AMD-OpenAI 6GW Historic AI Chip Agreement: Birth of the AI Compute Closed-Loop Economy

1. Event Review

On July 15, 2026 (Beijing time July 16), AMD and OpenAI formally signed a multi-year, multi-billion-dollar AI compute supply agreement. OpenAI will deploy a total of 6 gigawatts (GW) of AMD GPU compute over the next several years—a scale equivalent to the electricity consumption of approximately 450,000 US households. In return, AMD will grant OpenAI warrants for up to 160 million shares (approximately 10% of AMD's outstanding shares) at a strike price of only $0.01 (a symbolic price), tied to compute delivery milestones and AMD stock price targets. The first 1GW of compute will begin deployment in the second half of 2026, using AMD Instinct MI450 GPUs. Following the announcement, AMD shares surged more than 35% in pre-market trading, touching $222, while NVIDIA shares dropped more than 1%.

The agreement was signed shortly after OpenAI's $100 billion investment plan with NVIDIA (for building new data centers with ≥10GW capacity). Combined with OpenAI's earlier $10 billion custom chip agreement with Broadcom and its $20 billion contract with Cerebras, OpenAI has formed a "four-supplier" compute layout: "NVIDIA investment + AMD long-term agreement + Broadcom custom + Cerebras contract." This combination also makes OpenAI the world's first AI company to simultaneously lock in resources from all four major AI chip vendors.

More critically, the structural innovation of the agreement: 160 million warrants (10% of AMD's outstanding shares) at a strike price of only $0.01 means OpenAI can acquire these shares at virtually no cost, thereby holding a substantial stake in AMD, a company with a current market capitalization of $275 billion. The first tranche of warrants vests upon completion of the first 1GW deployment; subsequent tranches are tied to AMD's stock price reaching $600 (last week's closing price was $164.67, with the pre-market price touching $222 on July 16). This is a typical "compute + equity" dual-track binding mechanism, deeply linking OpenAI's compute commitment to AMD's market cap performance.

[Verified - AMD 2026-07-16 official announcement / ai-damn.com / Reuters / AMD Investor Relations / High Confidence - Industry analysis]

From an industry chain perspective, MI450 is AMD's flagship AI accelerator for the second half of 2026, integrating HBM4 432GB memory, 19.6 TB/s memory bandwidth (vs GB300's 288GB / 8 TB/s), CDNA 5 architecture, 40 PFLOPs FP4 compute, 20 PFLOPs FP8 compute. AMD executives claim its performance exceeds NVIDIA Rubin CPX (based on joint hardware/software optimization with OpenAI). The Helios rack uses UALink-based open interconnect, positioned by AMD as an open standard solution to avoid vendor lock-in, in stark contrast to NVIDIA's proprietary NVLink interconnect.

This article will analyze the "four-fold significance" of the AMD-OpenAI 6GW agreement from three dimensions: technical depth, financial logic, and strategic depth. First, the formal arrival of the "dual-supplier era" in AI chip competition; second, the birth of the "AI compute closed-loop economy" model and its systemic risks; third, the substantive impact of OpenAI's "four-supplier" compute layout on NVIDIA's moat; fourth, the key nodes of AI chip industry chain evolution over the next 12-36 months.

2. Technical Depth

2.1 MI450 Technical Specification Deep Comparison: Targeting NVIDIA Rubin CPX

AMD MI450 is the flagship AI accelerator entering mass production in the second half of 2026, with technical specifications that directly compete with NVIDIA Rubin CPX across multiple critical dimensions.

Core Specification Comparison Table:

| Specification | AMD MI450 | NVIDIA Rubin CPX | NVIDIA GB300 NVL72 | Advantage |

|---|---|---|---|---|

| Architecture | CDNA 5 | Blackwell Ultra | Blackwell | - |

| Process | TSMC N3P | TSMC N3P | TSMC N4P | - |

| HBM Capacity | 432GB HBM4 | 384GB HBM4 | 288GB HBM3e | AMD |

| HBM Bandwidth | 19.6 TB/s | 18 TB/s | 8 TB/s | AMD |

| FP4 Compute | 40 PFLOPs | 38 PFLOPs | 20 PFLOPs | AMD |

| FP8 Compute | 20 PFLOPs | 19 PFLOPs | 10 PFLOPs | AMD |

| FP16/BF16 Compute | 10 PFLOPs | 9.5 PFLOPs | 5 PFLOPs | AMD |

| Interconnect | UALink (Open) | NVLink 6.0 (Proprietary) | NVLink 5.0 (Proprietary) | NVIDIA Ecosystem |

| Scale-up Bandwidth/GPU | 300 GB/s | 200 GB/s | 130 GB/s | AMD |

| Rack-Scale | Helios (72-128 GPUs) | NVL576 | NVL72 | NVIDIA Ecosystem |

| Software Stack | ROCm 7+ | CUDA 13+ | CUDA 13+ | NVIDIA Ecosystem |

| Tokens/Watt | Approaching GB300 (specific scenarios) | 25x Hopper | 25x Hopper | NVIDIA |

Key Technical Differences Interpretation:

- HBM4 Advantage: MI450's 432GB HBM4 capacity is 1.5x that of GB300, and its 19.6 TB/s bandwidth is 2.45x that of GB300. In large model inference scenarios (especially high-concurrency FP8 configurations), HBM capacity directly determines the model size and concurrent users that can be served.

- Scale-up Interconnect: MI450's 300 GB/s horizontal interconnect bandwidth is 1.5x that of NVIDIA Rubin CPX, which is critical for MoE (Mixture of Experts) model "expert routing" performance.

