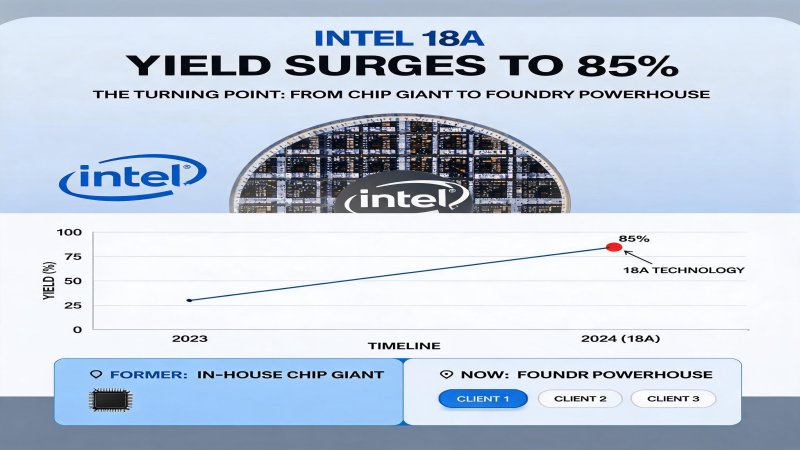

<h2>I. Event Recap: Intel 18A Yield Surges from 65% to 85%, Foundry Business at a Historic Inflection Point</h2>

<p>On July 15, 2026, an industry report jointly released by KeyBanc and FactSet sent shockwaves through the semiconductor community: Intel's 18A (1.8nm-class) process yield had surged from 65% in the previous quarter to 85%. This figure not only signifies a milestone breakthrough in Intel's advanced process technology but also marks the formal emergence of the former chip king as a credible third pillar in the foundry market alongside TSMC and Samsung.</p>

<p>The timeline stretches back to 2024. At that time, Intel's 18A process was still in early development with yields hovering around 50%, and the market widely doubted whether mass production could be achieved by 2025. By Q4 2025, 18A yield had climbed to 65%, beginning to attract tentative orders from smaller customers. By Q2 2026, yield had jumped to 85%—just 5 percentage points behind TSMC's N2 (2nm) process at 90%, and far ahead of Samsung's SF2 process at 50-60%.</p>

<p>Alongside the yield breakthrough came a series of heavyweight customer signings: NVIDIA, AMD, Marvell, Microsoft, Micron, and OpenAI have all reached cooperation intentions with Intel Foundry. According to the KeyBanc report, due to severe TSMC capacity shortages, Intel's process technology has become an ideal choice for numerous external customers. KeyBanc promptly raised Intel's price target from $110 to $155, an increase of 41%.</p>

<p>On the financial front, Intel's full-year 2025 revenue was approximately $52 billion, with foundry business (Intel Foundry) revenue of about $12 billion, accounting for 23% of total revenue. With 18A mass production and customer orders pouring in, analysts expect Intel Foundry revenue to grow 40%-50% in 2026, reaching $17-18 billion. Notably, Intel's advanced packaging EMIB-T chip yield has reached 98%, nearly on par with TSMC's CoWoS technology at 98%-99%, up from just 90% three months ago.</p>

<h2>II. Technical Deep Dive: The Dual Engine of 18A Process and EMIB Packaging</h2>

<p>Intel 18A process, short for Intel 18 Angstrom (~1.8nm), is the ultimate node in Intel's "five nodes in four years" strategy announced in 2021. The process employs multiple revolutionary technologies: RibbonFET gate-all-around (GAA) transistors, PowerVia backside power delivery, and High-NA EUV lithography.</p>

<p>RibbonFET is Intel's commercial name for GAA transistors. Compared to traditional FinFET structures, RibbonFET achieves better electrostatic control and lower leakage by completely surrounding the channel region with the gate. According to Intel's published data, RibbonFET delivers approximately 15% performance improvement at the same power, or about 25% power reduction at the same performance. PowerVia moves the power delivery network from the frontside to the backside of the chip, freeing frontside routing resources for signal transmission and further increasing chip density by approximately 5-10%.</p>

<p>High-NA EUV is the key enabling technology for the 18A process. ASML's latest financial report shows that its High-NA EUV equipment has reached a new mass-production readiness milestone, with the first high-volume Logic product already validated through Intel's 18A process. This makes Intel the world's first chipmaker to integrate High-NA EUV into a production-grade advanced process, ahead of TSMC's N2.</p>

