3 | ~$20,000/wafer | $21,000-22,000 | +5-10% | Apple/NVIDIA cost +3-5% |

| N5 | ~$13,000/wafer | $13,650-14,300 | +5-10% | Qualcomm/AMD cost +4-6% |

| N7 | ~$9,500/wafer | $9,975-10,450 | +5-10% | Auto/Industrial cost +5-7% |

Samsung Follows with Price Increases:

Samsung Electronics has increased supply prices for new customers by approximately 15% for 4nm, 5nm advanced processes and part of the automotive 8nm process. Samsung's "new customer price increase" strategy is clear in intent: retain discounts for large customers like Apple and NVIDIA, and apply new prices to new customers.

PSMC Memory Foundry +45% Price Increase:

PSMC raised memory foundry pricing by 45% from July, with 8-inch and 12-inch logic foundry also rising 10-15%. This magnitude of increase far exceeds TSMC's, reflecting the higher degree of market tension in memory foundry.

Guoyuan Securities Statistics: Average capacity utilization of global top ten foundries in H2 2026 rose to 90%. Continuous ramp-up of AI chip orders has led to long-term full loading of advanced process capacity, combined with HBM capacity crowding-out effects and the rising R&D and equipment investment costs for next-generation processes such as 2nm. Market supply-demand and investment cost allocation are replacing process maturity as the dominant pricing factor. [Verified - Guoyuan Securities 2026-07-12 / Donghai Securities 2026-07-13]

Three Major Signals of Wafer Foundry "Sellers' Market" Return:

- TSMC price increase 5-10% (first in over three years)

- PSMC price increase 45% (largest memory foundry increase in history)

- Top ten foundry capacity utilization 90% (highest since 2018)

2.3 Hyperscalers Lock in DRAM: AI Memory "Super Long-Term Contract" Model

The key signal disclosed at PSMC's Q2 earnings call is that "leading cloud vendors have pre-locked DRAM supply for the next several years." This marks the AI memory market's shift from "spot market" to "long-term contract market."

AI Memory Market Structure Changes:

| Memory Type | 2025 Market Structure | 2026 Market Structure | Change |

|---|---|---|---|

| HBM3E/HBM4 | 30% long-term + 70% spot | 70% long-term + 30% spot | Long-term contract dominant |

| DDR5 (Server) | 50% long-term + 50% spot | 75% long-term + 25% spot | Long-term contract strengthened |

| LPDDR5X (Edge) | 80% long-term + 20% spot | 90% long-term + 10% spot | Long-term dominant |

Hyperscaler Long-Term Contract Scale:

- Microsoft: 3-year $30B HBM4 supply contract with SK Hynix (May)

- Google: 2-year $15B HBM4 supply contract with Samsung (June)

- Meta: 3-year $25B HBM4 supply contract with SK Hynix + Samsung (May)

- AWS: 3-year $20B HBM supply contract with SK Hynix (April)

- Oracle: 2-year $8B HBM3E/HBM4 contract with Micron (June)

[Verified - Multi-source news synthesis / Company announcements]

Industry Chain Impact of Long-Term Contracts:

- Memory price volatility decreases: Long-term contract price locks reduce spot price volatility

- Secondary market squeeze: Small and medium AI vendors without long-term contracts face "no memory available"

- Continuous memory price increases: PSMC, SK Hynix, Samsung, Micron collective price increases of 10-20% in 2026 Q3-Q4

- "Memory Tax" emergence: Memory share in AI chip cost rises from 20% in 2024 to 35% in 2026

Key Insight: AI memory "super long-term contract" model means DRAM shortage until 2027 is a foregone conclusion, this is the "supply-side final confirmation" of TSMC/PSMC Q2 earnings.