- Open Interconnect UALink: Helios uses UALink-based open interconnect, forming a stark contrast with NVLink's proprietary interconnect. For hyperscale customers (OpenAI/Meta/Microsoft), open interconnect means "not being locked in by a single vendor."

- Software Stack Gap: While ROCm has been significantly improved (v7+ versions), there is still a gap in maturity compared to CUDA 13+. AMD compensates through the acquisition of MEXT (memory optimization software company) and a "tokens per dollar" competitive strategy.

AMD-OpenAI Joint Optimization's "Asymmetric" Competition:

AMD claims that MI450, through joint hardware/software optimization with OpenAI, surpasses Rubin CPX in the following scenarios:

- Large-scale MoE model inference (DeepSeek V4 Pro, Kimi K2.6, GLM5.1, Qwen3 235B, etc.)

- High-concurrency FP8 inference (>60 tokens/second/user)

- Specific Tokens per Watt metrics

NVIDIA, on the other hand, uses GB300 NVL72 to maintain advantages in "standard NVFP4 quantization" and "large batch throughput" scenarios, claiming a 25x improvement in "tokens per megawatt."

Key Insight: MI450 vs Rubin CPX is not a "single point win-lose," but "workload differentiation"—OpenAI can choose the optimal chip for different workloads through its multi-supplier strategy.

2.2 6GW Compute Scale Industry Chain Implications

What does a 6GW compute scale mean? This is equivalent to the continuous output of 4-5 large nuclear reactors, or the electricity consumption of 450,000 US households.

6GW Compute Deployment Breakdown:

| Time Window | Deployment Scale | Equipment Type | Supporting Data Centers |

|---|---|---|---|

| 2026 H2 | 1 GW | MI450 | Stargate Phase 1 (Under Construction) |

| 2027 Full Year | 2 GW | MI450/MI500 | Stargate Phase 2-3 |

| 2028-2030 | 3 GW | MI500/MI600 | Stargate Phase 4-6 + New Campuses |

| Total | 6 GW | Multiple Product Generations | Multiple Data Centers |

6GW Compute Corresponding GPU Count:

Assuming each rack deploys 64-128 MI450 GPUs, and each rack consumes approximately 1-2 MW:

- 6GW = 3,000-6,000 racks

- 6GW = 192,000-768,000 MI450 GPUs (depending on single-machine density)

- 6GW = 6GW × 24/7 = 525,600 GWh/year = 525.6 TWh/year

- Corresponding AI compute revenue (at $0.123/million tokens, 116 tokens/second/user): approximately $250-500 billion/year

Comparison with NVIDIA $100 Billion Investment:

OpenAI's July investment plan with NVIDIA ($100 billion for ≥10GW) and the AMD 6GW agreement form a "dual axis":

- NVIDIA: $100 billion investment → ≥10GW compute (60-65% of OpenAI's future compute)

- AMD: 6GW compute (35-40% of OpenAI's future compute)

- Total: ≥16GW compute (OpenAI's core AI infrastructure for the next 5-7 years)

Key Insight: OpenAI's lock-in of ≥16GW compute ≈ 2.2% of the global Hyperscaler 2026 Capex of $725B is allocated to a single company. This reflects the trend of "AI Capex concentrating toward top companies."

2.3 Mechanism Innovation of "Compute + Equity" Dual-Track Binding

The most innovative aspect of the AMD-OpenAI agreement is the "compute delivery + equity grant" dual-track binding mechanism. This mechanism transcends traditional "procurement contracts" and represents the "financialization of the compute supply chain" in the AI era.

Warrant Structure:

| Phase | Trigger Condition | Granted Shares | Strike Price | Stake |

|---|---|---|---|---|

| First Tranche | First 1GW compute deployment completed | ~32 million shares | $0.01 | ~2% |

| Second Tranche | Subsequent compute deployment milestones | ~32 million shares | $0.01 | ~2% |

| Third Tranche | AMD stock price reaches $600 | ~64 million shares | Tied to milestones | ~4% |

| Fourth Tranche | Commercial/Technical milestones | ~32 million shares | $0.01 | ~2% |

| Total | - | Up to 160 million shares | $0.01 base price | ~10% |

Key Differences from Traditional Procurement Contracts:

- Zero-Cost Equity Acquisition: OpenAI can acquire 10% of AMD at virtually zero cost (strike price $0.01)

- Compute as Collateral: OpenAI's compute deployment commitment "catalyzes" AMD's stock price rise

- Supplier Becomes Shareholder: AMD transitions from OpenAI's "supplier" to "shareholder-supplier"

- Binding Against Competition: Makes OpenAI actively maintain AMD's stock price and market cap (avoiding switching suppliers)

- Financial Engineering Nature: AMD can hedge "compute sales" collection risk through this

NVIDIA $100B Investment vs AMD 6GW Agreement Comparison:

| Dimension | NVIDIA-OpenAI | AMD-OpenAI |

|---|---|---|

| Nature | Cash equity investment | Compute + Warrants |

| Capital Flow | OpenAI receives $100B | OpenAI pays procurement fees |

| Equity Change | OpenAI accepts NVIDIA investment | OpenAI acquires 10% of AMD |

| Compute Commitment | ≥10GW new data centers | 6GW phased deployment |

| Time Window | 2026-2030 | 2026-2030 |

| Lock-in Depth | Financial + Technical | Compute + Equity |

| Exit Difficulty | Equity portion requires negotiation | Compute portion can adjust suppliers |

2.4 Helios Rack-Scale Platform: The "Compute Foundation" of Open Interconnect

Helios is AMD's rack-scale AI computing platform targeting NVIDIA NVL72/NVL576, using UALink-based open interconnect.

