Event Overview

On July 5, 2026, semiconductor research firm SemiAnalysis released a blockbuster report claiming that NVIDIA's next-generation flagship AI server system Kyber faced significant production delays due to core PCB circuit board manufacturing challenges, with the original H2 2027 launch potentially pushed to 2028. This news sent shockwaves through global capital markets—Asian PCB manufacturers saw collective stock plunges, with NVIDIA's largest supplier Ibiden dropping 10%, Zhejiang Union Holding H-shares tumbling 18%, and Samsung Electro-Mechanics falling 11%.

However, the plot reversed the next day. An NVIDIA spokesperson quickly responded: "Our product roadmap remains unchanged," explicitly denying the delay rumors. Capital markets reacted with remarkable calm—NVIDIA shares rose a mere 0.37% to $195.55 on Monday, with market cap stable at $4.73 trillion. Mizuho Securities analyst Jordan Klein dismissed the episode as "clickbait noise."

Kyber represents NVIDIA's next-generation core rack architecture for hyperscale AI training and AI factories. Its strategic importance cannot be overstated. The architecture abandons traditional horizontal server tray layouts in favor of book-style vertical blade stacking, with the NVL144 version integrating 144 Rubin Ultra GPUs per rack, while the expanded NVL576 version accommodates up to 576 GPUs. Compared to the current Blackwell platform, Kyber delivers over tenfold improvement in FP4 inference compute to 15 EFLOPS.

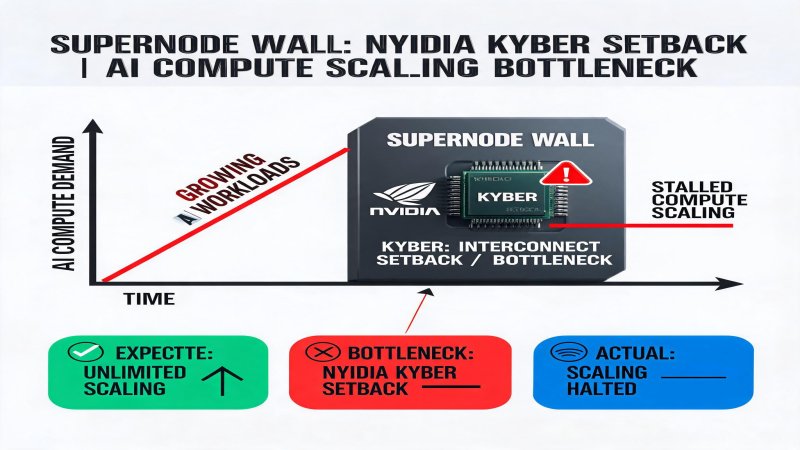

The technical details from SemiAnalysis' exposé warrant deeper investigation: 78-layer ultra-high-density multilayer PCB design creates manufacturing feasibility challenges; NVIDIA was forced to cancel the four-chip Rubin Ultra version in favor of a two-chip solution, cutting performance in half; the proposed NVL72x2 backup configuration was rejected by cloud providers for being "operationally unworkable." These details reveal a deeper issue: AI compute scaling is hitting the walls of physical reality.

Technical Deep-Dive: Physical Limits of AI Factories

Engineering Challenges of SuperNode Architectures

From a technical architecture perspective, the Kyber delay rumors expose the core contradiction in AI infrastructure development: industry demand for compute density is exceeding the boundaries of physical feasibility.

Density vs Reliability: Traditional data center racks consume approximately 10-30kW, while AI supernodes can reach 100kW+ per rack. Kyber NVL576's vertical stacking design integrating 576 high-performance GPUs in limited space means power density increases by an order of magnitude. This places extreme demands not only on power delivery systems but creates severe challenges in cooling and reliability.

Interconnect Bottlenecks: All-to-All communication among 576 GPUs requires ultra-high-speed interconnect. While NVLink 5.0 theoretical bandwidth reaches 3.6TB/s, physical implementation requires complex multilayer PCB stacking. Signal integrity issues on any single layer can cause total yield collapse.

Serviceability Paradox: Ultra-high density means single node failures affect larger areas while maintenance windows shrink. Cloud providers rejecting the NVL72x2 backup configuration suggests they prefer sacrificing some compute density over accepting exponential growth in operational complexity.

Competitive Landscape Comparison

Table 1: Major AI Chip Vendor SuperNode Roadmap Comparison

| Vendor | Architecture | GPUs per Rack | Expected Production | Interconnect | Cooling |

|---|---|---|---|---|---|

| NVIDIA | Kyber NVL576 | 576 | 2027H2 (reported delay) | NVLink 5.0 | Full liquid |

| AMD | MI450 | 256 | 2027 | Infinity Fabric 5.0 | Hybrid |

| Intel | Gaudi 4 | 128 | 2026H2 | CCIX 2.0 | Air-capable |

| Huawei | CloudMatrix 384 | 384 | In production | HCCS | Full liquid |

| Metric | NVIDIA Kyber | AMD MI450 | Intel Gaudi 4 | Huawei CloudMatrix |

|---|---|---|---|---|

| FP4 Compute (EFLOPS) | 15 | 8.2 | 3.5 | 6.8 |

| HBM Bandwidth (TB/s) | 19.2 | 12.8 | 6.4 | 9.6 |

| Power (kW) | 120 | 85 | 45 | 95 |

| Efficiency (TFLOPS/kW) | 125 | 96 | 78 | 72 |

Financial Logic: Return-on-Compute Investment Dilemmas

NVIDIA's Pricing Power Moat

Despite technical challenges, NVIDIA's financial performance remains stellar. FY2026 data center revenue is projected to exceed $200 billion, and the minimal stock price impact from Kyber delay rumors confirms market confidence in NVIDIA's moat.