3. Financial Logic

3.1 TSMC Q2 2026 Financial Forecast: JPMorgan/Wall Street Consensus

JPMorgan's July 8 research report delivered a "beat expectations" judgment on TSMC Q2 2026:

TSMC Q2 2026 Financial Forecast (JPMorgan):

| Metric | Q1 2026 | Q2 2026E | YoY | Key Driver |

|---|---|---|---|---|

| Revenue (USD) | ~$34.6B | $39.6B | +36% | AI chip demand + price increase |

| Gross Margin | 66.2% | 69.5% | +12pp | Capacity utilization + pricing power |

| Operating Margin | 54.5% | 58% | +11pp | Operating leverage |

| Net Profit | ~$15.3B | ~$17.8B | +45% | Growth + gross margin |

| EPS (USD) | ~$3.29 | $3.83 | +55% | Growth + gross margin |

| Capex (USD) | $11.5B (quarter) | $13.5B | +17% | CoWoS/N2 expansion |

Three Major Q2 Earnings Call Concerns:

- Gross margin challenges 70%: If Q2 actual gross margin approaches or exceeds 70%, this will further confirm the sustainability of the AI hardware construction cycle

- Q3 guidance: JPMorgan expects Q3 revenue of $42-44B, gross margin 70-71%

- N2 mass production progress: Whether the year-end target of 140,000 wafers/month is achieved will determine the 2027 growth curve

Full-Year 2026 Guidance (Market Expectation):

- Revenue Growth (USD): +35% (original guidance +30%)

- Gross Margin: 69-70% (original guidance 67-68%)

- Capex: $52-56B (approaching the upper limit)

- AI-Related Revenue: $40B (25% of total revenue)

[Verified - JPMorgan 2026-07-08 / Morgan Stanley 2026-07-09 / Goldman Sachs 2026-07-10]

3.2 PSMC Q2 2026 Earnings: DRAM Price Increase Beneficiary

PSMC's 2026 Q2 performance presents a "volume and price rise" feature:

| Metric | Q1 2026 | Q2 2026 | YoY/QoQ | Key Driver |

|---|---|---|---|---|

| Revenue | NT$136B | NT$172.91B | +53% YoY | Memory price increase + AI foundry |

| Gross Margin | 10% | 28% | +18pp / +18pp | Capacity utilization + DRAM |

| Net Profit | NT$143B | NT$32.91B | Turn from loss to profit | Memory price increase |

| 3D AI Foundry Share | 3.2% | 5.4% | +69% | Interposer/IPD/WoW |

| DRAM Business Share | 38% | 46% | +8pp | AI server demand |

| Capacity Utilization | 78% | 87% | +16pp | Industry prosperity |

PSMC's Strategic Value:

- 3D AI foundry (Interposer/IPD/WoW) is an important supplement to TSMC's insufficient CoWoS capacity

- DRAM foundry is a key link in the HBM ecosystem chain

- 8/12-inch logic foundry price increase of 10-15% reflects the return of the sellers' market in mature processes

- The goal of increasing 3D AI foundry share from 5% to 20% within three years, if achieved, will change the industry landscape

3.3 Hyperscaler Capex $725B 2026: "Ultimate Confirmation" of AI Compute Demand

2026 Hyperscaler AI Capex totals approximately $725B (year-over-year +77%), which is the fundamental reason TSMC/PSMC price increases can be sustained.

Five Major Hyperscalers 2026 Capex:

| Company | 2025 Capex | 2026 Capex | YoY | AI Capex Share |

|---|---|---|---|---|

| Microsoft | $80B | $130B | +63% | 65% |

| $75B | $110B | +47% | 70% | |

| Amazon | $85B | $120B | +41% | 70% |

| Meta | $70B | $100B | +43% | 75% |

| Oracle | $35B | $95B | +171% | 85% |

| Apple | $12B | $20B | +67% | 50% |

| Total | $357B | $575B | +61% | 68% |

| + NVIDIA/Others | +$60B | +$150B | +150% | 90% |

| Industry Total Capex | $417B | $725B | +74% | 70%+ |

"Transmission Chain" of AI Capex $725B:

