AI-Driven Cybersecurity Transformation and Valuation Reconstruction

I. Event Recap: Four Giants Signal AI Security Divergence on the Same Day

June 30, 2026, marked a notable inflection point for the cybersecurity sector. Palo Alto Networks (PANW), Zscaler, Cloudflare, and Fortinet — with a combined market cap exceeding $300 billion — released critical signals about the AI security market almost simultaneously, yet their trajectories diverged sharply.

Palo Alto Networks announced strategic partnerships with IBM, Red Hat, and Deutsche Telekom to expand its AI security platform. The IBM/Red Hat collaboration focuses on joint solutions to shorten vulnerability-to-remediation cycles across open-source software, commercial applications, OT systems, and healthcare infrastructure. The more strategically significant partnership with Deutsche Telekom delivers an AI-driven "Sovereign Cortex" security operations platform targeting stringent European data residency requirements under GDPR, NIS2, and DORA, scheduled for launch in Q3 FY2026. PANW's stock has gained 65.1% year-to-date, far outpacing the Zacks security sector average of 49.8%.

In stark contrast, Zscaler experienced its largest single-day drop in company history — plummeting over 30%. The apparent trigger was the departure of two sales leaders and management's cautious FY2027 ARR growth guidance of 16%-17%. However, the deeper issue is that the market had priced Zscaler on an assumption of perpetual 30%+ growth. Any deceleration signal triggers severe valuation compression. Notably, Zscaler's fundamentals remain intact: Q2 revenue grew 26% YoY, ARR reached $3.53 billion growing at 25.1%, AI Protect surpassed $100 million in trailing-twelve-month revenue, and deferred revenue grew 32%.

Cloudflare surged 4.29%, driven by NowSecure's 2026 Mobile Application Risk Management Survey revealing that 95% of enterprises have deployed AI features in mobile apps, yet 37% lack AI behavior monitoring and 68% heavily rely on third-party code with minimal security review. This disconnect between AI deployment and security governance directly fuels demand for robust security infrastructure.

Fortinet occupies the middle ground. It launched FortiSOC, a unified cloud-delivered security operations platform consolidating six SOC functions into a single SaaS experience with built-in AI agents for automated alert triage and response. Q1 revenue reached $1.85 billion (20% YoY growth), with free cash flow hitting a record $1.01 billion.

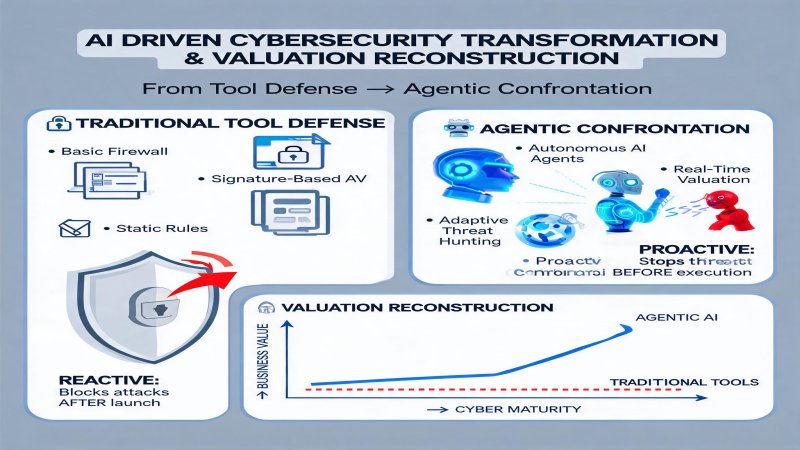

II. Technical Depth: Three Architectural Paradigms for AI Security

The four vendors represent three fundamentally different AI security architectures, signaling the industry's shift from signature-based detection to behavioral understanding.

