I. Event Recap: A Revised Agreement That Rewrote AI Industry Rules

On April 27, 2026, OpenAI and Microsoft signed the most significant amendment to their strategic partnership since its inception in 2019. On July 1, 2026, this agreement took formal effect, marking the end of the three-year "deep OpenAI-Azure binding" arrangement.

To understand the weight of this agreement, one must revisit its history. In 2019, Microsoft invested $1 billion in OpenAI, securing exclusive cloud licensing rights to its technology. In January 2023, the partnership expanded: Microsoft obtained an "exclusive" license to OpenAI's intellectual property (with limited edge-case exceptions), and more critically, OpenAI committed to routing the vast majority of its training and inference compute through Azure—creating what the industry called a "capacity commitment" binding structure.

This arrangement was crucial in OpenAI's early development phase—Microsoft provided capital and compute; OpenAI provided technology and brand. However, as demand for GPT-5 and subsequent reasoning models exploded, tensions emerged. By late 2025, OpenAI's Azure usage had grown to the point where capacity shortages began limiting new feature availability, prompting CEO Sam Altman to publicly complain about "compute constraints."

The revised agreement effective July 1, 2026, fundamentally rewrote the partnership rules across four dimensions.

Core Terms Analyzed

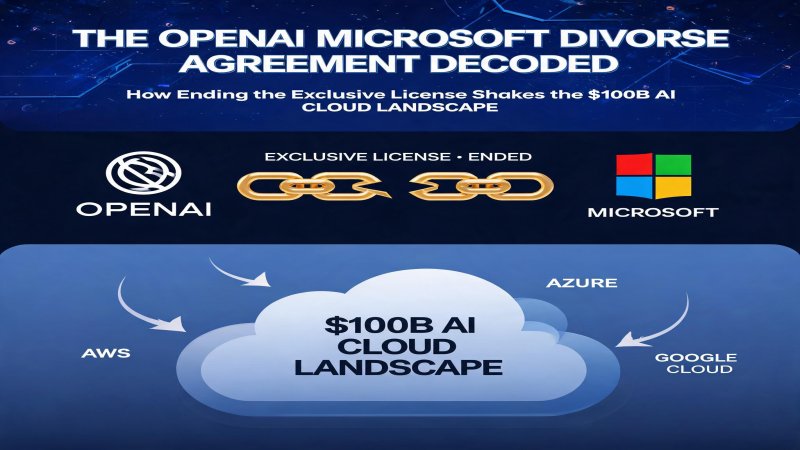

Term 1: Exclusive License Eliminated

The original agreement granted Microsoft an "exclusive" license to OpenAI's IP. Under revision, OpenAI can license its models directly to any enterprise or embed them in third-party services without Microsoft as intermediary. Microsoft retains a non-exclusive license and remains the sole OpenAI model provider for its first-party products like Microsoft 365 Copilot and GitHub Copilot.

Term 2: Capacity Agreement Unbundled

The old "committed spend" model required OpenAI to route at least 95% of training and inference through Azure. Under revision, Microsoft obtains a "Right of First Refusal" (ROFR)—Microsoft gets first look at any new capacity deal, but if it cannot match pricing or delivery timelines from competitors, OpenAI is free to go elsewhere.

Term 3: Competitive Notice Period

OpenAI must provide Microsoft with 90 days' notice before signing capacity contracts with alternative providers. This gives Microsoft time to counter-offer or adjust infrastructure investments.

Term 4: Revenue-Sharing Adjusted

Previously, Microsoft collected 20% on all OpenAI API calls regardless of hosting cloud. Under revision, the 20% share applies only to traffic flowing through Microsoft's own platforms. If OpenAI sells directly on AWS, Google Cloud, or CoreWeave, Microsoft gets zero.

Key Data

- Agreement effective date: July 1, 2026; six-month transition through December 31, 2026

- Microsoft ownership stake: ~27%, valued at ~$135 billion at time of investment

- OpenAI projected mid-2026 inference compute need: nearly 3 exaflops

- Microsoft estimated annual profit gap: $4-6 billion (Goldman Sachs analysis)

- Azure current global datacenter count: 500+

II. Technical Depth: How a 3 Exaflops Gap Crushed the Exclusive License

The surface cause of the agreement revision was commercial negotiation, but the deep driver was a hard technical-economic reality: OpenAI's compute demand growth outpaced Azure's supply capacity.

The Math of the Compute Gap

OpenAI's internal projections showed a need for nearly 3 exaflops of dedicated inference compute by mid-2026 to support GPT-5.1 and its advanced reasoning agent ecosystem. For context, 1 exaflop equals 10^18 floating-point operations per second. As of early 2026, the world's top supercomputer "Frontier" delivered roughly 1.2 exaflops. OpenAI needed inference compute equivalent to 2.5 "Frontiers" dedicated solely to its services.

