Chip Industry Price Surge and Supply Shortage: Industry Landscape Evolution

I. Event Recap: Four Signals Reveal Structural Supply Shortages

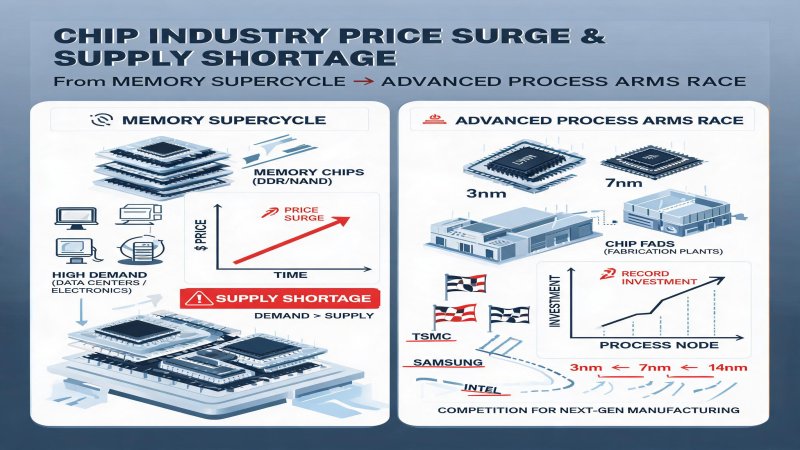

June 30, 2026, witnessed a rare "multi-point resonance" of price hike signals across the chip industry value chain — from upstream memory to midstream foundries to downstream terminal modules.

AMD Graphics Card Price Increase: Channel source Bolangtang revealed on June 30 that AMD formally notified AIB partners of a 10% price increase for GPU+GDDR bundled kits, effective July 2026. NVIDIA simultaneously raised kit costs for GeForce RTX 5090 and 5090D v2 cards.

NVIDIA Legacy GPU Revival: On June 30, Newegg listed Gigabyte RTX 3060 12GB cards — the model's first return after five years of discontinuation. German retailers also began selling RTX 3060 cards from ASUS, Gigabyte, MSI, and others. This seemingly contradictory "reverse move" reflects capacity reallocation under supply constraints.

TSMC Target Price Upgrade: Morgan Stanley raised TSMC's target price by 12% to NT$2,888 on June 30, citing improved revenue and pricing prospects. TSMC continues to benefit from strong AI chip demand with high advanced-process utilization.

Qualcomm 2nm Chip Announcement: Qualcomm announced Snapdragon Summit 2026 for September 22, expected to launch the Snapdragon 8 Elite Gen 6 series on TSMC's 2nm process — Android's first mass-produced 2nm mobile processor, with Xiaomi 18 series likely debuting it.

These four signals collectively point to one conclusion: AI demand is driving a profound "structural reallocation" of global chip capacity.

II. Technical Depth: The HBM-Advanced Process-Mature Process Triangle

The chip supply shortage is not simply "insufficient capacity" but rather "structural capacity misallocation" triggered by AI demand.

HBM Squeezing GDDR and DDR Capacity. AI training demand for HBM (High Bandwidth Memory) is growing exponentially. A single NVIDIA B200 GPU requires 8 HBM3E chips (24GB each, >4.8TB/s total bandwidth). Traditional GDDR6 bandwidth is less than 1/10 of HBM. Samsung, SK Hynix, and Micron have redirected over 40% of advanced memory capacity to HBM lines. This creates two chain reactions: GDDR shortages driving graphics card price hikes, and DDR5 capacity squeeze pushing PC/server memory prices higher.

The 2nm Advanced Process Arms Race. Qualcomm's rush to 2nm first reflects intensifying competition for mobile flagship process nodes. Apple A19 Pro, Qualcomm Snapdragon 8 Elite Gen 6, and MediaTek Dimensity 9500 all plan TSMC 2nm adoption in H2 2026, yet TSMC's total 2nm output in 2026 is estimated at only 150,000 wafers/month.

The Mature Process Revival. NVIDIA's RTX 3060 revival uses Samsung's 8nm process, which faces no advanced-process capacity constraints. In the GDDR shortage environment, RTX 3060's 14-15Gbps GDDR6 memory is relatively accessible and cost-controllable. Steam data shows RTX 3060 remains the world's most popular gaming GPU, indicating genuine mid-market demand.

III. Financial Logic: How Price Surges Reshape Profit Distribution

The chip price surge is profoundly reshaping value chain profit distribution.

TSMC: The Ultimate Validation of Pricing Power. Morgan Stanley's 12% target price increase reflects confidence in TSMC's earnings trajectory. TSMC's A14 and A13 processes lead the industry, serving major AI chip designers globally. Revenue is expected to grow double digits in 2026, with gross margins near 60%. Crucially, TSMC is transitioning from "per-wafer pricing" to "per-wafer + per-performance pricing" — charging an "AI premium" for high-performance computing chips.

Memory Makers: HBM as the Profit Engine. SK Hynix's 2025 HBM revenue exceeded 50% of total memory revenue, with gross margins far exceeding traditional DRAM. Samsung and Micron are also accelerating HBM expansion, but capacity ramp-up takes time.

Graphics Card Makers: Cost Pressure Transmission. AMD and NVIDIA's simultaneous 10% kit price increases compress AIB partners' (ASUS, Gigabyte, MSI) margins. These partners face a dilemma: absorb costs (hurting profits) or raise retail prices (hurting volumes).

Terminal Brands: Further Margin Compression. For downstream OEMs, chip price hikes mean squeezed margins or higher retail prices. Apple and Samsung can absorb costs through brand premiums, but smaller Android OEMs face existential pressure. Qualcomm's 2nm chip launch prices are expected to rise 15-20% over the previous generation, potentially pushing H2 2026 Android flagship ASPs above $800.