NVIDIA's business model is evolving from "selling GPUs" to "selling AI factories." The Spectrum-X network platform helped NVIDIA reach #1 position in data center Ethernet switch market in Q1 2026, with revenue of $2.1 billion representing 192.7% year-over-year growth and 21.5% market share. This means customers purchasing NVIDIA GPUs typically "bundle buy" NVIDIA networking equipment, creating ecosystem lock-in.

More importantly, NVIDIA's AI Computing Partnership program uses credit enhancement, revenue sharing, and GPU buyback mechanisms to transfer customer investment risk to NVIDIA while securing long-term compute supply commitments. This transforms NVIDIA from a hardware vendor into an "AI Compute Central Bank"—holding pricing power over compute supply.

Cloud Provider CapEx Pressure

However, cloud provider capital expenditure pressure is accumulating. Combined AI CapEx for Meta, Google, and Microsoft is projected to exceed $300 billion in 2026, with approximately 60% flowing to hardware procurement. This investment intensity is unsustainable.

Samsung's "death earnings" stock plunge reveals deep market concerns about AI investment returns. When memory chip profits surge 18-fold yet trigger selling, it signals investors have begun questioning the marginal returns on AI infrastructure investment. Samsung's Q2 operating profit of 89.4 trillion KRW already exceeds NVIDIA's by over two times, yet its stock hit record lows—the core logic being "buy the rumor, sell the news." Markets had fully priced the memory price hike; genuine concerns center on potential price collapse once Samsung + SK Hynix's 3,200 trillion KRW production expansion comes online in 2028.

The same logic applies to AI compute. When NVIDIA Rubin Ultra and AMD MI450 reach mass production in 2027-2028, compute supply will face structural oversupply. Cloud providers forced to lock in long-term contracts at price peaks will face dual pressure from capacity release and declining utilization rates.

Strategic Deep-Dive: Geopolitical Dynamics of AI Compute

National Strategy of Supply Chain Security

The Kyber-triggered A-share PCB sector "roller coaster" reveals AI infrastructure's supply chain fragility. Taiwan-region PCB supply chains play core roles in AI server motherboards—companies like Shalun Precision, Sheng Hong Technology, and Dongshan Precision bear NVIDIA and customer pressure for price cuts while managing cash flow strain from expansion.

Geopolitics further complicates supply chain dynamics. US export controls on semiconductors to China continue tightening, with NVIDIA H100/H200 exports to China restricted. This forces Chinese cloud providers toward domestic alternatives, creating development windows for Huawei Ascend, Cambricon, and other local chips—while limiting Chinese AI training compute ceilings.

Engineering Insights from the Huawei Path

Huawei CloudMatrix 384's successful mass production offers critical lessons: achieving equivalent compute through system-level optimization is viable engineering when EUV lithography remains restricted.

Multi-Chip Horizontal Scaling: Huawei employs 384 Ascend 910C chips via HCCS interconnect rather than pursuing maximum single-chip density. This reduces single-chip manufacturing difficulty while improving supply chain availability.

Standard Rack Design: CloudMatrix 384 uses standard 19-inch racks—each rack separable, maintainable, and transportable, overcoming serviceability pain points of ultra-dense architectures.

Software Ecosystem Closure: Cluster scheduling optimization based on MindSpore framework achieves heterogeneous compute coordination across Ascend chips. Even with inferior single-chip performance versus NVIDIA, superior software scheduling can compensate.

This "system optimization priority" path contrasts with NVIDIA's "maximum single-chip performance" approach. Both have trade-offs: NVIDIA targets performance ceilings; Huawei prioritizes supply chain resilience and serviceability. During the current AI compute demand surge, both paths have room to coexist.

Challenges and Concerns

Technical Route Uncertainty

The core issue in Kyber delay rumors concerns PCB midplane manufacturing yield. Despite NVIDIA's denial, the technical challenge of 78-layer ultra-high-density multilayer PCBs is real. Historically, Blackwell faced similar doubts (thermal, power, HBM compatibility) yet shipped on schedule though with slower-than-expected ramp.

More fundamental uncertainty looms: Do physical limits exist for supernode architectures? When compute density increases by an order of magnitude, must reliability, cost, and serviceability worsen exponentially? These questions currently lack answers—engineering practice must provide validation.