Even with 500+ datacenters and rapid deployment of NVIDIA GB200 and AMD Instinct MI400 clusters, Azure could not guarantee this capacity within rigid contractual frameworks. Reasons include:

- Physical construction cycles: Large AI datacenter builds take 18-24 months, while OpenAI's model iteration cycles are 6-12 months.

- Supply chain bottlenecks: NVIDIA GB200 delivery lead times exceed 12 months; AMD MI400 capacity is similarly constrained.

- Power constraints: A 3 exaflops inference cluster requires over 1 gigawatt of electrical power—equivalent to a mid-sized city.

Competitors' Pricing Advantage

Another push factor came from competitors' aggressive pricing. Both Oracle's OCI platform and CoreWeave offered OpenAI substantially lower per-GPU-hour pricing than Azure, especially for large-scale dedicated inference instances. Industry sources indicate CoreWeave's quotes were 15-25% below Azure, while Oracle offered discounts up to 30% on certain long-term contracts.

For OpenAI, continuing with Azure as sole supplier meant paying hundreds of millions more in annual compute costs. With AI model training and inference already representing the company's largest operating expense, this cost differential was unacceptable.

Technical Challenges of Multi-Cloud Inference

Shifting from exclusive Azure to multi-cloud architecture presents major technical challenges for OpenAI. First is API consistency: different cloud providers may have varying OpenAI model versions, latency characteristics, and error-handling behaviors. Second is data sovereignty: enterprise customer data residency requirements mean OpenAI must maintain separate model instances across multiple clouds. Third is cost optimization: real-time routing of inference requests across clouds for lowest cost requires sophisticated load balancing and caching strategies.

OpenAI is rumored to be planning a "Global Inference Mesh" that automatically routes requests to the cheapest available cloud provider, with Azure positioned as a "premium tier" offering guaranteed latency SLAs.

III. Financial Logic: Microsoft's $100B Profit Calculus and OpenAI's Platformization Gamble

This revised agreement is not merely a technical cooperation adjustment—it involves the redistribution of billions of dollars in value.

Quantifying Microsoft's Profit Gap

Goldman Sachs analysts estimate that removing the exclusive API revenue share could create a $4-6 billion annual gap in Microsoft's AI services profit. The calculation logic follows:

- Approximately 60-70% of OpenAI API calls previously routed through Azure (Microsoft collected 20% share)

- The remaining 30-40% ran on OpenAI's own API platform, where Microsoft also collected 20% (this disappearing income is the key change)

- Assuming OpenAI 2026 API total revenue of $20-25 billion, Microsoft's share revenue was $4-5 billion

- Post-revision, if OpenAI shifts 30-40% of traffic to non-Azure clouds, Microsoft loses $0.8-1.2 billion in share revenue

- More critically, Azure OpenAI Service's premium pricing power will erode due to competition, further compressing margins

What does a $4-6 billion profit gap mean for Microsoft? Against roughly $80 billion in net income for FY2026, this represents a 5-7.5% profit loss. While Microsoft's diversified business can absorb this shock, Azure AI—as the fastest-growing segment—will face valuation multiple pressure from margin compression.

Microsoft's Response Strategy

Microsoft is not passively taking hits. Several countermeasures are underway:

- Accelerating proprietary model commercialization: The Phi family of small language models and the upcoming MARS reasoning model run entirely on Azure with no partner revenue split. Microsoft plans to integrate MARS into Copilot Runtime, seamlessly switching between OpenAI models and proprietary models based on task cost and latency requirements.

- $15 billion datacenter expansion: Microsoft announced $15 billion in AI-optimized datacenter investments across Iowa, Phoenix, and Calgary, targeting 30% per-teraflop cost reduction before 2027.

- Deepening Copilot ecosystem lock-in: While OpenAI models are no longer Azure-exclusive, the integrated experience of Microsoft 365 Copilot, GitHub Copilot, and Dynamics 365 Copilot remains Azure's unique advantage. Enterprise customers seeking the smoothest agent experience will still find Azure the path of least resistance.

OpenAI's Platformization Valuation Leap

For OpenAI, unbundling is the necessary step to become a "platform company." Previously, OpenAI functioned as an advanced Azure feature module—customers purchased OpenAI services through Azure, with Microsoft controlling customer relationships, billing, and pricing. Now, OpenAI can face enterprises directly and control its own destiny.

The direct benefit of platformization is valuation uplift. As an "Azure feature module," OpenAI's valuation was constrained by Microsoft's pricing strategy and channel control. As a "platform company," OpenAI can be valued on SaaS platform logic—revenue multiples could rise from the current 15-20x to 30-40x. If OpenAI launches an IPO, its valuation could move from the current $135 billion toward the $200-250 billion range.