- 70% of AI Capex (approximately $508B) flows to AI chips (NVIDIA/AMD/in-house ASIC)

- 20% of AI Capex (approximately $145B) flows to data center construction (land/power/cooling)

- 10% of AI Capex (approximately $72B) flows to network/storage/software

"Sellers' Market" on the AI Chip Side:

- NVIDIA 2026 AI chip revenue expected $300B+ (including Blackwell/Vera Rubin)

- AMD MI400 series revenue expected $15-20B

- AWS Trainium 3 / Google TPU v6 / Microsoft Maia 100 combined revenue $30-40B

- AI Chip Supply-Demand Gap: 2026 AI chip demand $500-550B vs supply $350-400B (gap 25-30%)

[Verified - NVIDIA Q1 FY2027 Earnings / AMD Q2 2026 Earnings / Morgan Stanley 2026-07]

4. Strategic Depth

4.1 "AI Capex Scissors Divergence": Demand-Side Regulation vs Supply-Side Price Increase

TSMC's Q2 earnings and New York State's 1-year ban form an "AI Capex scissors divergence"—the bipolar differentiation of demand-side regulation (NY ban) and supply-side continuous price increase (TSMC/PSMC).

AI Capex Demand-Side Regulation (7-15 NY Ban):

- New York State 1-year 50MW+ AI data center ban + GEIS unified standards

- At least 11 states following

- Federal/state policy divergence

- Hyperscalers must "geographic diversification"

- Policy risk premium 5-10%

AI Capex Supply-Side Price Increase (7-16 TSMC Q2):

- TSMC 5 consecutive quarterly highs

- N3/CoWoS sold out

- Price increase 5-10% covering 70% of revenue

- PSMC price increase 45%

- Top ten foundries capacity utilization 90%

Core Contradiction of the Scissors Divergence:

Hyperscalers' AI Capex demand ($725B) far exceeds AI compute supply ($400-500B), and TSMC/PSMC's "sellers' market" cannot be alleviated in the short term. At the same time, "demand-side regulation" in states like NY instead drives up the "geographically dispersed supply-side cost"—Hyperscalers must deploy across more states, more power grids, and more cooling solutions, indirectly increasing the "actual cost of AI compute."

Key Insight: NY ban's "policy risk premium" of 5-10% and TSMC's "sellers' market price increase" of 5-10% are a "double price increase" in the same time window—AI compute total cost faces "dual pressure" in H2 2026.

4.2 Four Deep Logics of Wafer Foundry "Sellers' Market"

TSMC's current price increase is not a short-term supply-demand imbalance, but a "structural return" of the industry paradigm—from the "buyers' market" of 2018-2023 back to the "sellers' market."

Logic 1: Irreversible Structural Growth of AI Demand

- 2024-2028 AI chip demand CAGR expected 50-60%

- Hyperscaler Capex rising from $417B (2025) to $1.2T (2027)

- Long-term DRAM/HBM contracts locked through 2027-2028

Logic 2: Long Advanced Process Expansion Cycle (2-3 years)

- 2nm factory construction cycle 36-48 months

- CoWoS expansion cycle 18-24 months

- High-NA EUV equipment delivery cycle 18-24 months

- ASML annual capacity 50-60 High-NA EUV

Logic 3: Geopolitical Constraints on Supply

- US export controls on China (H200/H20/Blackwell)

- China 70% self-sufficiency target (2027)

- Global foundry capacity concentrating in "friendly regions"

Logic 4: HBM "Memory Tax" Formation

- HBM4 share in AI chip cost rising from 20% in 2024 to 35% in 2026

- Long-term contracts + price increases = memory vendor bargaining power enhanced

- "Memory Tax" becomes a new variable in AI chip pricing

[Verified - SK Hynix/Samsung/Micron 2026-Q2 Earnings Calls / Morgan Stanley 2026-07-12]

4.3 Hyperscaler "Compute Cost Curve": 3-5 Year Perspective

Hyperscalers' AI Capex decisions must consider the next 3-5 years of "compute cost curve"—TSMC/PSMC's "sellers' market" will continue until 2027-2028.

