I. Event Recap

On July 6, 2026, multiple structurally significant messages emerged from the global AI chip market, revealing that the cloud and edge AI chip landscape is undergoing profound reshaping. AWS notified its supply chain to raise Q3 2026 ASIC server shipments by 20-30% from original plans, with optimistic Trainium 3 sales prospects; Apple was reported to globally launch the M7 chip, skipping the M6 generation to bet directly on edge AI; Huawei's Mate 90 series confirmed it will carry a new Kirin chip based on Tao's Law, with transistor density improving 53.5%; NVIDIA announced the RTX Spark super chip will debut at BW2026, aggressively entering the personal AI PC market; meanwhile, Microsoft Azure laid off 200-400 employees in China, with some offered transfers to Canada.

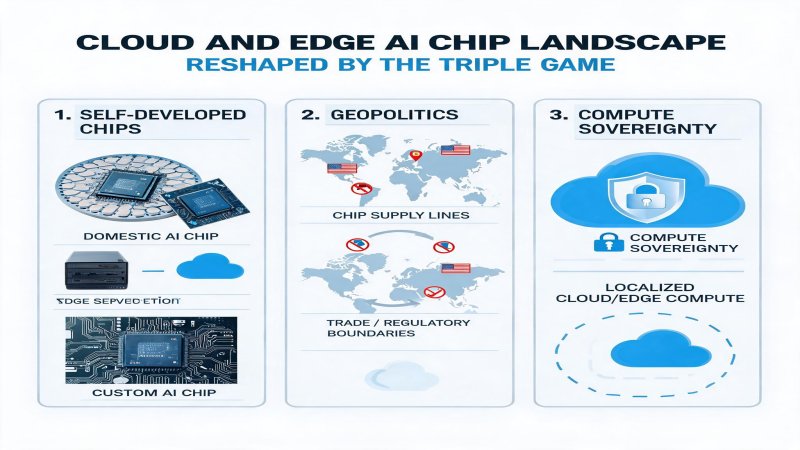

These five developments, seemingly scattered across cloud, edge, and geopolitical dimensions, collectively point to one core trend: AI computing is evolving from 'centralized' (hyperscale cloud data centers) to 'distributed' (cloud self-developed chips + edge AI chips), with geopolitical factors accelerating this transition. AWS Trainium shipment increases mark cloud providers' self-developed AI chips moving from 'experimental projects' to 'large-scale deployment'; Apple M7 and Huawei Kirin represent two technical routes for edge AI—traditional process catch-up versus architectural innovation breakthroughs; NVIDIA RTX Spark is a strategic move from data centers to consumer AI PCs; while Azure China layoffs embody how geopolitical risks directly impact multinational cloud providers' operations.

On the timeline, summer 2026 became a critical window for AI chip industry changes. On July 6 alone, US pre-market storage chip stocks surged across the board, reflecting sustained market optimism for AI computing demand. Yet beneath this optimism, industry participants face increasingly complex strategic choices: cloud vendors must find optimal balance between self-developed chips and NVIDIA GPUs; edge device makers must explore architectural innovation under process constraints; multinational enterprises must carefully weigh data sovereignty, compliance requirements, and market opportunities.

II. Technical Depth

Cloud-side AI chip technology is transitioning from 'general-purpose GPU dominance' to 'GPU+ASIC+FPGA heterogeneous computing.' AWS Trainium series exemplifies this transition. Trainium 3 adopts advanced processes, optimized specifically for deep learning training workloads, offering higher compute density and energy efficiency per dollar than equivalent GPUs in specific scenarios. AWS's decision to raise Q3 shipments by 20-30% implies internal consensus on Trainium's TCO advantages has reached the critical point for large-scale deployment.

However, self-developed chips are not a panacea. Trainium's flexibility and software ecosystem maturity for training large-scale Transformer models still lag behind NVIDIA's CUDA ecosystem. AWS's strategy is 'tiered deployment': training and complex inference continue using NVIDIA GPUs, while standardized inference workloads migrate to Trainium, optimizing comprehensive TCO. This 'hybrid architecture' is becoming the standard strategy for global hyperscalers—Google has TPU, Microsoft has Maia, Meta has MTIA, all following similar logic.