But platformization also means OpenAI must bear more operational complexity itself: multi-cloud architecture management, enterprise sales team building, and global compliance handling. Costs previously borne by Microsoft must now be digested by OpenAI.

IV. Strategic Depth: From Bilateral Game to Multilateral Competition

The OpenAI-Microsoft unbundling not only changes the relationship between the two companies but reshapes the entire AI cloud competitive landscape.

Microsoft vs AWS vs Google Cloud: The OpenAI Compute Scramble

With the agreement in effect, AWS and Google Cloud immediately gained eligibility to bid for OpenAI workloads. Oracle and CoreWeave issued statements within hours welcoming bidding opportunities.

AWS advantages lie in its globally largest cloud infrastructure scale and mature enterprise sales system. If OpenAI chooses AWS, it gains the broadest global regional coverage and richest supporting services (S3, Lambda, SageMaker).

Google Cloud advantages center on its self-developed TPU chips and deep Vertex AI platform integration. Google may offer competitive TPU v6 pricing to OpenAI in exchange for inference workload share.

Oracle advantages stem from aggressive pricing strategy and customized large-scale workload services. Oracle Chairman Larry Ellison has publicly stated willingness to win OpenAI business at "any price."

CoreWeave, as a GPU cloud specialist, advantages lie in professional NVIDIA GPU optimization and flexible service terms. CoreWeave has offered OpenAI GPU-hour pricing significantly below hyperscale cloud providers.

OpenAI's "Sovereign AI" New Market

Post-unbundling, OpenAI gains access to a previously unreachable market: "Sovereign AI." Under the old agreement, OpenAI's dedicated isolated instances were only available through Azure Government Secret clouds, limiting penetration in highly regulated industries.

Now, OpenAI can deploy dedicated instances on any compliant infrastructure, including:

- Air-gapped environments for defense and government agencies

- Private cloud datacenters for financial institutions

- HIPAA-compliant infrastructure for healthcare organizations

- GDPR-localized deployments for European enterprises

Forrester analyst Cynthia Zheng estimates the "sovereign AI" market could generate hundreds of millions in new contract revenue for OpenAI by 2027, particularly in vendor-lock-in-sensitive government and EU markets.

Competitive Matrix: Four Cloud Vendors' OpenAI Capture Strategies

| Dimension | Microsoft Azure | AWS | Google Cloud | Oracle OCI |

|---|---|---|---|---|

| Current OpenAI Share | ~70% (training + historical inference) | ~0% | ~0% | ~0% |

| Core Advantage | Copilot ecosystem, historical relationship | Global scale, enterprise services | TPU chips, Vertex AI | Aggressive pricing, custom services |

| Bidding Strategy | ROFR + counter-offer | Scale + regional coverage | TPU discounts + AI ecosystem | Price + flexible terms |

| Value to OpenAI | Highest (non-price dimensions) | High | Medium-high | Medium (pure price) |

| Primary Risk | Profit erosion | Margin pressure | TPU capacity limits | Operational inexperience |

V. Challenges and Concerns: Risks and Uncertainties After Unbundling

While unbundling brings more choice to OpenAI and the AI industry, multiple risks and uncertainties warrant vigilance.

Technology Fragmentation and Migration Costs

Multi-cloud architecture brings flexibility but significantly increases technical complexity. Enterprise customers deploying OpenAI models across Azure, AWS, and Google Cloud simultaneously must manage:

- API version differences and feature inconsistencies across clouds

- Cross-cloud identity authentication and access control (Entra ID vs IAM vs Cloud Identity)

- Fragmented data residency and compliance policy management

- Multi-point failure risks and more complex monitoring systems

A top-voted developer comment on Reddit expressed widespread concern: "We've built our entire RAG pipeline around Azure's managed identity and private endpoint model. If OpenAI starts pushing its own multi-cloud auth API, our migration costs will be catastrophic."

The Antitrust Sword of Damocles

The U.S. FTC opened an inquiry in late 2025 into the OpenAI-Microsoft partnership structure, questioning whether exclusive licensing and fixed capacity arrangements constituted an unregistered merger. While unbundling is a preemptive step, the FTC's final ruling could still impose binding requirements on both parties.

The EU regulatory environment is equally challenging. The Digital Markets Act (DMA) constraints on large platforms are tightening, and the European Commission may question "priority partnerships" between OpenAI and any single cloud provider.

Potential Deterioration of Equity Relations

Microsoft currently holds approximately 27% of OpenAI, valued at roughly $135 billion. If OpenAI's platformization strategy succeeds and its standalone valuation rises significantly, Microsoft's equity value will grow accordingly. But conversely, if OpenAI competes directly with Microsoft for the same enterprise customers in multi-cloud competition, the equity relationship could shift from strategic synergy to financial drag.