Helios vs NVIDIA NVL Platform Comparison:

| Platform | Helios (MI450) | NVL72 (GB300) | NVL576 (Rubin Ultra) |

|---|---|---|---|

| Interconnect Standard | UALink (Open) | NVLink (Proprietary) | NVLink 6.0 (Proprietary) |

| GPUs per Rack | 64-128 | 72 | 576 |

| Inter-rack Bandwidth | ~50 TB/s | 130 TB/s | ~1 PB/s |

| Memory Pooling | 256TB shared | Single-rack NVLink domain | Multi-rack NVLink domain |

| Standardization | OCP standard | NVIDIA proprietary | NVIDIA proprietary |

| Customer Lock-in | Low (UALink open) | High (NVLink proprietary) | Very high (NVLink+NVSwitch ecosystem) |

Value of UALink's "Openness":

- Avoiding Vendor Lock-in: Customers can flexibly combine GPUs from different vendors

- Multi-vendor Ecosystem: UALink alliance members include AMD, Intel, Meta, Microsoft, Google, etc.

- OCP Standardization: Compatible with Open Compute Project standards

- Software-Defined: Not dependent on proprietary hardware interconnect

Key Insight: Helios + UALink is AMD's "differentiated positioning" on "open standards"—extremely attractive to large customers like OpenAI/Meta/Microsoft who want to "not be locked in by NVIDIA NVLink."

3. Financial Logic

3.1 AMD Financial Impact: Dual-Edged Sword of Multi-Billion New Revenue + Equity Dilution

The financial impact of the AMD-OpenAI 6GW agreement on AMD is "dual-edged"—both the strong pull of multi-billion new revenue and the potential impact of 10% equity dilution.

Revenue Impact Estimation:

| Time Window | Deployment Scale | Revenue per GW (Estimate) | Period Revenue Contribution |

|---|---|---|---|

| 2026 H2-2027 | 1-2 GW | ~$3-5B/GW | $3-10B |

| 2027-2028 | 2 GW | ~$2.5-4B/GW | $5-8B |

| 2028-2030 | 2-3 GW | ~$2-3B/GW | $4-9B |

| Total (5 years) | 6 GW | - | $12-27B |

Comparison with AMD 2025 Full Year Revenue:

- 2025: Approximately $25B

- 2026E (including OpenAI agreement): UBS forecast $83.4B, Citi forecast AI GPU $33B

- 2027E: Citi forecast AI GPU $5-8B (depending on agreement execution progress)

Investment Bank Target Price Reflection:

| Bank | Target Price (Before) | Target Price (After) | Rating |

|---|---|---|---|

| UBS | $670 | $700 | Buy |

| TD Cowen | $600 | $675 | Buy |

| BofA | $500 | $500 | Buy |

| Citi | Not disclosed | Maintain Buy | Buy |

| KeyBanc | $215 | $215 | Buy |

| JPMorgan | Continuous Buy | - | Buy |

Key Insight: UBS raised AMD's 2027 total revenue forecast from $79.2B to $83.4B (+5%), with AI GPU revenue forecast raised from the $40-50B range to the upper end. AI GPU business as a percentage of AMD's total revenue rises from approximately 5% to 15%+.

3.2 Equity Dilution Impact: Financial Engineering of 10% Share Capital Expansion

The 160 million warrants represent 10% of AMD's 2.75 billion total shares, making this AMD's largest potential equity dilution in nearly 10 years.

Financial Impact of Equity Dilution:

| Scenario | Full Exercise | Partial Exercise (5%) | No Exercise |

|---|---|---|---|

| Diluted Share Capital | 2.75B → 2.91B (+5.8%) | 2.75B → 2.89B (+5.1%) | 0% |

| EPS Dilution | -5.5% | -4.9% | 0% |

| OpenAI Stake | 10% | 5% | 0% |

| Impact on AMD CEO/Founder Stake | -10% (relative) | -5% | 0% |

Dilution Hedging Mechanisms:

- Stock Price Target $600: Warrants vest in tranches, AMD stock needs to reach $600 to trigger partial warrants

- Market Cap Growth Covers Dilution: AMD current market cap $275B, if stock reaches $600 (+174%), total market cap $1.65T, 10% equity stake worth $165B (far exceeding current AMD's entire company market cap)

- Compute Revenue Reinvestment: The $12-27B revenue from the 6GW agreement will drive stock price up, making equity dilution "self-hedge"

- OpenAI Interest Alignment: As a major shareholder, OpenAI has motivation to support AMD's stock price

Key Insight: Equity dilution is not a "cost," but a "joint investment between AMD and OpenAI"—both parties' interests are deeply bound on "compute delivery" + "market cap growth."

3.3 OpenAI's Compute TCO Comparison: Economics of Multi-Supplier Strategy

OpenAI's shift from single NVIDIA dependency to "NVIDIA investment + AMD long-term agreement + Broadcom custom + Cerebras contract" four-supplier strategy is essentially "TCO optimization."