Competitive Landscape Dynamics

NVIDIA's dominance faces triple threats: direct competition from AMD MI450 (AMD MI300X already surpasses H100 in memory bandwidth), flanking attacks from custom ASICs (Google TPU, AWS Trainium, Microsoft Maia, OpenAI Jalapeño), and system-level competition (Huawei CloudMatrix achieving equivalent compute via multi-chip coordination).

NVIDIA's software moat (CUDA ecosystem) represents its most critical defense. However, as PyTorch 2.0's support for non-CUDA backends improves and ROCm ecosystem matures, this moat erodes. Perplexity's adoption of both NVIDIA Vera CPU and AMD MI chips demonstrates multi-vendor strategies becoming industry consensus.

Demand-Side Cyclical Risk

AI investment sustainability emerges as the paramount concern. Samsung's "death earnings" stock plunge, triggered by the memory sector selloff, fundamentally reflects market repricing of AI demand expectations. Morgan Stanley's observation that "the rate of change has peaked" suggests the AI infrastructure supercycle may be topping.

If AI application-layer commercialization develops slower than expected (currently 95% of enterprise generative AI pilots fail to generate measurable ROI), cloud provider CapEx faces contraction pressure, impacting upstream chip and PCB supply chains. The entire AI infrastructure chain's valuation logic will require restructuring.

Conclusion: Multi-Layered Significance

Implications for Industry Development

The Kyber controversy (whether real or rumor) exposes AI infrastructure's core contradiction: exponential compute demand growth versus linear physical world expansion limits. This contradiction won't resolve short-term but will drive industry exploration of new technical paths—from chip design (Chiplet, 3D stacking) to system architecture (distributed training, model parallelism) to cooling technology (immersion liquid cooling, nuclear power).

Whether NVIDIA's "AI Compute Central Bank" model sustains depends on whether AI application layers generate sufficient commercial value to support continued compute investment. This forms a positive feedback loop—applications drive demand, demand drives investment, investment drives R&D, R&D produces stronger compute. But the loop can also reverse: when application deployment underperforms, CapEx contracts, R&D investment declines, compute density growth slows, and the industry enters a de-capacity cycle.

Value for Enterprise Decision-Makers

For enterprise technology decision-makers, the Kyber event provides several critical insights:

Supply chain diversification is mandatory: Single-vendor strategies carry unacceptable risk in the AI era. NVIDIA's technical leadership cannot eliminate supply risks from geopolitics, capacity fluctuations, or pricing power dynamics. Recommendation: maintain NVIDIA for core training workloads while testing alternatives for inference and edge scenarios.

Compute utilization matters more than peak compute: Huawei CloudMatrix 384 demonstrates that 58% cluster utilization can outperform competitors claiming higher compute but achieving only 35% utilization. Enterprises should invest in compute scheduling optimization and workload consolidation rather than pursuing higher-end GPU procurement alone.

Focus on total cost of ownership, not acquisition cost: In AI cluster full lifecycle costs, power comprises 40-50%, operations 20-30%, and acquisition only 20-30%. Full liquid cooling and high-density designs may reduce electrical efficiency while increasing operational complexity. Enterprises should build TCO models to evaluate long-term value across different architectures.

Investor Perspective

For investors, the Kyber episode reveals the cyclical nature of AI infrastructure investment:

Short-term: Supply chain volatility and competitive landscape changes create trading opportunities. Kyber delay rumors created PCB sector declines providing buying windows (since news was quickly denied); Samsung's "death earnings" triggered memory sector declines warranting observation (this may mark a structural turning point).

Medium-term (2026-2028): Competition landscape among NVIDIA vs AMD vs custom ASICs will determine who dominates the AI compute era. NVIDIA's software moat and scale advantages provide defensive assets, but face erosion from cost-driven customers pursuing multi-vendor strategies.

Long-term (2028+): When compute density approaches physical limits, AI infrastructure competition will shift from chip performance to system efficiency, software ecosystems, and energy supply. Enterprises establishing advantages across these dimensions will emerge as leaders in next-generation AI infrastructure.

Why it Matters

AI infrastructure is transitioning from "compute hunger" to "compute efficiency" paradigm. NVIDIA's "AI Compute Central Bank" model faces physical limits; Huawei's system optimization path offers an alternative. Samsung's "death earnings" already revealed market's deep concerns about AI investment sustainability. Engineering challenges in supernode architectures will reshape AI infrastructure competitive dynamics for the next 3-5 years.

DECISION

- Enterprise Tech Leaders: Maintain NVIDIA for core training workloads while testing AMD/ASIC alternatives for inference and edge; 2. Prioritize compute scheduling optimization over pure GPU procurement upgrades—58% utilization can outperform competitors claiming higher compute at 35%; 3. Build TCO models evaluating full lifecycle costs, not just acquisition costs.

PREDICT

- Within 12 months: Kyber delay impact subsides, but GTC 2026 will reveal production ramp details; 2. Within 24 months: AMD MI450 and NVIDIA Rubin Ultra direct competition, enterprise multi-vendor strategies accelerate adoption; 3. Within 36 months: If AI application commercialization fails validation, cloud provider CapEx cuts will trigger AI infrastructure de-capacity cycle.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)