I. Event Recap

In early July 2026, the global AI regulation and cybersecurity sectors witnessed multiple landmark events, revealing that the triple resonance of policy frameworks, technology evolution, and market demand is reshaping the industry landscape.

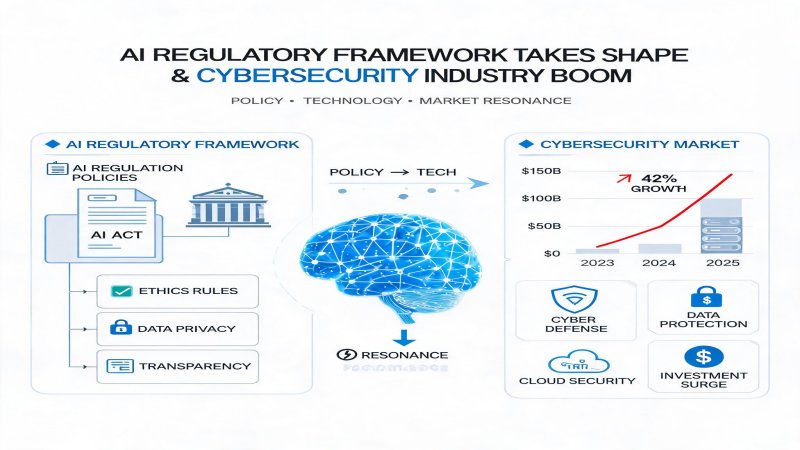

On the AI regulation front, the U.S. Department of Commerce lifted export controls on Anthropic's two top-tier models, Fable and Mythos, on July 1—less than three weeks after suspending their export citing national security risks. Meanwhile, OpenAI CEO Sam Altman was reported to have proposed offering the U.S. government approximately 5% equity in the company during early contacts with the Trump administration, hoping to share AI industry development benefits with the public and ease regulatory pressure. The Financial Times reported on July 2 that the U.S. government is conducting in-depth consultations with AI companies including OpenAI, Anthropic, and Google, planning to introduce voluntary industry standards for new model releases, with an announcement expected as early as next week.

On the cybersecurity front, Palo Alto Networks and CrowdStrike both reported record quarterly results on July 1. Palo Alto Networks Q3 revenue reached $3.0 billion, up 31% YoY, with next-generation security product ARR growing 60%, and securing a $200 million platform services order from a leading frontier AI lab. CrowdStrike reported quarterly revenue of $1.39 billion, up 26% YoY, with net new ARR of $256 million. Cisco announced a fixed biweekly security patch release schedule starting July, directly responding to the industry trend of AI-accelerated vulnerability discovery. Cloudflare announced on July 1 plans to block AI agent and training crawlers from accessing ad-supported web pages by default starting September 15, 2026.

On the geopolitical front, Microsoft announced cuts of 200-400 Azure R&D positions in China, with affected employees leaving by July 6, marking a strategic retreat by U.S. tech giants from the Chinese market. Huawei raised prices on smart terminals by 5-10% starting July 1, citing memory chip shortages and AI chip demand. Apple was reported to be in negotiations with two domestic chip vendors for procurement for the China market.

Key Timeline:

- July 1: U.S. Commerce Department lifts Anthropic Fable/Mythos export controls; Cloudflare announces AI crawler blocking plan; Palo Alto Networks and CrowdStrike report earnings

- July 2: U.S. government consults with AI companies on industry standards; Anthropic admits and removes Claude Code hidden detection code; Microsoft Azure China layoffs revealed

- July 2: OpenAI reported proposing 5% equity to U.S. government

- July 6: Deadline for affected Microsoft Azure China employees to depart

Financial Data:

- Palo Alto Networks Q3 revenue: $3.0 billion, +31% YoY; next-gen security product ARR +60%

- CrowdStrike quarterly revenue: $1.39 billion, +26% YoY; net new ARR $256 million

- Global cybersecurity software market expected to grow over 30% in 2026

- OpenAI valuation and pre-IPO equity structure facing reshaping

II. Technical Depth

The Anthropic hidden code incident reveals the cutting-edge battlefield of AI model protection technology. Reddit developers' reverse engineering analysis discovered that Anthropic embedded a detection mechanism in Claude Code starting in April: when proxy access is detected, the program checks whether the system timezone is China, whether the proxy belongs to a Chinese domain, and encodes detection results using different Unicode characters by modifying date and punctuation formats in system prompts. Anthropic engineers explained this was an anti-model-distillation experiment launched in March. Model distillation—replicating model capabilities through extensive querying—has become a core competitive issue among AI labs.