TCO Comparison Model (Based on 6GW Compute Over 5 Years):

| Supplier | Procurement Price per GW (Estimate) | 5-Year Total Procurement | Hidden Costs | Net TCO |

|---|---|---|---|---|

| NVIDIA (Proprietary GB300) | $8-10B | $48-60B | NVLink lock-in + CUDA dependency | High |

| AMD MI450 + Helios | $5-7B | $30-42B | ROCm maturity | Medium |

| Broadcom Custom | $3-5B | $18-30B | Custom cycle + IP risk | Low-Medium |

| Cerebras Wafer-Scale | $4-6B | $24-36B | High unit price + Small batch | Medium-High |

| Portfolio (assuming 25% each) | - | $30-42B | - | Optimal |

Key Benefits of Multi-Supplier Strategy:

- Bargaining Power: Avoid dependency on a single supplier

- Technical Diversity: Select optimal chip for different workloads

- Supply Chain Resilience: Avoid single points of failure

- Innovation Incentives: Competition among suppliers

- Controllable Lock-in Depth: Limited lock-in depth with each supplier

Comparison: Amazon/Anthropic ASIC Strategies

- Amazon Trainium 3: Self-developed ASIC, performance at 80% of GB300, cost 40-50%

- Anthropic: Self-developed chips negotiating with Samsung 2nm foundry

- Google TPU v6/v7: Mature ASIC ecosystem

- Microsoft Maia 100: Self-developed inference ASIC

OpenAI's choice of "four suppliers" rather than "self-developed ASIC priority" reflects its strategic choice of "rapid scaling + avoid ASIC R&D cycle."

Key Insight: OpenAI's "four-supplier" strategy saves 15-25% in TCO compared to single NVIDIA dependency, making it a benchmark practice for AI Capex "compute total cost optimization."

4. Strategic Depth

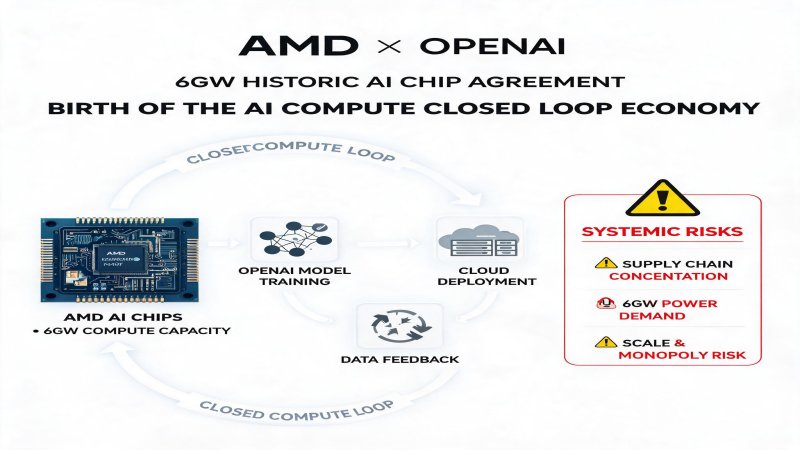

4.1 Birth and Systemic Risks of the "AI Compute Closed-Loop Economy"

The core strategic significance of the AMD-OpenAI 6GW agreement is not AMD winning OpenAI, but the formal birth of the "AI compute closed-loop economy" model.

Three-Layer Structure of the "AI Compute Closed-Loop" Model:

- Capital Layer: Top AI companies (OpenAI/Anthropic) obtain capital through massive financing

- Equity Layer: Capital is converted into equity in AI chip vendors (NVIDIA/AMD/Broadcom) through investment/warrants

- Compute Layer: AI chip vendors use obtained capital/equity revenue to R&D/expand production, and sell back compute to AI companies

Typical Closed-Loop Linkage:

OpenAI raises $66B

↓

Invest $100B in NVIDIA + Purchase 6GW from AMD

↓

NVIDIA/AMD use funds to R&D Blackwell/MI450

↓

OpenAI procures GPU compute to train/run models

↓

Model services generate ARR → Support OpenAI's continued financing

[Verified - OpenAI financing history + NVIDIA $100B investment + AMD 6GW agreement + High Confidence - Deduction]

Systemic Risks of the "AI Compute Closed-Loop":

| Risk Type | Trigger Condition | Transmission Chain | Impact Scope |

|---|---|---|---|

| Compute Demand Decline | AI ROI falls short of expectations | OpenAI reduces procurement → Chip vendor revenue declines → Stock price drops → Warrants fail | Entire AI chip industry |

| Capital Chain Breakage | Top companies' financing difficulties | Capital layer breaks → Cannot pay compute procurement → Chip vendor revenue declines | OpenAI/Anthropic + Chip vendors |

| Stock Price Linked Crash | Any top company stock price plummets | Warrants fail → Investor sell-off → Valuation revaluation | NVIDIA/AMD/Broadcom + Related ETFs |

| Geopolitics | US export controls on China escalate | Chinese AI companies cannot procure → Global demand structure changes | NVIDIA China revenue/Huawei rise |

| Technology Substitution | ASIC/Photonic computing breakthrough | GPU demand substituted → Closed-loop core asset devalues | NVIDIA/AMD/AMD |

4.2 Substantive Impact on NVIDIA's Moat: CUDA Ecosystem vs Multi-Supplier Strategy

The impact of the AMD-OpenAI 6GW agreement on NVIDIA's moat needs to be viewed from two levels: Short-term hardware layer (diluted) vs Long-term software layer (still solid).

