OpenAI Ends Microsoft Exclusive Partnership: AI Infrastructure Market Shifts from 'Exclusive Moat' to 'Open Competition'

Seven-Year Exclusive Partnership Ends: Core Terms of Agreement Revision

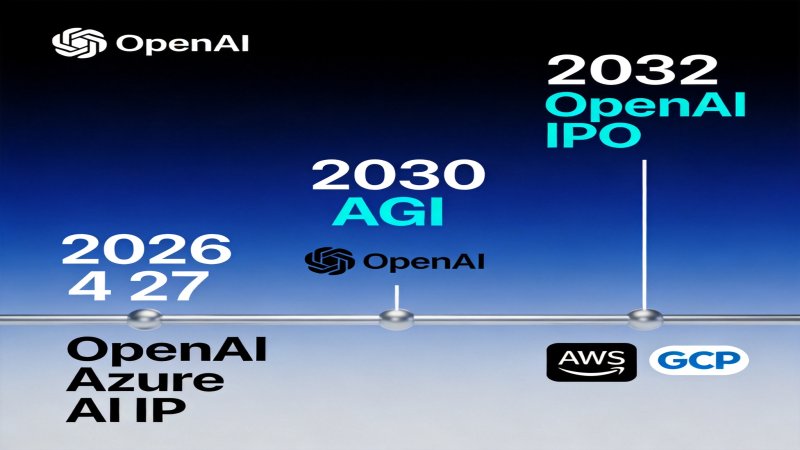

On April 27, 2026, Microsoft and OpenAI simultaneously announced on their official websites a major adjustment to their seven-year strategic partnership framework. This is not an ordinary contract revision—it represents a strategic turning point that could reshape the global AI industry's power dynamics.

The core terms of this agreement revision clearly point to three keywords: unbundling, balancing, opening.

End of Cloud Service Exclusivity: Microsoft remains OpenAI's "Primary Cloud Partner," with OpenAI products still launching first on Azure, but a critical new clause has been added—"unless Microsoft cannot or chooses not to support the necessary capabilities." This means OpenAI can now offer all products to customers of any cloud service provider, completely breaking Microsoft's monopoly on OpenAI model distribution.

IP License Shifts from Exclusive to Non-Exclusive: Microsoft's IP license to OpenAI models and products extends to 2032, but its nature changes from "exclusive" to "non-exclusive." This change clears legal obstacles for OpenAI's collaboration with competitors like AWS and Google Cloud.

Revenue Sharing Structure Adjustment: Microsoft will no longer pay revenue share to OpenAI (the previous bilateral revenue-sharing mechanism has been terminated). OpenAI's revenue share to Microsoft continues through 2030, with the ratio unchanged but subject to an undisclosed total cap. Notably, the original agreement's trigger clause stating "revenue sharing stops once OpenAI achieves AGI" has been officially cancelled.

Microsoft remains involved in OpenAI's growth with approximately 27% equity (valued at approximately $135 billion), playing a key role in OpenAI's for-profit restructuring in 2025. This revised agreement represents a recalibration of interests in the new AI competition landscape.

OpenAI's True Motivation for Independence: Strategic Unbundling Before IPO

Why did OpenAI choose to unbundle at this moment? The answer lies at the intersection of three主线: compute bottleneck, revenue pressure, IPO countdown.

Compute Anxiety and Multi-Cloud Needs: As AI competition shifts from the "large model arms race" to the "Agentic AI" era, OpenAI's compute demands have grown exponentially. Relying solely on Microsoft Azure can no longer support its GW-level compute expansion plans. OpenAI's Head of Revenue Denise Dresser candidly stated in an internal memo: "The exclusive relationship with Microsoft has limited our ability to meet enterprise needs."

Revenue Growth Stalls: According to internal sources, affected by Google Gemini's rapid market share gains, OpenAI failed to achieve its 2025 annual revenue target. Entering 2026, due to Anthropic's aggressive market penetration in coding tools and enterprise markets, OpenAI has failed to meet monthly revenue targets for consecutive months. More troubling for management is the persistently high churn rate among ChatGPT paid subscribers.