<p>In packaging technology, Intel's EMIB (Embedded Multi-die Interconnect Bridge) has also made significant progress. The report indicates EMIB-T chip yield has reached 98%, currently used in products including NVIDIA Feynman GPU, Google TPU HumuFish, and Amazon AWS Trainium 3. EMIB's advantage lies in eliminating the need for silicon interposers, enabling high-bandwidth chip-to-chip interconnect at lower cost—highly attractive for multi-chip packaging solutions such as AI accelerators.</p>

| Dimension | Intel 18A | TSMC N2 | Samsung SF2 |

|---|---|---|---|

| Process Node | 18A (~1.8nm) | N2 (2nm) | SF2 (2nm) |

| Transistor Structure | RibbonFET (GAA) | GAA | GAA |

| Backside Power | PowerVia (Production) | Planned H2 2026 | Planned |

| Current Yield | 85% | 90% | 50-60% |

| High-NA EUV | Production Validated | Not in N2 Initial | Not Adopted |

| Packaging Tech | EMIB-T (98% yield) | CoWoS (98-99%) | I-Cube |

| Key Customers | NVIDIA, OpenAI, Microsoft | Apple, NVIDIA, AMD | Internal Mostly |

| Risk Production | Q1 2026 | Q4 2025 | Q4 2025 |

| Mass Production | Q2 2026 | H1 2026 | H2 2026 |

<h2>III. Financial Logic: Can the Foundry Business Sustain Intel's Second Growth Curve?</h2>

<p>Intel's financial struggles have persisted for years. In 2024, company revenue was approximately $54 billion, down about 5% year-over-year; net profit was only about $3 billion, with margins severely compressed. Core issues include eroding PC and server CPU market share to AMD, persistent losses in the foundry business, and massive advanced process R&D investments with delayed returns.</p>

<p>However, the 18A yield breakthrough could change everything. Intel Foundry achieved approximately $12 billion in revenue in 2025 but remained in the red, primarily due to capacity ramp costs and R&D amortization. With 18A mass production and increasing customer orders, Foundry gross margins are expected to turn positive in the second half of 2026. KeyBanc predicts Intel's AI server-related revenue will grow 25-30% in 2026 and another 50% the following year.</p>

<p>From a valuation perspective, Intel's current market cap is approximately $80 billion, with a price-to-book ratio of only about 0.8x—a historical low. KeyBanc's $155 target price implies roughly 70% upside. Three core logics underpin this valuation recovery: first, Foundry business turning profitable; second, market share gains from the 18A process; third, EMIB packaging technology becoming a significant alternative for AI chip packaging.</p>

<p>The risk lies in capital expenditure. Intel's 2026 CapEx plan is approximately $17 billion, with about €5 billion (~$5.4 billion) allocated to expanding the Leixlip fab in Ireland. This massive investment will continue to pressure free cash flow. If customer adoption proceeds slower than expected, financial stress will intensify further.</p>

<h2>IV. Strategic Depth: How Intel Can Shake TSMC's Foundry Hegemony</h2>

<p>TSMC currently commands approximately 90% of the global advanced process foundry market. While its N2 process yield (90%) still slightly exceeds Intel 18A (85%), TSMC faces two structural challenges: capacity bottlenecks and geopolitical risk.</p>

<p>On capacity, TSMC's CoWoS advanced packaging capacity has been fully allocated to major customers such as NVIDIA, AMD, and Apple, with new customer orders backlogged for 12-18 months. Intel's EMIB technology offers an alternative high-bandwidth packaging option with relatively abundant capacity. Furthermore, Intel owns substantial fabs in the US (Arizona, Oregon, New Mexico) and Europe (Ireland, Germany), providing customers seeking supply chain diversification with a "non-Taiwan" option.</p>

<p>Geopolitics is another critical variable. The US CHIPS Act provided Intel with approximately $8.5 billion in direct subsidies and $11 billion in loan guarantees, significantly reducing its US fab construction costs. For American AI giants such as NVIDIA and OpenAI, shifting some chip production to Intel is both a strategy to diversify geopolitical risk and aligns with the US government's policy of reshoring semiconductor manufacturing.</p>

<p>Nevertheless, Intel's strategic depth is not without challenges. TSMC still holds clear advantages in customer trust, ecosystem maturity, and manufacturing execution. Intel must prove that its 18A process not only meets yield targets but truly matches or surpasses TSMC N2 in power, performance, and area (PPA). Additionally, Intel has historically suffered from process delays, and rebuilding customer trust in its delivery capabilities will take time.</p>

<h2>V. Challenges and Concerns: Uncertainties Beyond Yield</h2>

<p>Despite the encouraging 18A yield breakthrough, Intel faces formidable challenges. First is technical risk: while 85% yield approaches TSMC N2's 90%, whether Intel 18A is truly competitive in transistor density, power consumption control, and chip area efficiency (PPA) remains to be validated by major customers such as NVIDIA and OpenAI in actual products.</p>