Edge AI chips present a completely different competitive landscape. Apple's M7 chip, skipping the M6 generation, indicates Apple believes edge AI competition has reached a critical inflection point. The M7 is expected to adopt more advanced process technology, integrating dedicated neural network engines to support more complex local AI inference tasks. Apple's competitive advantage lies in hardware-software integration—from chip architecture to Core ML framework to developer ecosystem, forming a closed-loop experience.

Huawei's Kirin 2026 chip represents a distinctly different technical route. Under advanced process constraints, Huawei achieves performance breakthroughs at the architectural level through 'Tao's Law' (Chiplet 2.5D hybrid bonding). Test data shows that compared to traditional 2D design chips, transistor density improves 53.5%, reaching 238 MTr/mm², with significant P-core energy efficiency gains. The significance of this technical route is that even without access to the most advanced process nodes, near-flagship performance can be achieved at equivalent 3nm levels through advanced packaging and architectural design.

NVIDIA RTX Spark's debut marks the substantive arrival of the 'AI PC' concept. RTX Spark integrates dedicated AI acceleration units, supporting higher-parameter local model execution, targeting content creation, AI development, and gaming experiences. NVIDIA's strategic intent is clear: while dominating the data center GPU market, extend AI computing power to the personal consumer market, building a full-stack AI computing platform from cloud to edge.

| Vendor | Product/Route | Technical Features | Target Scenario | Competitive Advantage ||--------|--------------|-------------------|-----------------|---------------------|| AWS | Trainium 3 | ASIC dedicated architecture | Cloud training/inference | Cost optimization + scale || Apple | M7 chip | Advanced process + NN engine | Mac/iPad edge AI | Hardware-software integration || Huawei | Kirin 2026 | Tao's Law Chiplet architecture | Mate 90 edge AI | Architectural innovation || NVIDIA | RTX Spark | Super chip + AI acceleration | Personal AI PC | CUDA ecosystem + full stack || Microsoft | Maia/Azure | Self-developed + partners | Cloud AI services | Enterprise customer breadth |

III. Financial Logic

From a financial perspective, cloud providers' core driver for self-developed chips is TCO optimization. NVIDIA H100/B100 GPU single-card prices have exceeded $30,000, while AI large model training and inference demands continue expanding exponentially, driving cloud providers' AI infrastructure capex to staggering levels. Microsoft's latest financial report shows Azure AI annualized revenue at approximately $33 billion, but corresponding GPU procurement costs are equally staggering. Although self-developed ASICs require massive upfront R&D investment (typically hundreds of millions to billions of dollars), once deployed at scale, per-card costs can be 30-50% lower than GPUs.

AWS Trainium 3's shipment increase of 20-30% implies Amazon has internally reached consensus on Trainium's TCO advantages. Industry analysis suggests that if AWS migrates 20-30% of standardized inference workloads from GPUs to Trainium, it could save hundreds of millions of dollars in infrastructure costs annually. More strategically, self-developed chips also provide cloud vendors with differentiated pricing capabilities—they can offer customers 'low-cost AI instances based on self-developed chips' to capture competitive advantages in price-sensitive markets.

The financial significance of Apple's M7 chip lies in gross margin protection. Apple's self-developed chips typically deliver 10-15 percentage points higher gross margins than externally sourced chips. Amid the global semiconductor price surge, self-development capability becomes Apple's key barrier for cost control and maintaining premium product profitability. Skipping M6 to directly launch M7, while meaningning concentrated short-term R&D investment release, enables faster capture of first-mover advantage in edge AI.

Huawei Kirin chip's financial logic is more complex. Due to advanced process constraints, Huawei must invest more in R&D than competitors to achieve equivalent performance. However, successful commercialization of Kirin chips means Huawei's smartphone business can regain high-end market competitiveness, driving device sales and ecosystem revenue. Estimates suggest Mate series sales reach tens of millions per generation, with self-developed chip scale amortization effects gradually appearing in 2026-2027.

NVIDIA RTX Spark represents a new growth curve for NVIDIA in the consumer market. While data center AI GPUs are highly profitable, they are cyclical and customer-concentrated. The personal AI PC market, though lower per-customer value, has a massive user base (global PC annual shipments ~250 million units), and replacement cycles may shorten driven by AI features. If RTX Spark can replicate GeForce's gaming market success, NVIDIA could open a multi-billion dollar new revenue source in consumer AI chips.