Independence Requirements Before IPO: Market sources reveal OpenAI's latest valuation reaches $852 billion, planning to submit IPO applications in Q4 2026, targeting a valuation to challenge $1 trillion. The exclusive partnership model creates excessive business dependence on Microsoft, failing to meet public company independence requirements. The revised agreement grants multi-cloud deployment and multi-channel licensing capabilities, creating more transparent financial structures and shifting growth logic from "Microsoft subsidiary" to "global AI platform."

Simultaneously, OpenAI has reached a strategic partnership with Amazon: committing up to $50 billion in investment, expanding the original $38 billion AWS agreement by $100 billion over the next eight years; AWS will also serve as the exclusive third-party cloud distributor for OpenAI's enterprise platform Frontier. The existence of this deal means OpenAI had long been positioning for the "post-Microsoft exclusive era."

Microsoft's Ledger of Gains and Losses: Cost Reduction and Risk Hedging

On the surface, Microsoft appears to have "lost" by giving up exclusive distribution rights. But a careful breakdown reveals this is an astute transaction for Microsoft.

Gain: Terminating Reverse Revenue Share Directly Improves Azure Gross Margins. Under the old mechanism, when users paid through Azure to access OpenAI models, Microsoft had to pay OpenAI a share. Under the new mechanism, this capital flow is cut off, and Azure's gross margins on OpenAI service sales will improve directly.

Gain: AGI Trigger Cancellation Makes Revenue Share More Stable. The original agreement stipulated that revenue sharing would stop once OpenAI was determined to have achieved AGI. The new agreement cancels this uncertainty, exchanging it for stable revenue sharing through 2030 (though with a total cap).

Gain: IP License Extended to 2032. Microsoft's access rights to OpenAI IP extended by two years, ensuring continuity of AI capabilities in Copilot and other products.

Loss: Losing Exclusive Distribution Control. This means Azure's differentiated advantage in OpenAI product distribution has weakened.

Microsoft CEO Satya Nadella stated in the announcement: "The revised agreement increases predictability, strengthens our joint ability to build and operate AI platforms at scale, while providing both companies greater flexibility to pursue independent opportunities." The subtext: Microsoft is transitioning from the "AI distributor" role to the "AI platform player" role—building more fundamental capabilities through initiatives like Stargate (AI infrastructure investment) and custom silicon (Maia 100) rather than relying on exclusive distribution of OpenAI models.

In fact, Microsoft has been advancing a "multi-model strategy." Beyond Azure OpenAI Service, Microsoft simultaneously introduces models from Meta Llama and Google Gemini, reducing dependence on any single vendor. This mirrors OpenAI's pursuit of multi-cloud collaboration—both parties are doing the same thing: reducing single-dependency risk.

AWS/GCP Strategic Opportunities: Who Can Capture OpenAI's Dividends

The end of the exclusive agreement opens a substantial opportunity window for AWS and Google Cloud.

AWS: Racing to Get OpenAI Access. Amazon CEO Andy Jassy quickly responded on X: "AWS will provide OpenAI models to customers through Bedrock in the coming weeks." This is not empty talk—OpenAI reached a strategic partnership with Amazon as early as February 2026, with AWS already positioning as the exclusive third-party cloud distributor for the Frontier platform.

More importantly, AWS launched OpenAI-compatible API endpoints in December 2025 (including Responses API and Chat Completions API), supporting models like GPT-OSS. This means developers can migrate existing OpenAI applications to AWS by simply changing the base URL, with extremely low migration costs.

Google Cloud: TPU Ban Lifted. Industry analysis suggests the biggest winner from this agreement revision might be Google—"Almost all frontier AI labs are using TPUs; the only one not using them was OpenAI, mainly due to the previous exclusive partnership agreement. With Google's eighth-generation TPU launch, OpenAI will likely begin considering adopting TPUs."

Google Cloud CEO Thomas Kurian has repeatedly expressed "open attitudes" toward OpenAI, noting Google Vertex AI's advantages in enterprise market security and compliance. With the exclusive shackles removed, Google Cloud will compete for OpenAI as the crown jewel of AI on a more equal footing.

From a market share perspective, AWS currently holds approximately 32% of the global cloud market, Azure approximately 24%, and Google Cloud approximately 12%. Full availability of OpenAI models will provide AWS and Google Cloud with differentiated competitive power, directly impacting Azure's "OpenAI-first" advantage.

