I. Event Recap: The Landmark AMD-Meta Agreement

On July 9, 2026, AMD announced a landmark high-performance AI chip supply agreement with Meta Platforms. Under the deal, AMD will supply its latest MI-series AI accelerators to power Meta's next-generation AI infrastructure and social media core algorithms. This marks AMD's second mega-level supply agreement in recent months, officially establishing it as NVIDIA's most credible challenger in data center AI chips.

AMD's breakthrough in data center AI is not accidental. The 2024 MI300X was AMD's first AI accelerator truly competitive with NVIDIA's H100, featuring 192GB HBM3 memory and 5.3TB/s memory bandwidth. The 2025 MI350 advanced to 3nm with CDNA 4 architecture, while the upcoming 2026 MI400 is expected to use TSMC N3E process with over 200 billion transistors and peak compute exceeding 2 PFLOPS (FP16).

Meta's motivation for choosing AMD is multifaceted. With 2026 AI CapEx expected at $65 billion, supplier diversification is both a cost optimization and supply chain security imperative. AMD's memory capacity advantages directly appeal to Meta's large language model training and recommendation inference workloads. While financial terms were not disclosed, analysts estimate a multi-billion dollar deal covering 2026-2028 deliveries.

II. Technical Deep Dive: MI vs H100/H200 Architecture Comparison

Process and Transistor Density: NVIDIA H100 uses TSMC 4N (5nm enhanced) with 80B transistors; H200 upgrades memory but retains the same core. AMD MI300X uses TSMC 5nm/6nm hybrid chiplet design with 153B transistors; the upcoming MI400 is expected to use TSMC N3E with over 200B transistors.

Memory Subsystem: This is AMD's key technical differentiator. MI300X offers 192GB HBM3 with 5.3TB/s bandwidth; MI350 is expected to upgrade to 288GB HBM3e. In comparison, H100 offers only 80GB HBM3 (SXM), and H200 upgrades to 141GB HBM3e. For 100B+ parameter models, larger per-card memory means fewer GPUs needed, reducing interconnect complexity.

Compute Performance: H100 peaks at 989 TFLOPS FP16 (sparse 1979 TFLOPS) and 3958 TFLOPS FP8. MI300X peaks at 1.3 PFLOPS FP16. Third-party benchmarks show MI300X delivering 20%-30% better performance-per-dollar in some inference scenarios, though training gaps remain.

Interconnect: NVIDIA's NVLink/NVSwitch remains the most mature high-bandwidth GPU interconnect, supporting up to 256 fully connected GPUs. AMD's Infinity Fabric is technically competitive but lacks large-scale cluster (128+ GPUs) deployment experience.

Software Ecosystem: This remains AMD's biggest challenge. NVIDIA's 18-year CUDA ecosystem has created near-monopolistic developer stickiness. AMD's ROCm has made significant progress supporting PyTorch and TensorFlow but still trails CUDA by 2-3 years in optimization maturity and library richness.

III. Financial Logic: AMD Data Center Growth and Meta CapEx

For AMD, data center is the fastest-growing segment. FY2025 data center revenue was approximately $9.8B, up over 120% YoY. Compared to NVIDIA's $50B+ annual data center revenue, AMD is still early in its追赶. If the Meta deal contributes $2-3B over 2026-2028, AMD's data center CAGR could sustain above 80%.

AI chip gross margins typically range 60%-70%, significantly higher than AMD's traditional CPU business at 40%-50%. Management has hinted at targeting 30%+ data center operating margins by 2027.

For Meta, with 2026 total CapEx around $65B and AI infrastructure exceeding 70% of that, even 10%-15% per-card savings translate to billions of dollars. More importantly, dual-sourcing provides stronger negotiating leverage.

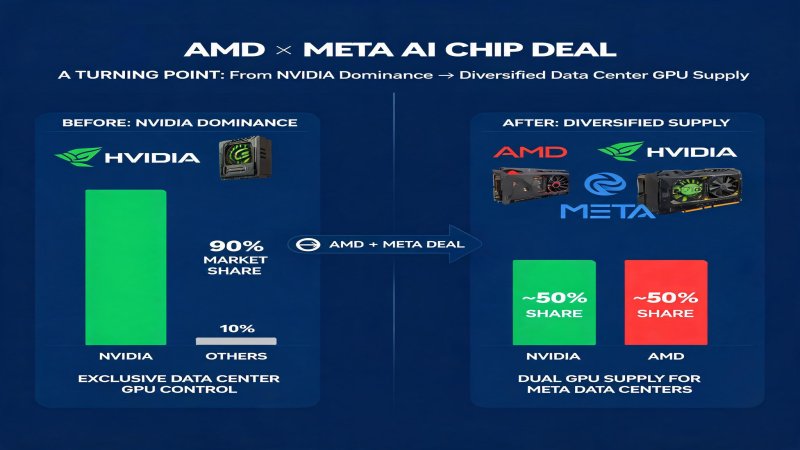

NVIDIA currently holds over 85% data center AI chip market share. AMD's goal is to compress this below 75% by 2027—capturing over $37.5B in a $150B market, roughly 4x its 2025 data center revenue.