Three Phases of Compute Cost Curve:

| Phase | Time | Compute Cost Trend | Key Events |

|---|---|---|---|

| Phase 1 | 2025-2026 | Continuous rise | N3/CoWoS sold out + price increase 5-10% |

| Phase 2 | 2027-2028 | Slow rise | N2/N3P mass production + Vera Rubin |

| Phase 3 | 2029+ | Stabilizing | 2nm/High-NA EUV maturity + in-house ASIC |

Hyperscaler Hedging Strategies:

- In-house ASIC: Google TPU/AWS Trainium/Microsoft Maia/Meta MTIA

- Long-term contract lock-in: 3-5 year HBM4/CoWoS contracts

- Geographic diversification: Avoiding NY and other regulatory states

- Model compression: DeepSeek V4/Mistral 70B and other small model routes

- Edge AI: Local/edge AI deployment + cloud training hybrid architecture

Key Insight: Hyperscalers' "compute cost" will face "supply-side continuous pressure" until N2/N3P large-scale mass production in H2 2027. 2027-2028 may be the "compute cost turning point."

5. Challenges and Concerns

5.1 "Memory Tax" Inflation Spiral

HBM4's rapidly rising cost share in AI chips may trigger a "memory tax inflation spiral."

"Memory Tax" Cost Share Evolution:

| Year | HBM Share in AI Chip Cost | Memory (DRAM+NAND) Share in AI Server Cost | Trend |

|---|---|---|---|

| 2024 | 20% | 18% | Baseline |

| 2025 | 28% | 25% | Rising |

| 2026 | 35% | 30% | Accelerating |

| 2027E | 40% | 35% | Continuous rise |

Transmission of Inflation Spiral:

- Hyperscaler Capex $725B → AI chip demand $500-550B

- AI chip demand → HBM demand $175-195B (35% share)

- HBM long-term contract lock-in → spot market tension

- Spot price surge → spot demand squeeze

- Spot demand squeeze → HBM vendor expansion

- Expansion cycle 2-3 years → shortage continues to 2027-2028

Risks:

- If AI chip demand exceeds expectations, "memory tax" may rise to 45%+

- SK Hynix/Samsung/Micron may leverage "sellers' market" to obtain excess profits

- Hyperscalers' "AI ROI" model faces challenges

5.2 Geopolitics and "Foundry Capacity Rebalancing"

TSMC's "sellers' market" is highly dependent on global foundry capacity stability, and geopolitics may trigger "foundry capacity rebalancing."

Key Risks:

| Risk | Impact | Time Window |

|---|---|---|

| Taiwan Strait Crisis | TSMC global supply disruption | Unpredictable |

| US-China Export Control Escalation | TSMC China revenue to zero | 12-24 months |

| Korea/Japan Earthquake | Memory capacity short-term disruption | Unpredictable |

| EU Carbon Tariff | TSMC European customers cost +5-10% | 18-36 months |

| US Export Controls | AI chip customer structure change | Continuous |

Possible Paths of Capacity Rebalancing:

- US Domestic: Intel 18A/14A + Samsung Texas + TSMC Arizona

- Europe: TSMC Dresden + Bosch/VIS

- Japan: TSMC Kumamoto + Rapidus

- India: TSMC/India Government cooperation (planned)

- Korea: Samsung Pyeongtaek expansion

Key Insight: 2027-2030 global foundry capacity will form a "China+US+Europe+Japan+India" five-pole structure, and TSMC's "sellers' market" position may be partially weakened by diversification.

5.3 "In-House ASIC" Disruption Risk

Hyperscalers' "in-house ASIC" is a potential disruptor to TSMC's "sellers' market."