AI Cloud Market Landscape Restructuring: From Oligopoly to Multi-Player Competition

The deeper significance of this agreement revision extends far beyond adjustments to two companies' interests. It signals a paradigm shift in the AI industry chain from the "exclusive moat" model to the "open competition" model.

Implications for AI Model Vendors: Multi-cloud deployment has become an irreversible trend. While exclusive partnerships can secure compute support and financial backing, they also limit growth ceilings and IPO independence. Future AI model vendors will more strongly favor "multi-cloud-first" distribution strategies.

Implications for Cloud Service Providers: "OpenAI exclusivity" was once Azure's core differentiated competitive advantage. As this advantage disappears, cloud service providers need to find new differentiation paths: self-developed AI chips (like Azure Maia, AWS Trainium), vertical industry AI solutions, and hybrid cloud and edge AI capabilities will become competitive focal points.

Implications for Enterprise Customers: The end of exclusive agreements means enterprises will have more choices. But more choices also mean increased management complexity—how to unify management, optimize costs, and ensure governance in a multi-cloud environment will become a new topic in enterprise AI procurement. This is also the fundamental reason the AI Gateway segment (like Portkey) is experiencing explosive growth.

Compute diversification is becoming a shared choice among leading AI companies. Meta recently committed $48 billion in supplementary compute to CoreWeave and Nebius; OpenAI's multi-cloud deployment is merely the latest footnote in this trend. In this sense, the agreement revision represents a form of "unbundling" for both parties—Microsoft loosens the "reins" of exclusive distribution, while OpenAI breaks free from the "shackles" of the single cloud platform.

But "unbundling" does not mean "breaking up." Microsoft remains OpenAI's largest shareholder, most important cloud partner, and beneficiary of the $250 billion Azure procurement commitment. This is a relationship upgrade from "exclusive binding" to "flexible alliance."

Why it Matters

On April 29, 2026, OpenAI announced the end of its seven-year exclusive partnership with Microsoft, a historic turning point in the AI infrastructure market. OpenAI's shift from 'exclusive moat' to 'open competition' is driven by computing bottlenecks, revenue pressure, and IPO preparation.

DECISION

Decision Recommendations

For Vendor(AI Model Vendors & Cloud Service Providers)

- Microsoft: Accelerate "multi-model strategy" implementation, reduce dependence on OpenAI; leverage Stargate project and custom silicon to build more fundamental AI infrastructure competitiveness

- AWS/Google Cloud: Immediately initiate OpenAI product integration, capture market share lost by Azure; strengthen enterprise security and compliance differentiation

- Anthropic/Google: Capitalize on OpenAI's internal turmoil window, intensify enterprise market and coding tools offensive

For Enterprise(Enterprise Buyers)

- High Priority: Evaluate multi-cloud AI deployment strategy, avoid binding all AI capabilities to a single cloud vendor

- Pay attention to AI Gateway tools (like Portkey) to simplify unified management, cost optimization, and security governance across multi-cloud environments

- Renegotiate AI service contracts with cloud providers, leverage intensified market competition to secure more favorable terms

For Investor(Investors)

- Microsoft: Near-term pressure but long-term thesis unchanged, maintain Overweight; monitor Azure gross margin changes as key indicator

- AWS (Amazon): OpenAI integration is an important supplement to AWS AI capabilities, expected to boost AWS market share outlook

- AI Gateway sector (Portkey, etc.): Multi-cloud trend directly benefits AI Gateway sector, focus on related targets

PREDICT

6 months(High confidence)

AWS officially provides OpenAI models through Bedrock, Azure OpenAI Service market share begins declining. Google Cloud accelerates OpenAI cooperation negotiations. OpenAI IPO preparations enter substantive stage.

1 year(High confidence)

OpenAI completes multi-cloud deployment strategy, AWS/GCP contribute significant revenue growth. Microsoft's multi-model strategy shows results, Azure gross margins stabilize and recover.

2 years(Medium confidence)

AI cloud market landscape initially reshapes: Azure market share may decline 3-5 percentage points, AWS and Google Cloud each gain 1.5-2.5 percentage points. OpenAI IPO completes, valuation challenging $1 trillion.

3 years+(Medium confidence)

"Exclusive partnership" model completely fades in AI industry, multi-cloud becomes mainstream. Cloud service provider competition focus shifts to AI infrastructure (chips, data centers) and vertical industry solutions.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)