IV. Strategic Landscape: AMD vs NVIDIA vs Intel

| Dimension | AMD | NVIDIA | Intel |

|---|---|---|---|

| Flagship AI Chip | MI300X/MI350/MI400 | H100/H200/B100 | Gaudi 2/Gaudi 3 |

| Process | TSMC 5nm/3nm | TSMC 4N/3nm | TSMC 5nm/7nm |

| Memory Capacity | 192GB-288GB | 80GB-141GB | 96GB-128GB |

| Memory Bandwidth | 5.3TB/s+ | 3.35-4.8TB/s | 2.45TB/s |

| Peak FP16 | 1.3 PFLOPS+ | 989 TFLOPS-1.98 PFLOPS | ~800 TFLOPS |

| Software | ROCm (catching up) | CUDA (dominant) | OpenVINO/Habana |

| Key Customers | Meta, Microsoft, Oracle | Google, Microsoft, Amazon | Limited pilots |

| 2025 AI Revenue | ~$10B (est.) | >$50B | <$1B |

| Market Share | ~10-12% | ~85% | ~2-3% |

| Core Strength | Memory, value, openness | Ecosystem monopoly | Unified CPU+accelerator |

V. Challenges: Software Gap and NVIDIA's Counterattack

Software ecosystem remains the critical gap. CUDA's dominance spans programming models, libraries, tools, and talent pools. ROCm supports high-level APIs but trails in kernel optimization and debugging tools.

Capacity constraints are real. AMD relies on TSMC advanced process capacity, which remains supply-constrained in 2026. NVIDIA, as TSMC's top customer, enjoys allocation priority.

NVIDIA's rapid iteration applies continuous pressure. NVIDIA's roadmap advances annually: H100 (2023) → H200 (2024) → B100/B200 (2025) → Rubin (2026). Each generation significantly improves compute, memory, and efficiency.

Customer concentration risk. AMD's AI revenue currently depends heavily on a few large customers. Any reduction would cause significant volatility.

VI. Conclusion and Recommendations

For Data Center Procurement: If planning large-scale AI deployment (1000+ GPUs), consider a dual-vendor AMD+NVIDIA strategy. AMD excels at inference and recommendation systems due to large memory; NVIDIA remains safer for training. For SMBs new to AI, prioritize NVIDIA to minimize adaptation risk.

For Investors: AMD's data center business is breaking through from 0 to 1, validated by the Meta deal. At roughly 1/8 of NVIDIA's market cap, AMD has significant valuation upside for 2026-2028. Monitor ROCm progress, capacity constraints, and potential NVIDIA price wars.

For NVIDIA: The AMD+Meta partnership signals the official arrival of dual-sourcing in data center AI. NVIDIA should accelerate CUDA ecosystem openness while using aggressive bundling (DGX + networking + software) to defend customer stickiness.

Forward Predictions:

- Q3-Q4 2026: AMD will announce 2-3 new tier-1 customers; data center AI revenue QoQ growth sustains above 50%.

- H1 2027: ROCm 7.0 approaches 80% of CUDA usability, significantly lowering adoption barriers for SMBs.

- H2 2027: AMD data center AI market share exceeds 20%; NVIDIA drops below 75% for the first time, marking a true multi-vendor era.

Why it Matters

The data center AI chip market has been dominated by NVIDIA with over 85% share. AMD's Meta deal marks the first large-scale tier-1 hyperscaler adoption of a non-NVIDIA solution. This validates AMD's product competitiveness and signals a shift from monopoly to diversified supply. For Meta, dual-sourcing could save billions; for the industry, intensified competition will accelerate innovation and lower compute costs.

DECISION

Data center buyers: Adopt dual-vendor AMD+NVIDIA strategy; evaluate AMD MI for inference workloads, stick with NVIDIA for training. Investors: AMD is at 0-to-1 inflection; Meta deal is a valuation catalyst—monitor ROCm progress and capacity ramp. NVIDIA watch: Accelerate ecosystem openness and prepare for price competition; B100/Rubin should increase memory to counter AMD.

PREDICT

Q3-Q4 2026: AMD announces 2-3 new tier-1 customers; data center AI revenue QoQ growth sustains above 50%. H1 2027: ROCm 7.0 achieves ~80% CUDA usability, lowering SMB barriers. H2 2027: AMD market share exceeds 20%; NVIDIA drops below 75% for the first time, marking a true multi-vendor era.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)