IV. Strategic Depth

The reshaping of cloud and edge AI chip landscapes is essentially the technical manifestation of 'compute sovereignty' competition. From a strategic matrix perspective, major players show significant positioning and strategy differences.

Hyperscale cloud providers (Amazon, Microsoft, Google, Meta) are pursuing 'de-NVIDIA-fication' strategies. This does not mean completely replacing NVIDIA GPUs, but rather reducing dependence on a single supplier through self-developed chips while gaining cost and differentiation advantages in standardized workloads. Microsoft Azure China layoffs, while not directly related to self-developed chips, reflect the complexity multinational cloud providers face in global strategic layout—pursuing technology autonomy while managing geopolitical operational constraints.

Apple and Huawei represent two strategic paradigms for edge AI. Apple's 'process leadership + ecosystem closed loop' model relies on support from advanced foundries like TSMC, maintaining competitiveness through continuous process dividend investment and hardware-software co-optimization. Huawei's 'architectural innovation + self-controllability' model is a survival path under external constraints, using Chiplet, logic folding, and other architectural innovations to catch up on performance despite process lag. Both models have pros and cons: Apple's model delivers more mature user experience but with concentrated supply chain risk; Huawei's model offers greater self-controllability but requires time to build commercial scale and software ecosystem.

NVIDIA's strategy is 'full-stack dominance.' On top of 80%+ data center GPU market share, it extends to consumer markets through RTX Spark, locks developers and enterprise customers through the CUDA ecosystem, and provides fully managed AI compute services through DGX Cloud. NVIDIA's potential risks include: cloud providers' self-developed chips eroding inference market share, geopolitical restrictions on China sales, and antitrust scrutiny of its ecosystem lock-in strategy.

| Vendor Type | Representative | Core Strategy | Main Advantage | Key Risk ||-------------|---------------|---------------|----------------|----------|| Cloud ASIC | Amazon/Google/MS | De-NVIDIA + TCO optimization | Scale + customer stickiness | Ecosystem immaturity || Edge process leader | Apple | HW-SW closed loop | User experience + brand premium | Supply concentration || Edge architecture innovator | Huawei | Self-controllability | Tech breakthrough + policy support | Process bottleneck + ecosystem || Full-stack GPU leader | NVIDIA | DC to edge full coverage | CUDA ecosystem + tech lead | Customer self-dev + geo risk || Traditional x86/foundry | Intel/TSMC | IDM 2.0/neutral foundry | Manufacturing + customer base | Process catch-up / geo risk |

V. Challenges and Concerns

The reshaping of cloud and edge AI chip landscapes faces multiple structural challenges.

Technology ecosystem fragmentation is the primary challenge. Cloud vendors each promote proprietary ASIC architectures (Trainium, TPU, Maia, MTIA), causing AI development frameworks and toolchains to fragment. Developers face rising costs for migrating models between cloud platforms, potentially inhibiting AI application innovation speed. While intermediate formats like ONNX attempt to solve interoperability issues, actual deployment still faces performance losses and feature gaps.

Edge AI's power-performance balance is another major challenge. Running large language models locally requires massive compute and memory bandwidth, yet terminal devices like phones and laptops have limited thermal dissipation and battery capacity. Apple M7 and Huawei Kirin must find optimal balance between inference efficiency and energy consumption, otherwise 'AI features' risk becoming marketing gimmicks rather than practical experiences.

Geopolitical risk casts a shadow over the entire industry. US export controls on chips to China have extended to advanced processes, EDA tools, and high-end GPUs, with Microsoft Azure China layoffs being just one manifestation of this larger trend. If controls escalate further, the global semiconductor supply chain could split into 'US camp' and 'China camp,' with technology standards, IP flows, and market access all facing restructuring. For multinational enterprises, this means rising compliance costs and strategic uncertainty.

Investment return cycle uncertainty also warrants attention. Cloud providers' massive upfront R&D investment in self-developed chips faces uncertainty from AI technology evolution directions (such as model architecture changes, quantization breakthroughs) that could quickly obsolete developed ASICs. If ROI falls short of expectations, some cloud providers may reevaluate self-developed chip strategic priorities, even cutting related team sizes.