<p>Second is financial risk. Intel's 2026 CapEx of $17 billion against expected full-year revenue of $55-60 billion implies a capital intensity (CapEx/Revenue) of nearly 30%, significantly higher than TSMC's ~25% and Samsung's ~20%. If Foundry customer adoption proceeds slower than expected, Intel's cash flow and debt levels will face tremendous pressure.</p>

<p>Third is competitive risk. TSMC's N2 process is already at 90% yield and in mass production, with N2P (2nm enhanced) and A14 (1.4nm) on the roadmap. While Samsung's SF2 yield remains low, its advantages in memory chips (HBM) and advanced packaging cannot be ignored. If Intel cannot rapidly establish economies of scale at the 18A node, it risks being left behind by TSMC's subsequent nodes.</p>

<p>Finally, customer concentration risk: the publicly confirmed partners (NVIDIA, OpenAI, Microsoft) are all American tech giants. If geopolitical tensions ease and TSMC capacity constraints are alleviated, whether these customers will return to TSMC after 18A mass production is a realistic strategic consideration.</p>

<h2>VI. Conclusion: Intel's Foundry Revival and Investment/Procurement Recommendations</h2>

<p>Intel's 18A yield surge from 65% to 85% represents the company's most important technical milestone in a decade. It not only means Intel has regained the ability to compete head-to-head with TSMC in the advanced process race but also marks the critical inflection point where its foundry business transitions from "strategic losses" to "scalable profitability."</p>

<p><strong>For investors:</strong> Intel's current valuation is at a historical low with a price-to-book ratio below 1x, offering an attractive risk-reward profile. KeyBanc's $155 target reflects market optimism for Foundry profitability. However, investors should closely monitor Q3 and Q4 Foundry customer onboarding progress, actual 18A PPA performance, and free cash flow improvement. A "buy-on-dips, accumulate in batches" strategy is recommended, with a 12-18 month target holding period.</p>

<p><strong>For chip procurement decision-makers:</strong> For AI/datacenter chip designers seeking a second source to reduce supply chain risk, Intel 18A and EMIB packaging provide a high-quality alternative to TSMC. Technical engagement and pilot production validation with Intel Foundry should be initiated in H2 2026, with particular attention to power consumption and packaging yield metrics. For consumer electronics and automotive chip customers, Intel's mature processes (Intel 4/3) are also worth evaluating.</p>

<p><strong>For industry observers:</strong> The global foundry market is evolving from "TSMC dominance" toward a "dual-leadership + Samsung chasing" tri-polar structure. Intel's return will intensify advanced process competition, potentially lowering global AI chip manufacturing costs and driving semiconductor supply chain diversification. But the final outcome of this race will be determined in 2027, when Intel 18A-P goes head-to-head with TSMC N2P.</p>

Why it Matters

Intel's 18A yield breakthrough directly threatens TSMC's monopoly in advanced foundry services. Global AI chip manufacturing currently relies heavily on TSMC, where capacity shortages have become a critical bottleneck for giants like NVIDIA and OpenAI. Intel's return offers a high-quality non-Taiwan alternative, supported by US CHIPS Act subsidies, potentially driving semiconductor supply chain diversification. For investors, Intel's current P/B ratio below 1x offers substantial valuation recovery potential if Foundry turns profitable.

DECISION

<ul><li><strong>Investors:</strong> Consider accumulating Intel stock on dips with a 12-18 month holding period; closely monitor Q3/Q4 Foundry customer onboarding and actual 18A PPA performance.</li><li><strong>Chip Designers:</strong> Initiate technical engagement with Intel Foundry in H2 2026, evaluating Intel 18A and EMIB packaging as a second source to TSMC.</li><li><strong>Enterprise Procurement:</strong> For AI server and datacenter CPU purchases, request suppliers to evaluate the feasibility and delivery timeline of Intel-foundry versions.</li></ul>

PREDICT

<ul><li><strong>Q3-Q4 2026:</strong> Intel 18A will see first mass-production chips for NVIDIA, OpenAI and others; actual PPA data will determine market confidence.</li><li><strong>H1 2027:</strong> Intel Foundry is expected to achieve quarterly gross margin profitability, with annual revenue reaching $17-18 billion.</li><li><strong>H2 2027:</strong> The head-to-head showdown between Intel 18A-P and TSMC N2P will determine medium-to-long-term technical leadership.</li><li><strong>2028:</strong> If Intel 14A proceeds on schedule, the global advanced foundry market could stabilize into a TSMC-Intel duopoly, with Samsung focusing on memory+HBM differentiation.</li></ul>

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)