Cloudflare's AI crawler control measures represent a technical counterattack at the content distribution layer against AI data scraping. Cloudflare plans to block AI agent and training crawlers from accessing ad-supported web pages by default on September 15, 2026, categorizing crawlers with search, agent, and training labels based on behavior. Given Cloudflare's network covers approximately 20% of global websites, this policy will significantly increase AI companies' training data acquisition costs. Previously, The New York Times, Reddit, and other content platforms have filed lawsuits against OpenAI or signed paid data agreements.

Cisco's new security patch cadence is a direct technical response to AI-accelerated vulnerability discovery. As AI tools are widely used for automated vulnerability mining, the speed and volume of security vulnerability discoveries have increased significantly. Cisco announced reserving the first and third Wednesdays of each month starting July for security-hardened software releases, with 7-day advance notice of affected technologies and platforms. Recently disclosed high-severity vulnerabilities, including the Catalyst SD-WAN Manager zero-day (CVE-2026-20245) and ISE authentication exposure vulnerabilities, demonstrate that AI-driven threats against enterprise network infrastructure are escalating.

Palo Alto Networks' "Precision AI" platform and CrowdStrike's Falcon platform showcase the depth of AI application on the defense side. Palo Alto Networks' $200 million platform services order from a leading frontier AI lab proves that AI security demand has expanded from traditional network perimeters to AI model training environments. CrowdStrike's newly released Spring '26 version establishes the endpoint as the epicenter of AI security, adding AI agent discovery, shadow AI governance, and runtime threat detection capabilities.

Four-Vendor Competitive Matrix:

| Dimension | Palo Alto Networks | CrowdStrike | Cloudflare | Cisco |

|---|---|---|---|---|

| Core Positioning | AI-driven platform security | Endpoint-centric security | CDN + edge security | Network infrastructure security |

| AI Security Capability | Precision AI platform | Falcon AI security modules | AI crawler control | AI vulnerability response |

| Latest Performance | Revenue $3.0B, +31% | Revenue $1.39B, +26% | Not separately disclosed | Traditional business stable |

| Customer Acquisition | $200M AI lab platform deal | Net new ARR $256M | 20% global website coverage | Enterprise network foundation |

| Strategic Direction | Platformization + M&A | Endpoint to cloud workload expansion | Content protection + edge compute | Security patch rhythm reform |

III. Financial Logic

The outperformance of Palo Alto Networks and CrowdStrike validates the robust growth logic of AI security demand. AI is shifting cybersecurity from a post-deployment supplement to an initial planning phase for AI system deployment, with three core drivers: securing AI systems themselves, protecting new AI-spawned infrastructure (new cloud environments, data centers, GPU compute platforms), and responding to AI-driven threat evolution acceleration.

Palo Alto Networks' quarterly revenue included $388 million from acquired companies CyberArk and Chronosphere, demonstrating that platform-oriented M&A strategy is accelerating. Its next-generation security product ARR grew 60%, far exceeding overall revenue growth, indicating strong customer willingness to pay for premium AI security products. CrowdStrike's net new ARR of $256 million shows its endpoint security platform's customer stickiness continues strengthening in the AI era.

From a valuation perspective, the cybersecurity sector is demonstrating "defensive growth" characteristics amid the AI wave. When market concerns arise about AI hardware (GPU, semiconductor) ROI, cybersecurity—as a "necessary cost" of AI applications—actually sees rising demand certainty. The Jefferies CIO survey shows 95% of respondents expect 2026 cloud budgets to increase year-over-year, with cloud security being an indispensable component.