Capacity Squeeze Effect of In-House ASIC:

- 2026 Hyperscaler in-house ASIC demand $30-40B

- 2027 expected $60-80B

- 2028 expected $100B+

- In-house ASIC CoWoS/N3 demand directly competes with NVIDIA

Typical In-House ASIC:

- Google TPU v6/v7: CoWoS capacity occupied 20-25% in 2026

- AWS Trainium 3: CoWoS capacity occupied 15-20% in 2026

- Microsoft Maia 100: CoWoS capacity occupied 10-15% in 2026

- Meta MTIA v3: CoWoS capacity occupied 10% in 2026

[Verified - Morgan Stanley 2026-07-12 / High Confidence - Inference]

Key Insight: The "capacity squeeze" of in-house ASIC further intensifies CoWoS sold out, but it also gives Hyperscalers enhanced "bargaining power" against TSMC—this is the "self-hedging" mechanism of TSMC's "sellers' market."

5.4 Key Test of "AI Demand Sustainability"

TSMC's "sellers' market" is built on a key assumption—that AI demand continues to grow rapidly. If AI demand growth slows, TSMC's "sellers' market" will quickly turn into a "buyers' market."

Four Tests of AI Demand Sustainability:

- AI ROI Implementation: Whether enterprise AI projects can achieve "clear ROI" in 2026-2027

- Regulatory Pressure: New York State's 1-year ban may spread, affecting Hyperscaler Capex

- Model Efficiency Improvement: DeepSeek V4/GPT-5.6 and other model efficiency improvements may reduce compute demand

- Alternative Technologies: Photonic computing/quantum computing/neuromorphic computing may disrupt GPU route

[Verified - DeepSeek V4 release / GPT-5.6 release / New York State ban / Google/Microsoft new model releases]

Key Insight: TSMC's "sellers' market" is highly certain in 2026-2027, but faces "AI demand sustainability" tests in 2028-2030.

6. Conclusion

6.1 Multi-Level Significance

For Hyperscalers (CIO/CDO Level):

- Immediate action: Take stock of 2026 Q3-Q4 AI chip/HBM/CoWoS long-term contract status, identify "no contract" risk

- Short-term (6-12 months): Accelerate signing 3-5 year HBM4/CoWoS long-term contracts (reference Microsoft/Google/Meta signed contracts)

- Mid-term (12-36 months): Establish "in-house ASIC + commercial chip" dual-track strategy, diversify CoWoS dependency

- Long-term: Watch TSMC N2/N3P/CoWoS expansion progress, 2027-2028 is the "compute cost turning point" window

For Enterprise IT Decision Makers:

- AI Cloud Pricing: May face 10-20% price increases in 2026 Q4-2027 Q1 (transmitting TSMC/PSMC/HBM price increases)

- AI Service ROI: Under rising compute cost pressure, "model efficiency" becomes a new key

- In-House Model Evaluation: DeepSeek V4/Mistral 70B and other cost-effective models' attractiveness rising

- Edge AI: Local/edge AI deployment economics improving

For Investors:

- TSMC: 5 consecutive quarterly highs + sellers' market = continued valuation repair in 2026-2027

- PSMC/SK Hynix/Samsung/Micron: Memory price increase + long-term contract = 2026 Q3-Q4 performance exceeding expectations

- NVIDIA/AMD: AI chip demand strong, but need to watch Hyperscaler in-house ASIC "capacity squeeze"

- Cisco/Palo Alto/CrowdStrike: AI data center construction continues, network/security demand stable

6.2 Investment Perspective

Direct Beneficiaries:

- TSMC (2330.TW / TSM.US): 5 consecutive quarterly highs + sellers' market + CoWoS bottleneck premium

- PSMC (6770.TW): DRAM price increase + 3D AI foundry share rising

- SK Hynix (000660.KS)/Samsung (005930.KS)/Micron (MU.US): HBM4 long-term contract + price increase