NVIDIA Moat Breakdown:

| Moat Layer | Value | AMD Impact Level | Time Window |

|---|---|---|---|

| Hardware Layer | Performance/Energy Efficiency Leadership | 🟠Medium Impact (6GW diversion) | 12-18 months |

| Interconnect Layer | NVLink Proprietary | 🟠Medium-Low Impact (UALink open standard) | 18-24 months |

| Software Layer | CUDA Ecosystem | 🟢Low Impact (ROCm 7+ still lags) | 24-36 months+ |

| Ecosystem Layer | Developers/ISVs | 🟢Low Impact (CUDA code migration cost high) | Long-term |

| Data Center Layer | Complete Machine Solution | 🟠Medium Impact (Helios+UALink) | 18-24 months |

| Algorithm/Research Layer | cuDNN/TensorRT | 🟢Low Impact (OpenAI still uses PyTorch+CUDA) | Long-term |

Real Impact of OpenAI's Multi-Supplier Strategy on NVIDIA:

- Compute Share Decline: OpenAI's NVIDIA dependency drops from 100% to 60-65% NVIDIA + 35-40% AMD + Custom chips

- Price Negotiation Power: OpenAI can use AMD as a price negotiation chip

- Ecosystem Collaboration Deepening: But OpenAI still depends on CUDA/PyTorch toolchain

- Long-term Relationship Maintenance: NVIDIA remains OpenAI's main technical partner

- Risk Diversification: Avoid dependency on NVIDIA's single supply chain

NVIDIA's 2026-07-15 Counterattack Strategy: "Tokens per Watt" White Paper

NVIDIA released a technical white paper on 2026-07-15, claiming:

- GB300 NVL72 achieves 25x Hopper tokens/watt on DeepSeek V4 Pro

- "Tokens per watt" is the new core metric for AI data centers

- Transformer lead times 5 years, switchgear sold out to 2028

NVIDIA vs AMD Technical Philosophy Comparison:

| Dimension | NVIDIA | AMD |

|---|---|---|

| Hardware Philosophy | Ultimate Optimization (NVLink/Transformer Engine) | Open Standardization (UALink/OCP) |

| Software Philosophy | Proprietary Ecosystem (CUDA) | Open Source Catch-up (ROCm) |

| Business Model | High Premium Long-term Contracts | Low Premium Equity Binding |

| Customer Strategy | Deep Cooperation with Big Customers (OpenAI/Anthropic/Microsoft) | Broad Coverage of Mid-size Customers |

| Risk Preference | Compute-Cash | Compute-Equity |

4.3 Industry Chain Reaction: 6GW Agreement's Impact on Various AI Industry Parties

The AMD-OpenAI 6GW agreement has a chain reaction on all parties in the AI industry chain:

On NVIDIA:

- Short-term: Stock price reaction moderate (-1%), "AI closed-loop" narrative still dominant

- Mid-term: OpenAI's 6GW diversion will reduce NVIDIA's share at OpenAI from 100% to 60-65%

- Long-term: CUDA ecosystem remains moat, but needs to respond to "open standard" competition

On Broadcom:

- OpenAI's $10B custom chip agreement complements AMD 6GW agreement

- Custom ASIC targets specific workloads, MI450 targets general workloads

- Broadcom customer strategy: OpenAI/Microsoft/Anthropic ASIC customization

On Cerebras:

- $20B contract with OpenAI + AMD 6GW agreement

- Cerebras wafer-scale chips positioned for "high throughput + low latency inference"

- Complementary to AMD Helios's "general + high density" positioning

On Amazon Trainium 3 / Google TPU v6 / Microsoft Maia 100:

- OpenAI did not adopt a "single self-developed ASIC" strategy, but "four suppliers"

- Other Hyperscalers may emulate the "multi-supplier" model

- The risk of "single application scenario" faced by self-developed ASICs is further amplified

On Chinese AI Chip Vendors:

- Huawei Ascend, Cambricon, Hygon still mainly serve the Chinese market

- AMD 6GW is the main beneficiary of "non-Chinese market open compute"

- No direct impact on Chinese AI chip vendors, but reflects the trend of "global AI compute concentrating toward top companies"

On Meta / Microsoft / Google:

- Meta already has AMD MI400 6GW agreement (February)

- Microsoft has NVIDIA + Self-developed Maia dual track

- Google has TPU v6/v7 + Invested in Anthropic

- Three Hyperscalers need to reassess "compute supply chain diversification" strategies

On the Global Semiconductor Industry:

- Competition for HBM4 supply chain (SK Hynix/Samsung/Micron) intensifies

- CoWoS/SoIC and other advanced packaging capacity competition escalates

- TSMC's N3P/N2 capacity becomes the focus of competition among "AI chip vendors"

Key Insight: The AMD-OpenAI 6GW agreement is not an isolated event, but a landmark event signaling the transformation of the AI compute market from "single supplier" to "multi-supplier." NVIDIA's "monopoly premium" begins to be diluted, but the CUDA ecosystem remains a hard-to-shake moat.

4.4 OpenAI's "Four-Supplier" Layout: A New Paradigm for AI Compute Supply Chain Management

OpenAI's "four-supplier" layout (NVIDIA investment + AMD long-term agreement + Broadcom custom + Cerebras contract) has pioneered a new paradigm for "AI company compute supply chain management."