Long-term, complete separation is not impossible. Microsoft may reduce its OpenAI stake through secondary markets in exchange for cash returns and priority renewal commitments on Azure. OpenAI may seek more diversified shareholders, including sovereign wealth funds and strategic investors.

Service Quality and SLA Risks

In the exclusive Azure era, OpenAI's service quality was backed by Microsoft's enterprise-grade infrastructure. Post multi-cloud transition, reliability, latency, and scalability may vary across cloud providers. If OpenAI's "Global Inference Mesh" routes requests during peak periods to capacity-constrained secondary clouds, user experience could suffer.

VI. Conclusion: Investment Perspective and Forward-Looking Judgments

The OpenAI-Microsoft unbundling is a structural inflection point as the AI industry shifts from "closed alliances" to "open competition." Over the next 24 months, this event's impact will permeate every layer of financial statements, competitive dynamics, and technical architecture.

Assessment for Microsoft

Short-term (6-12 months): Microsoft Azure AI revenue growth may remain strong (because historical customer migration takes time), but margins will face pressure. Investors should focus on Azure AI services gross margin changes; if margins decline more than 200 basis points for two consecutive quarters, Microsoft's AI business valuation multiples may need downward revision.

Medium-term (12-24 months): Commercialization progress of Microsoft's proprietary MARS model will be the key variable. If MARS can compete with OpenAI models on inference cost and performance, Microsoft can reduce OpenAI dependency and rebuild profit moats. Copilot ecosystem integration remains Microsoft's most solid defensive barrier.

Long-term (24+ months): The Microsoft-OpenAI relationship may further loosen. Microsoft may reduce its OpenAI stake below 15% in exchange for long-term priority cooperation commitments on Azure. The two will shift from "strategic alliance" to "important partner."

Assessment for OpenAI

Short-term: Platformization transformation will bring rising operational costs (multi-cloud architecture management, enterprise sales team building). OpenAI must balance revenue growth against cost control.

Medium-term: If the "sovereign AI" market and multi-cloud compute services progress smoothly, OpenAI's valuation could leap from $135 billion to above $200 billion. An IPO becomes the most likely capital event.

Long-term: OpenAI must prove it can acquire and retain enterprise customers without Microsoft's channel support. If multi-cloud competition triggers price wars, OpenAI's margins could face compression.

Judgment for the Overall AI Cloud Market

By 2027, top-tier AI model deployment architectures will universally adopt "multi-cloud + self-hosted" hybrid models. Single-cloud lock-in will become history, and cloud provider competition will shift from "exclusive partnership relationships" to "pure technology and price competition." This is favorable for enterprise customers but pressures cloud provider margins. Ultimate winners will be those capable of delivering differentiated value (lower latency, better security, deeper enterprise integration) within open ecosystems.

Why it Matters

This revised agreement is a landmark event as the AI industry shifts from 'single-cloud lock-in' to 'multi-cloud freedom.' For Microsoft, losing exclusivity means a $4-6 billion annual profit gap and direct erosion of Azure's AI inference market share by AWS, Google Cloud, and Oracle. For OpenAI, it is the critical step from being 'a Microsoft feature module' to becoming a 'platform company,' but also means managing multi-cloud complexity and costs independently. For enterprise customers, intensified competition brings lower prices and more choices, but increases cross-cloud governance complexity. For investors, Microsoft Azure AI growth figures need re-disaggregation, while OpenAI's standalone valuation may rise significantly due to platformization.

DECISION

[CIO/CTO] 1. Immediately launch multi-cloud deployment evaluations for OpenAI models, adding AWS Bedrock, Google Vertex AI, and Oracle OCI to candidate lists to avoid Azure dependency. 2. Renegotiate existing Azure OpenAI Service contracts, leveraging competitive dynamics for better unit pricing and flexible capacity commitments. 3. Establish cross-cloud AI governance frameworks to uniformly manage OpenAI model versions, API consistency, and security compliance across clouds. [Investors] 4. Closely monitor Microsoft Q3-Q4 2026 earnings for Azure AI services gross margin changes; if AI service margins decline more than 200 basis points, reassess Microsoft's AI business valuation model. 5. Watch for OpenAI IPO valuation premium if launched; platform positioning could move valuation from current $135B toward $200-250B range.

PREDICT

- By Q4 2026, at least 30% of OpenAI inference workloads will run on non-Azure clouds, with Oracle and CoreWeave as first major beneficiaries. 2. Microsoft will release its proprietary MARS reasoning model before Build 2027 (May 2027) as a core initiative to reduce OpenAI dependency. 3. By mid-2027, OpenAI and Microsoft may fully unwind deep equity ties, with Microsoft reducing its stake below 15% through secondary markets in exchange for OpenAI's priority renewal commitment on Azure. 4. Due to intensified multi-cloud competition, OpenAI API average unit prices will decline 15-20% in 2027 versus 2026, but total market size will expand more than 3x due to surging usage.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)