The financial logic of OpenAI's proposal to offer 5% equity to the U.S. government is equally noteworthy. Pre-IPO, OpenAI needs to build government relationships to reduce regulatory risk. If approved, this would bring the U.S. government billions in potential returns while providing OpenAI with political protection. Anthropic, Google, Meta, and other major U.S. AI companies might participate in similar arrangements, reshaping the capital structure and governance model of the AI industry.

IV. Strategic Depth

From the global AI regulatory landscape perspective, the U.S. is accelerating construction of a three-layer regulatory framework: "voluntary industry standards + export controls + government equity." The Trump administration's June executive order requires federal agencies to collaborate with leading AI developers to complete safety testing before frontier models are publicly released. This "government-business co-governance" model contrasts sharply with the EU's AI Act: the U.S. emphasizes industry self-regulation and government participation, while the EU tends toward legislative mandatory standards.

In the cybersecurity competitive landscape, industry dividends are rapidly concentrating toward leading platform vendors. Palo Alto Networks has built a full-stack security platform covering network, cloud, identity, and applications through acquisitions of CyberArk (identity security) and Chronosphere (observability). CrowdStrike leverages its leading position in endpoint detection and response (EDR) to expand into cloud workload protection and identity security.

The "data war" between content platforms and AI companies is also escalating. Cloudflare's AI crawler blocking, The New York Times' lawsuit against OpenAI, and Reddit's paid data agreement with Google all indicate that the cost of acquiring high-quality training data is rising rapidly. This is particularly detrimental to smaller AI labs and may increase industry concentration.

Geopolitical factors' impact on technology supply chains is deepening. Microsoft's Azure China layoffs of 200-400 people reflect U.S. tech giants' strategic contraction under data sovereignty, export controls, and local compliance pressures. Apple's negotiations with domestic chip vendors and Huawei's terminal price increases demonstrate Chinese enterprises' urgency regarding semiconductor supply chain autonomy.

Vendor Strategy Matrix:

| Strategic Positioning | Representative Vendors | Core Strategy | Risk Factors |

|---|---|---|---|

| AI Security Platform | Palo Alto Networks, CrowdStrike | Platform M&A + AI-native security | Integration risk, price wars |

| Edge Content Protection | Cloudflare | AI crawler control + edge security | Customer churn, false blocking |

| Network Infrastructure | Cisco | Predictable patching + zero trust | Market share erosion, legacy products |

| Regulatory Compliance | OpenAI, Anthropic | Government cooperation + industry standards | Political risk, competitive disadvantage |

V. Challenges and Concerns

While the AI regulatory framework is accelerating, it still faces numerous challenges. The voluntary industry standards planned by the U.S. government lack binding enforcement and may become mere "self-regulatory" formalism. OpenAI's proposal to offer 5% equity to the government, if approved, could spark major controversies regarding government interference in corporate innovation, cronyism, and fair competition. The more fundamental question is how to safeguard national security without stifling technological innovation—overly strict export controls may force restricted countries to accelerate self-developed alternatives, ultimately weakening U.S. technological leadership.

The cybersecurity industry's rapid growth also carries hidden concerns. Palo Alto Networks and CrowdStrike's high valuations already fully reflect expectations of AI security demand growth; any slowdown in performance could trigger sharp corrections. Additionally, the "arms race" between AI-driven automated attacks and AI-driven automated defenses may lead to declining security spending efficiency—enterprises may fall into a "buying for buying's sake" trap while actual security posture fails to improve correspondingly.

Cloudflare's AI crawler blocking strategy, while protecting content creators' rights, may also inadvertently harm legitimate search engine crawlers and research-purpose crawlers. A more profound impact is that if mainstream CDN vendors universally adopt similar measures, AI model training data quality may decline, subsequently affecting model performance.