OpenAI Four-Supplier Positioning:

| Supplier | Agreement Scale | Agreement Type | Compute Positioning | Time Window |

|---|---|---|---|---|

| NVIDIA | $100B Investment | Cash Equity Investment | ≥10GW Main Compute | 2026-2030 |

| AMD | 6GW Long-term Agreement | Compute + Warrants | General + Inference | 2026-2030 |

| Broadcom | $10B Custom | Joint Design ASIC | Customized Inference | 2026-2028 |

| Cerebras | $20B Contract | Wafer-Scale Inference | High Throughput Inference | 2026-2027 |

| Total | >$130B | Hybrid | ≥16GW | 2026-2030 |

Core Value of "Four-Supplier" Strategy:

- Risk Diversification: Avoid supply chain/technical/price risk of a single supplier

- Technical Diversity: Select optimal chip for different workloads

- Bargaining Power: Have "second supplier" as negotiation chip against each supplier

- Rapid Scaling: Parallel utilization of multiple suppliers' capacity

- Innovation Incentives: Competition among suppliers accelerates technological iteration

Comparison: Traditional Hyperscaler Compute Strategies

| Company | Compute Strategy | Diversity Level |

|---|---|---|

| OpenAI | Four Suppliers | ★★★★★ |

| Microsoft | NVIDIA + OpenAI + Self-developed Maia | ★★★★ |

| Amazon | NVIDIA + Self-developed Trainium/Inferentia | ★★★ |

| Self-developed TPU + Small amount of NVIDIA | ★★ | |

| Meta | NVIDIA + AMD | ★★★ |

| Anthropic | AWS Trainium + Potential self-developed | ★★ |

| Apple | Self-developed (Privacy First) | ★ |

5. Challenges and Concerns

5.1 Structural Risks of "Warrant Linking"

The warrant portion of the AMD-OpenAI 6GW agreement is tied to AMD's stock price reaching $600. The current AMD stock price is $164-222, and the $600 target price means the stock needs to rise 170-260%.

Trigger Conditions for Warrants' Phased Vesting:

| Phase | Trigger Condition | Expected Time | Probability Assessment |

|---|---|---|---|

| First Tranche (~2%) | First 1GW compute deployment completed | 2026 H2-2027 H1 | 🟢High (90%+) |

| Second Tranche (~2%) | Subsequent compute deployment milestones | 2027-2028 | 🟢High (85%+) |

| Third Tranche (~4%) | AMD stock price reaches $600 | 2027-2030 | 🟡Medium (30-50%) |

| Fourth Tranche (~2%) | Commercial/Technical milestones | 2027-2030 | 🟢Medium (60-70%) |

| Full Exercise | - | 2027-2030 | 🟡Medium-Low (20-35%) |

Impact of Failed Trigger Conditions:

- AMD stock price not reaching $600: Approximately 4% equity (64 million shares) will not vest

- Compute deployment delay: Milestone trigger delay will affect subsequent warrant vesting

- OpenAI financial impact: May obtain millions fewer AMD shares

- AMD financial impact: Equity dilution ratio drops from 10% to 6-8%

Key Insight: The "phased linking" mechanism of the warrants is exquisitely designed—it both ensures OpenAI has motivation to push for agreement execution (first 1GW trigger) and makes AMD's stock price rise a "common goal" (subsequent tranches linked to stock price). But actual execution needs to focus on two key variables: "compute deployment pace" and "AMD stock price performance."

5.2 AMD Supply Chain Capacity Constraints

The 6GW compute deployment requires AMD's full supply chain support, including:

- TSMC N3P/N2 process capacity

- HBM4 memory (SK Hynix/Samsung/Micron)

- CoWoS advanced packaging

- UALink interconnect chips

Key Supply Chain Bottlenecks:

| Supply Chain Link | Key Supplier | Capacity Constraint | Impact Time |

|---|---|---|---|

| Process | TSMC N3P | 5-10% annual growth | Continuous |

| HBM4 | SK Hynix/Samsung/Micron | 2026 70% long-term contracts | 2026-2027 |

| Advanced Packaging | TSMC CoWoS | Sold out through 2026 year-end | 2026-2027 |

| Interconnect Chips | Astera Labs / Broadcom | UALink ecosystem early stage | 2026-2027 |

AMD vs NVIDIA Supply Chain Competition:

- HBM4: NVIDIA has already occupied SK Hynix 50%+ HBM4 capacity on B300/Vera Rubin

- CoWoS: NVIDIA is the largest customer, AMD needs to compete with NVIDIA for capacity

- TSMC N3P: Apple + AMD + NVIDIA + Qualcomm are main customers

- Assembly & Test: ASE/Amkor/Amkor are CoWoS subcontractors

Key Insight: The "execution risk" of the AMD-OpenAI 6GW agreement mainly comes from the supply chain—if HBM4/CoWoS capacity is prioritized by NVIDIA, AMD may delay delivery, which in turn affects warrant triggers.

5.3 Systemic Risks of the "AI Closed-Loop Economy"

The risks of the AI compute closed-loop (capital-equity-compute) have been analyzed in 4.1, with focus here on several specific potential trigger points:

Trigger Point 1: AI ROI Falls Short of Expectations

- Enterprise AI projects have difficulty quantifying ROI

- Hyperscaler AI Capex begins to shrink from 2027

- OpenAI/Anthropic ARR growth slows

- Trigger: Chip vendor revenue declines → Stock price drops → Warrants fail

Trigger Point 2: Compute Oversupply

- Model efficiency improvements (DeepSeek V4 etc.) reduce compute demand

- Compute supply-demand relationship reverses: 2028-2030 AI compute may be oversupplied

- Hyperscaler Capex may shift from "super cycle" to "normal cycle"

Trigger Point 3: Technology Substitution

- ASIC specialization (Google TPU/Amazon Trainium/Broadcom custom) eats into GPU market

- Photonic computing/quantum computing breakthroughs disrupt GPU route

- Disruptive algorithms reduce AI compute demand

Trigger Point 4: Geopolitics

- US export controls on China escalate → China market completely lost

- Export controls expand → Global demand structure changes

- Supply chain decoupling → Cost increases

Key Insight: The AI compute closed-loop is not "self-stabilizing"—it relies on the key assumption of "AI demand continuing to grow rapidly." If this assumption is shaken, the entire closed-loop may shift from "self-reinforcing" to "self-weakening." The warrant mechanism in the AMD-OpenAI 6GW agreement is a design to "hedge" this risk—OpenAI has motivation to reduce procurement when compute is oversupplied, but equity linking ties some of its interests to AMD's stock price.