VI. Conclusion

From an investment perspective, cloud and edge AI chip landscape reshaping is in a 'strategic stalemate' phase: NVIDIA's dominance in data center GPUs is unlikely to be shaken in the short term, but cloud providers' self-developed chip erosion in inference markets has already begun; edge AI chip competition presents a multi-polar landscape with Apple, Qualcomm, MediaTek, and Huawei competing, where technical route and market strategy differentiation will determine the market map over the next 3-5 years.

Forward-looking judgments:

- In H2 2026, AWS Trainium 3, Google TPU v6, and Microsoft Maia 100 will form the first substantive wave impacting NVIDIA's inference market, with the three collectively expected to grow inference workload market share from current 5-8% to 12-15%.

- Apple M7 and Huawei Kirin 2026 will face direct competition in Q4 2026, with edge AI chip competition focus shifting from 'peak compute' to 'AI feature practicalization' (real-time translation, local document processing, AI photography, etc.).

- If NVIDIA RTX Spark receives positive market feedback at BW2026, it will accelerate personal AI PC market maturation, with global AI PC shipment share expected to rise from current 15% to 35% in 2027.

- Geopolitical risks will continue rising in 2026-2027, requiring multinational tech enterprises to establish 'dual-track supply chains' and 'regionalized data centers' to address potential technology decoupling and data localization requirements.

For CIOs and CTOs, the key decision in the current phase is establishing 'chip-agnostic' AI application architectures in multi-cloud environments, reducing dependence on specific chip platforms through containerization and abstraction layers; while closely monitoring cloud providers' self-developed chip cost-performance evolution, timely adjusting compute procurement portfolios. For investors, NVIDIA remains AI chips' 'core asset,' but moderate allocation to cloud service providers (Amazon, Microsoft, Google) and edge innovators (Apple, Huawei supply chain) is prudent to diversify technology route risks.

Why it Matters

The reshaping of cloud and edge AI chip landscapes concerns not just technology route choices but global compute sovereignty distribution. Cloud providers' self-developed chip rise is weakening NVIDIA's monopoly, while edge AI chip competition determines next-gen smart device experience definition rights. For CIOs/CTOs, this means more diversified AI infrastructure supplier portfolios; for investors, NVIDIA remains a core asset, but cloud service providers and edge innovators' allocation value is rising. Geopolitical factors will further amplify this landscape's uncertainty, making 'chip-agnostic' AI architectures and dual-track supply chains mandatory for enterprise customers.

DECISION

【CIO/CTO Recommendations】

- Architecture: Establish chip-agnostic AI application architectures in multi-cloud environments, reducing platform dependency through Kubernetes and ONNX Runtime abstraction layers.

- Procurement: Adopt 'NVIDIA GPU primary + cloud provider self-developed chips secondary' hybrid strategy, deploying standardized inference workloads on Trainium/TPU for TCO optimization.

- Compliance: For China-market AI applications, evaluate Huawei Ascend and Kirin ecosystem applicability; establish regionalized compute deployment for data localization requirements.

【Investor Recommendations】

- Core position: Maintain NVIDIA (NVDA) overweight, but shift from 'absolute concentration' to 'core + satellite' strategy.

- Satellite allocation: Overweight Amazon (AMZN) and Microsoft (MSFT), benefiting from self-developed chip TCO optimization and AI service revenue growth.

- Thematic investment: Focus on edge AI chip supply chain (Apple supply chain, TSMC advanced packaging equipment) and geopolitical beneficiaries (domestic substitution theme).

PREDICT

【3 months】After NVIDIA RTX Spark launch at BW2026, AI PC concept gains capital market enthusiasm, related supply chain (memory, cooling, power) sees thematic rallies.

【6 months】AWS Trainium 3 instances achieve large-scale commercial use, inference costs 30-40% lower than GPU instances, driving more enterprise customers to try self-developed chip solutions.

【12 months】Apple M7 and Huawei Kirin 2026 form 'duopoly' in edge AI benchmarks, forcing Qualcomm and MediaTek to accelerate edge NPU upgrades.

【18 months】If US-China tech decoupling intensifies, global AI chip market may form 'dual-track system': US camp centered on NVIDIA/TSMC, China camp centered on Huawei/SMIC, with rising technical standards and market access barriers.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)