The cost escalation from geopolitical decoupling cannot be ignored. Huawei's terminal price increases of 5-10% are just the tip of the iceberg; the regionalization of global semiconductor supply chains is driving up overall manufacturing costs. For multinational enterprises, maintaining compliant "China versions" and "international versions" of technology stacks will continue increasing costs.

VI. Conclusion

From an investment perspective, the AI regulation and cybersecurity track is in a "policy catalyst + demand explosion" double-click window. The strong performances of Palo Alto Networks and CrowdStrike are not isolated events but early signals of structurally rising AI security demand. Leading platform vendors with full-stack coverage can convert short-term demand urgency into long-term stable revenue by increasing customer switching costs.

In the near term, the cybersecurity sector carries a higher certainty premium relative to AI hardware. When market concerns about compute oversupply emerge (such as the Micron and SanDisk price crashes triggered by Meta's compute sales plans), cybersecurity—as a "mandatory cost" of AI applications—will demonstrate more prominent defensive characteristics.

Over the medium term, the speed at which the AI regulatory framework takes shape will directly impact industry development pace. If the U.S. government can issue clear industry standards within the next 3-6 months, it will provide AI companies with predictable compliance paths and reduce regulatory uncertainty. Conversely, vague or contradictory regulatory signals may suppress corporate innovation and investment willingness.

Forward-looking judgment: Over the next 12-24 months, the AI security market will rapidly evolve from "point solutions" (endpoint, network, and cloud operating independently) to "unified platforms." Vendors capable of providing full-lifecycle AI security protection—"prevention, detection, response, and recovery"—on a single platform will gain decisive competitive advantages. Meanwhile, the博弈 between content protection and AI data acquisition will spawn new business models—"Data Licensing as a Service" may become the next high-growth niche segment.

Why it Matters

AI regulation and cybersecurity are forming a triple resonance of policy, technology, and market. The U.S. government is accelerating a three-layer regulatory framework of voluntary standards, export controls, and government equity, which will reshape AI industry competition rules within 3-6 months. Meanwhile, strong performances by Palo Alto Networks and CrowdStrike prove AI security demand has shifted from 'optional' to 'mandatory'—three drivers propel structural enterprise security budget increases: AI system security itself, protection of AI-spawned infrastructure, and response to AI-driven threats. Cloudflare's AI crawler blocking marks a new phase in the 'data war' between content platforms and AI companies, with high-quality training data acquisition costs rising significantly, potentially increasing industry concentration.

DECISION

For CISOs/security decision-makers: 1) Prioritize evaluating unified AI security platforms (e.g., Palo Alto Networks Precision AI, CrowdStrike Falcon) ROI over continued point solution procurement; 2) Complete security assessments before AI system deployment, shifting security from 'post-incident remediation' to 'pre-deployment planning'; 3) Monitor CDN vendors' AI crawler policy changes and assess impacts on public data acquisition strategies. For compliance/legal teams: 1) Closely track upcoming U.S. government voluntary AI industry standards and prepare compliance paths in advance; 2) Assess potential impacts of OpenAI's government equity model on industry competitive landscape; 3) Review existing cloud service contracts' cross-border data clauses to address geopolitical risks. For investors: 1) Near-term bullish on Palo Alto Networks and CrowdStrike platform integration dividends; 2) Medium-term focus on emerging 'Data Licensing as a Service' (DLaaS) segment; 3) Long-term cautious about geopolitics-driven rising costs in global technology supply chains.

PREDICT

Next 3-6 months: U.S. government will release voluntary AI industry standards, likely requiring safety testing before frontier model releases; Palo Alto Networks and CrowdStrike's next quarterly earnings will continue validating AI security demand sustainability. Next 6-12 months: Cloudflare's AI crawler blocking policy (effective September 15) will trigger new rounds of negotiations and litigation between content platforms and AI companies; more CDN vendors may follow with similar measures. Next 12-24 months: AI security market will rapidly evolve from point solutions to unified platforms, with vendors offering full-lifecycle 'prevention-detection-response-recovery' protection gaining decisive advantages; 'Data Licensing as a Service' (DLaaS) may become a new high-growth niche segment.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)