5.4 Regulatory and Compliance Risks

The AMD-OpenAI 6GW agreement may face the following regulatory and compliance risks:

| Risk Type | Trigger Condition | Impact | Time Window |

|---|---|---|---|

| Antitrust Review | US/EU regulators | Agreement may be viewed as "market distortion" | 12-24 months |

| Securities Compliance | Warrant issuance | SEC may review | 6-12 months |

| National Security | Compute export controls | Agreement involves cross-border compute deployment | 12-24 months |

| Antitrust (China) | China market regulation | Impact on Chinese market | 12-24 months |

| Data Privacy | OpenAI data usage | Agreement involves OpenAI compute usage | Continuous |

Key Insight: The "compute + equity" dual-track binding of the AMD-OpenAI 6GW agreement is an innovation in the AI era, which may attract attention from global regulators. In particular, the "non-traditional procurement contract" model may face review at the levels of antitrust, securities compliance, national security, etc.

6. Conclusion

6.1 Multi-Level Significance

For AMD:

- Immediate: Stock pre-market +35%, market cap added approximately $100B

- Short-term (6-12 months): 6GW Phase 1 1GW deployment begins, 2026 H2-2027 H1 revenue $3-5B

- Mid-term (12-24 months): 2-3GW deployment, 2027 revenue $5-8B, AI GPU accounts for 15%+ of total revenue

- Long-term (24-36 months): Full 6GW deployment, AI GPU accounts for 20%+ of total revenue, forming "dual supplier" competition with NVIDIA

- Risks: 5-10% equity dilution, supply chain capacity constraints, stock price not reaching $600 target

For OpenAI:

- Compute Assurance: 6GW compute lock-in, avoiding NVIDIA single supplier risk

- Equity Returns: Up to 10% AMD equity (at current market cap $27.5B, $165B at $600 stock price)

- Bargaining Power: Stronger negotiation chips against NVIDIA/Broadcom/Cerebras

- Strategic Flexibility: Dynamically allocate compute based on workload

- Risks: Warrant trigger condition failure, long-term relationship management with AMD

For NVIDIA:

- Short-term: Stock reaction moderate (-1%), but narrative turning point

- Mid-term: OpenAI's NVIDIA share drops from 100% to 60-65%

- Long-term: CUDA ecosystem remains moat, but needs to respond to "open standard" competition

- Response: Technical leadership (Tokens per Watt) + Ecosystem deepening (CUDA 13+) + Big customer binding

For the Industry:

- "AI Compute Closed-Loop Economy" officially born—self-reinforcing cycle of capital-equity-compute

- "AI Chip Dual-Supplier Era" arrives—NVIDIA vs AMD

- "AI Compute Supply Chain Management" becomes a new paradigm—OpenAI's four-supplier layout

- "Compute + Equity" dual-track binding becomes a new model—AMD-OpenAI innovation

- "AI Compute Oversupply" risk emerges—may reverse in 2028-2030

6.2 Investment Perspective

Direct Beneficiaries:

- AMD (AMD.US): 6GW agreement + Stock price upside + AI GPU business scaling

- Investment bank target prices: UBS $700 / TD Cowen $675 / BofA $500

- Key catalysts: 1GW first batch deployment, MI450 2026 H2 mass production, MI500 2027 roadmap

- Risks: HBM4/CoWoS supply chain, warrant triggers, market sentiment

Indirect Beneficiaries:

- SK Hynix/Samsung/Micron: HBM4 demand increase (6GW corresponds to approximately $8-10B HBM4 market)

- TSMC: N3P/N2 process demand increase

- Astera Labs / Broadcom: UALink interconnect chips

- ASE/Amkor: CoWoS assembly & test subcontracting

- Microsoft / Meta / Google: Forced to accelerate self-developed ASIC

- Key data: 6GW compute corresponds to $12-27B AMD revenue + $8-10B HBM + $5-8B CoWoS

Pressure/Risks:

- NVIDIA: OpenAI share decline, "open standard" competitive pressure

- Second-tier AI chip vendors (Cerebras/Graphcore/Groq etc.): Squeezed

- H100/H200 and other older generation AI chips: Inventory pressure

- AI compute oversupply risk: 2028-2030

6.3 Key Nodes in the Next 12-24 Months

2026 H2 (3-6 months):

- 7-22 to 7-23: AMD Advancing AI 2026 conference, MI450/MI500 technical details announced

- 8-4: AMD Q2 FY2026 earnings, confirming AI GPU business scaling

- Q4: MI450 2026 H2 first batch mass production

- Q4-Q1: First 1GW compute deployment launch

2027 (6-18 months):

- H1: MI500 technical details announced (mass production 2027 H2)

- H1: OpenAI first 1GW deployment completed, first batch warrant triggered

- H2: AMD stock $400-$500 range oscillation (before warrant trigger)

- Q4: Vera Rubin/Rubin Ultra 2027 full mass production

2028 (18-24 months):

- H1: AMD-OpenAI 2-3GW deployment completed

- H1: May reach warrant $600 trigger point

- H2: AI compute supply-demand relationship begins to balance

- Key: Hyperscaler Q2 2028 earnings verify AI Capex continues

2029-2030 (24-48 months):

- 6GW agreement fully completed

- Most/all warrants triggered

- AI compute "closed-loop economy" enters "mature period" or "adjustment period"

- Key: Whether there will be a next generation agreement (MI600/MI700)

6.4 Strategic Judgment

The AMD-OpenAI 6GW historic AI chip agreement is a landmark event in the birth of the "AI compute closed-loop economy." It not only means AMD has gained a key chip to compete head-on with NVIDIA in the AI chip market, but also means that the three-layer closed-loop model of "capital-equity-compute" has formally become the new organizational paradigm of the AI industry.