- ASML (ASML.US): High-NA EUV sole supplier

- Long-term DRAM/CoWoS suppliers

Neutral:

- NVIDIA: AI chip demand strong, but HBM4 certification + long-term contract squeeze

- AMD: MI400 series demand certain, but capacity limited

- Apple: N3 large customer, but cost +5% may affect iPhone 18 pricing

Short-term Pressure:

- Small and medium chip design companies that rely on TSMC but have weak bargaining power

- Secondary AI chip vendors without HBM/CoWoS long-term contracts

- NVIDIA China customers highly dependent on H200/H20 (already affected by export controls)

6.3 Key Nodes in the Next 12-24 Months

- 2026 Q3 (7-16/7-17): TSMC Q2 earnings call confirms 70% gross margin + full-year guidance upward revision

- 2026 Q3: Hyperscaler Q2 earnings (Alphabet 7-22, Microsoft/Meta 7-29, Apple/Amazon 7-30) confirm AI Capex continues

- 2026 Q4: TSMC Q3 earnings + N2 mass production progress update

- 2026 Q4: PSMC Q3 earnings + 3D AI foundry share update

- 2027 Q1: Vera Rubin/Rubin Ultra mass production + HBM4 full shipment

- 2027 Q2: TSMC N3P large-scale mass production + CoWoS expansion reaches 95,000 wafers/month

- 2027 H2: Compute cost turning point expectation

6.4 Strategic Judgment

TSMC Q2 2026 earnings is the "final confirmation" of "AI compute supply-side"—5 consecutive quarterly highs + N3/CoWoS sold out + price increase 5-10% + PSMC DRAM price increase 45% + Hyperscaler Capex $725B form the "full-chain confirmation" of the "AI compute sellers' market."

Core Judgment:

- "AI Compute Sellers' Market" is the "supply-side main line" of the 2026-2027 AI Capex cycle—TSMC/PSMC/HBM three-axis simultaneous price increase

- 7-15 NY ban (demand-side regulation) and 7-16 TSMC Q2 (supply-side price increase) form the "AI Capex scissors divergence"—AI compute total cost faces "double price increase" in H2 2026

- Hyperscalers' "in-house ASIC + long-term contract + geographic diversification" are the three major hedges against the "sellers' market"

- 2027-2028 is the "compute cost turning point"—N2/N3P/CoWoS expansion + long-term contract expiration renegotiation

Real Impact:

- Short-term (12 months): TSMC/PSMC/SK Hynix/Samsung/Micron valuation continued repair

- Mid-term (12-24 months): Hyperscaler AI ROI model faces test

- Long-term (24-36 months): AI compute supply-demand moves toward new balance, geopolitics and in-house ASIC become key variables

The AI compute "sellers' market" will not last forever—but 2026-2027 is an unquestionable "sellers' time window."

Sources:

[1] Reuters - TSMC posts record June revenue on AI demand (2026-07-13) - https://www.reuters.com/technology/tsmc-q2-2026-record-revenue/

[2] TSMC Investor Relations 2026-07-10 Monthly Revenue Announcement - https://investor.tsmc.com/

[3] SemiAnalysis - TSMC Q2 2026 Deep Dive (2026-07) - https://semianalysis.com/

[4] DigiTimes - TSMC to raise 3/5/7nm prices by 5-10% (2026-07-09)

[5] Counterpoint Research - Foundry Market Share Q1 2026 (2026-06)

[6] JPMorgan - TSMC Q2 2026 Preview (2026-07-08)

[7] Powerchip Semiconductor Manufacturing Corporation Q2 2026 Earnings Call 2026-07-14 - 36Kr Report

[8] Morgan Stanley - Hyperscaler Capex 2026 (2026-07-12)

[9] Morgan Stanley - AI Memory Market 2026 (2026-07-12)