IV. Strategic Depth: How AI Demand Reshapes Global Chip Industry Structure

Supply Chain Diversification and New Data Security Risks. The June 30 Apple-Tata Electronics data breach revealed new supply chain risks amid diversification (India-produced iPhones estimated at 26% of global output). Tata's systems were compromised by ransomware, stealing 200,000+ files totaling 630GB, including Apple and Tesla component designs. Supply chain resilience now requires not just geographic diversification but synchronized information security upgrades.

Geopolitics and Capacity Layout. TSMC's Arizona, Kumamoto, and Dresden fabs are critical to global AI chip supply stability. The US CHIPS Act subsidies are attracting Samsung and TSMC to build in America, but costs and talent gaps remain challenges. China's domestic substitution (SMIC, YMTC) is accelerating but still faces equipment and material bottlenecks at advanced nodes.

The Strategic Significance of "Mature Process Revival". As advanced processes are consumed by AI chips, mature processes (28nm+) are gaining new strategic value. Automotive chips, industrial control, and IoT devices have stable, growing demand for mature processes. TSMC, UMC, and SMIC are all increasing mature-process investments. NVIDIA's RTX 3060 revival signals that filling market gaps with mature-process products is a pragmatic strategy under supply constraints.

V. Challenges and Risks Behind the Price Surge

Risk 1: AI Demand Bubble and Inventory Cycle. Current AI chip demand growth partly stems from large model training capex races. If AI commercialization underperforms (e.g., enterprise AI adoption slows), an inventory correction cycle similar to 2022-2023 could occur. HBM and advanced-process overcapacity would then be more painful than shortages.

Risk 2: Geopolitical Supply Chain Disruption. Escalating US-China tech decoupling could interrupt key equipment (EUV lithography) and material supplies. ASML's High-NA EUV machines are essential for 2nm and below — any export control escalation would shock global chip supply.

Risk 3: Survival Crisis for Smaller Players. Chip price hikes hit downstream smaller manufacturers hardest. White-label phone makers, mid-size PC vendors, and IoT device makers without brand premiums may face direct losses from rising chip costs, accelerating downstream consolidation.

Risk 4: Data Breach Chain Reactions. The Apple-Tata breach involved not just iPhone 18 Pro files but also TSMC and Qualcomm supply chain documents. Such incidents may trigger client trust crises, prompting leading vendors to tighten supplier准入 standards and increase compliance costs.

VI. Conclusion: Industry Evolution and Investment Perspective

The four chip industry signals on June 30 — AMD/NVIDIA graphics card price hikes, NVIDIA legacy GPU revival, Qualcomm 2nm announcement, and TSMC target price upgrade — collectively point to one core conclusion: AI demand is driving a profound structural reallocation of global chip capacity.

Investment Perspective:

- TSMC (Overweight): Advanced-process monopoly is unshakable; "AI premium" pricing will significantly boost profitability. Key variable: 2nm capacity ramp speed.

- SK Hynix / Micron (Overweight): HBM is the "oil" of the AI era; supply-demand imbalance persists at least through 2027.

- NVIDIA (Hold): AI chip ecosystem dominance is solid, but monitor Blackwell capacity release and antitrust regulatory risks.

- AMD (Hold): Graphics card price hikes improve GPU margins, but high-end AI chip market share remains far behind NVIDIA.

- Upstream Equipment/Materials (Overweight): ASML, Applied Materials, and packaging material suppliers benefit most stably from the supercycle.

Forward Outlook:

- Price hikes will persist through H1 2027, with GDDR shortages particularly severe.

- "Mature process revival" becomes a sustained trend.

- Chip designers' gross margin divergence intensifies.

- Supply chain security investment increases significantly.

Why it Matters

Chips are the foundational infrastructure of the AI era, and the current price surge represents structural transformation rather than cyclical fluctuation. AI training's explosive HBM demand (each B200 GPU requires 8 HBM3E chips) is reshaping the memory landscape. TSMC's 2nm capacity of only 150,000 wafers/month must satisfy Apple, Qualcomm, and MediaTek flagship demand — "securing capacity" is more urgent than "securing customers." For supply chain decision-makers, dual-sourcing strategies and supplier security audits are becoming essential. For investors, "pick-and-shovel" plays (ASML, SK Hynix) offer more stable returns than "gold miners" (terminal brands).

DECISION

- For chip procurement: Immediately establish dual-sourcing strategies, locking capacity quotas with at least two suppliers each for advanced (3nm and below) and mature (12nm and above) processes.

- For CIOs/CTOs: Integrate supply chain data security audits into vendor assessments. Require core suppliers to provide ISO 27001 certification and zero-trust architecture deployment proof.

- For terminal brands: Lock chip purchase orders 6-12 months in advance, consider securing capacity through prepayments, and evaluate mature-process alternatives.

- For investors: Overweight HBM/advanced memory (SK Hynix, Micron), foundry (TSMC), and upstream equipment (ASML). Underweight downstream terminal brands with thin margins and weak bargaining power.

PREDICT

- Within 12 months: GDDR shortages will drive a second round of graphics card retail price increases in Q3-Q4 (5-10%). TSMC 2nm utilization will remain above 100%, with customers needing 9-12 month advance bookings.

- Within 2 years: Mature process (28nm+) utilization will rise from current 75% to above 90%, becoming the primary supply source for automotive and IoT chips. HBM4 will reach mass production with 48GB per chip.

- Within 3 years: Global chip industry will form a "dual-track" structure — advanced processes (3nm and below) shared among TSMC, Samsung, and Intel; mature processes dominated by mainland China (SMIC, HHGrace) and Taiwan (UMC, Vanguard). Supply chain security investment will represent 5-8% of chip vendor operating costs.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)