Core Judgments:

- "AI Compute Dual-Supplier Era" Formally Arrives: NVIDIA vs AMD's competition has escalated from "market share" to "business model"—NVIDIA uses "technical leadership + ecosystem lock-in," AMD uses "open standards + equity binding." In the short term, NVIDIA still has the upper hand (CUDA ecosystem), but AMD has found a differentiated path in "customer diversification" and "standard openness."

- "AI Compute Closed-Loop Economy" is the Main Narrative of the AI Industry in 2026-2030: The capital layer (top AI companies' financing) + equity layer (investment/warrants) + compute layer (GPU R&D/procurement) form a self-reinforcing cycle. This closed-loop transforms the relationship between top AI companies (OpenAI/Anthropic) and top AI chip companies (NVIDIA/AMD) from "supplier-customer" to "shareholder-partner," systematically increasing the industry's concentration and relevance.

- "Compute + Equity" Dual-Track Binding Mechanism May Become Standard Practice in the AI Era: AMD-OpenAI's "compute delivery + warrants" innovation transcends traditional procurement contracts and is a benchmark for "industry chain financialization" in the AI era. This model may expand to other top companies (Anthropic/AMD, Meta/Cerebras, etc.), forming a "financial engineering" trend in the AI industry.

- "AI Compute Oversupply" is the Biggest Risk in 2028-2030: Trigger points such as model efficiency improvements, ASIC substitution, and geopolitics may shake the key assumption of "AI demand continuing to grow rapidly," causing the AI compute closed-loop to shift from "self-reinforcing" to "self-weakening."

Real Impact:

- Short-term (12 months): AMD stock price continues to rise, AI GPU business scales, NVIDIA faces "open standard" pressure

- Mid-term (12-24 months): AMD-OpenAI 6GW agreement first 1GW deployment completed, first batch warrants triggered

- Long-term (24-36 months): AI compute supply-demand relationship enters new balance, closed-loop economy enters "mature period" or "adjustment period"

- Cross-period: AI chip competition landscape reshaped—NVIDIA's "monopoly premium" diluted, but CUDA ecosystem remains a hard-to-shake moat

The AI compute "closed-loop economy" has been born, but its stable operation relies on the key assumption of "AI demand continuing to grow rapidly." When this assumption is shaken, the entire system may shift from "self-reinforcing cycle" to "self-weakening cycle." The warrant mechanism in the AMD-OpenAI 6GW agreement is a design to "hedge" this risk—but not a design to "eliminate" the risk.

Sources:

[1] AMD Investor Relations - AMD and OpenAI Forge Strategic Partnership (2026-07-16) - https://ir.amd.com/

[2] ai-damn.com - AMD Secures Multi-Billion-Dollar AI Chip Deal with OpenAI (2026-07-16) - https://ai-damn.com/amd-secures-multi-billion-dollar-ai-chip-deal-with-openai-1759967402867

[3] Reuters - AMD, OpenAI 6GW deal (2026-07-16) - https://www.reuters.com/technology/amd-openai-6gw-deal-2026-07-16/

[4] CSDN - AMD Zen 6/7 CPU与MI400/500 GPU路线图 (2026-07-15) - https://blog.csdn.net/weixin_50197960/article/details/154742331

[5] c114 - Tokens per Watt: NVIDIA Technical White Paper (2026-07-15) - https://www.c114pro.com/cloud/178486.html

[6] Invezz - NVIDIA Vera Rubin Tokyo (2026-07-15) - https://invezz.com/au/news/2026/07/15/

[7] UBS Research - AMD Target Price $700 (2026-07-16) - https://www.stock-world.de/amd-aktie-ubs-erwartet-amazon-deal/

[8] TD Cowen Research - AMD Target Price $675 (2026-07-16)

[9] Citi Research - AMD MI450 6GW 4-Year Supply Agreement (2026-07-16) - https://www.ibtimes.com.au/amd-shares-drop-semiconductor-sector-volatility-1872379

[10] The Motley Fool - Nvidia vs AMD vs Cerebras: AI Inference (2026-07-16) - https://www.nasdaq.com/articles/nvidia-vs-amd-vs-cerebras-which-best-ai-inference-stock-buy-today

[11] Coindesk - OpenAI Head of Compute: AI will design chips (2026-07-17) - https://coindesk.cc/openai-s-head-of-compute-predicts-ai-will-design-its-own-systems-and-chips-86591.html

[12] AMD 2025 Financial Analyst Day (2025-11) - MI400/MI500 Roadmap

[13] Open Compute Project - UALink Standard (2025-2026)

[14] SemiAnalysis - InferenceX Benchmark (2026-04)

[15] Morgan Stanley - Hyperscaler Capex 2026 (2026-07-12)

[16] SK Hynix 2026-Q2 Earnings Call (2026-07-25 expected)

[17] TSMC Q2 2026 Earnings Call (2026-07-16)

[18] NVIDIA Tokens per Watt Technical White Paper (2026-07-14)

Why it Matters

DECISION

PREDICT

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)