[10] Guoyuan Securities - Semiconductor Industry Q3 Outlook (2026-07-12)

[11] Donghai Securities - Wafer Foundry Sellers' Market Return (2026-07-13)

[12] Morgan Stanley - TSMC Supply-Demand Outlook (2026-07-09)

[13] Goldman Sachs - TSMC Pricing Power (2026-07-10)

[14] NVIDIA Q1 FY2027 Earnings (2026-05) - https://nvidianews.nvidia.com/

[15] SK Hynix 2026-Q2 Earnings Call (2026-07-25 expected)

[16] DeepSeek V4 Release (2026-06)

[17] GPT-5.6 Release (2026-05)

Why it Matters

TSMC Q2 2026 earnings is the 'final confirmation' of 'AI compute supply-side'—5 consecutive quarterly highs + N3/CoWoS sold out + 5-10% price increase + PSMC DRAM 45% price increase + Hyperscaler Capex $725B form 'AI compute sellers' market' full-chain confirmation. 7-15 NY ban (demand regulation) and 7-16 TSMC Q2 (supply price increase) form 'AI Capex scissors divergence', AI compute total cost faces 'double price increase' in H2 2026. Hyperscalers need to hedge through 'in-house ASIC + long-term contracts + geographic diversification' three axes. 2027-2028 is the 'compute cost turning point'.

DECISION

- Hyperscaler CTOs/CIOs: Within 30 days, take stock of 2026 Q3-Q4 AI chip/HBM/CoWoS long-term contract status, identify 'no contract' risk; accelerate signing 3-5 year HBM4/CoWoS long-term contracts (reference Microsoft/Google/Meta signed contracts); establish 'in-house ASIC + commercial chip' dual-track strategy, diversify CoWoS dependency; watch TSMC N2/N3P/CoWoS expansion progress

- AI Infrastructure Investors: Overweight TSMC (2330.TW/TSM.US) / PSMC (6770.TW) / SK Hynix / Samsung / Micron; focus on CoWoS/HBM long-term contract suppliers; focus on ASML (ASML.US) High-NA EUV sole supplier position

- Enterprise IT Decision Makers: Evaluate AI Cloud pricing 10-20% potential increase in 2026 Q4-2027 Q1 (transmitting TSMC/PSMC/HBM price increases); re-evaluate AI service ROI models; consider cost-effective models (DeepSeek V4/Mistral 70B); focus on edge AI deployment economics

- NVIDIA/AMD Competitive Analysis: CoWoS capacity squeeze effect from Hyperscaler in-house ASIC (Google TPU/AWS Trainium/Microsoft Maia/Meta MTIA)—in-house ASIC CoWoS occupancy 60%+ in 2026, affecting NVIDIA capacity allocation

PREDICT

- 7-16: TSMC Q2 earnings call confirms 70% gross margin challenge + full-year guidance upward revision to +35%/+69-70% gross margin

- Within 12 months: Hyperscaler Q2 earnings (Alphabet 7-22, Microsoft/Meta 7-29, Apple/Amazon 7-30) confirm AI Capex $725B continues; Vera Rubin/Rubin Ultra mass production timeline confirmed; HBM4 70% long-term contract dominates spot market

- Within 12-18 months: TSMC N2 mass production 140,000 wafers/month (2026 Q4) / CoWoS expansion to 95,000 wafers/month (2027); Vera Rubin full shipment; PSMC 3D AI foundry share rises from 5.4% to 8%+

- Within 18-24 months: Compute cost turning point initially emerges (N2/N3P large-scale mass production); HBM4 long-term contract expiration renegotiation (2027 Q2-Q3); 'AI Capex scissors divergence' may begin to converge in H2 2027; 'Memory tax' rises from 35% to 40%+

- Within 24-36 months: AI compute supply-demand moves toward new balance; geopolitics and in-house ASIC become key variables; TSMC 'sellers' market' position partially weakened by diversification

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)