Palo Alto Networks: Platform-Centric AI Architecture. Cortex XSIAM 3.0 employs "In-Flight Inference" — analyzing data streams in real-time without backhauling raw data to the cloud. Its Prisma AIRS system deploys 300+ specialized models covering the full attack chain, from supply chain poisoning to AI-generated phishing. The IBM partnership embeds security into Red Hat OpenShift DevOps pipelines, enabling "security left-shift."

Zscaler: Zero Trust + AI Agent Architecture. AI Protect leverages Zscaler's global security cloud processing 750 billion daily transactions, using federated learning to continuously improve detection while preserving customer privacy. Its core advantage is deep coupling of AI inference with zero-trust access control — every user access, API call, and AI agent operation receives real-time risk scoring.

Cloudflare: Network-Native AI Security. Cloudflare's edge network spanning 270+ cities enables millisecond-level response. Its 2026 AI Blockade feature covers 3.8 million domains through three-layer permission controls (robots.txt / search / ai-train / ai-input) to prevent unauthorized AI crawler access.

Fortinet: ASIC-Accelerated AI Security Operations. FortiGate G-series 3500G/400G runs on proprietary NP7 and SP5 processors optimized for AI inference throughput. FortiSOC's AI agents automate the complete response cycle from alert aggregation to root-cause analysis to automatic blocking, compressing mean-time-to-response (MTTR) from hours to minutes.

III. Financial Logic: AI Security Revenue as the Core Valuation Variable

June 30 market movements revealed that AI security capabilities are transforming from cost centers to valuation drivers.

Palo Alto Networks' financials are most compelling. Q2 FY2026 revenue reached $2.6 billion (15% YoY growth), with Next-Generation Security ARR at $5.6 billion growing 32%. The 65.1% YTD stock gain and 18.35x forward P/S ratio (vs. sector average 16.34x) reflect market willingness to pay a premium for platformization. Cortex XSIAM is evolving from a security tool to a "security operating system."

Zscaler's 30% crash illustrates the other side of the valuation equation. Despite Q2 revenue of $850.5 million (25.4% YoY growth), ARR of $3.53 billion (25.1% growth), and AI Protect surpassing $100 million TTM, the market's negative reaction to 16-17% ARR growth guidance signals a shift from "pure growth valuation" to "growth quality valuation." When growth decelerates from 30%+ to below 20%, SaaS valuation multiples contract dramatically.

Fortinet exemplifies the "steady-state" value proposition. Q1 revenue of $1.85 billion (20% YoY), product revenue up 41%, GAAP operating margin of 31%, and non-GAAP EPS of $0.82 (up 41%). Full-year FY2026 guidance raised to $7.71-7.87 billion (approximately 15% growth). Record free cash flow of $1.01 billion demonstrates the cash-flow advantage of hardware+SaaS hybrid models.

Cloudflare's 4.29% surge reflects a different valuation logic — "AI infrastructure" rather than pure security. Its global edge network carries rapidly growing AI workloads, and investors increasingly evaluate it alongside AI infrastructure companies rather than traditional security vendors.

IV. Strategic Depth: Competitive Landscape and Ecosystem Positioning

AI security competition is escalating from feature competition to ecosystem definition battles.

PANW: The "Operating System" Play. Through IBM, Red Hat, and Deutsche Telekom partnerships, PANW is building an open AI security ecosystem. Its core thesis: future enterprise security is not buying a product but connecting to a platform. "Sovereign Cortex" addresses European data sovereignty pain points — under GDPR, NIS2, and DORA, multinationals cannot simply upload security data to US clouds. PANW converts compliance costs into competitive moats by establishing localized AI security operations in each major jurisdiction.

Zscaler: The "Zero Trust Native" Play. Zscaler differentiates by embedding AI security deep within zero-trust architecture. As enterprises shift from perimeter defense to boundary-less access, every user, device, and AI agent becomes a potential attack surface. Zscaler's value proposition: in a world where nobody can be trusted, AI is the only technology capable of continuously assessing risk and dynamically adjusting access policies.

Cloudflare: The "Infrastructure" Play. Cloudflare doesn't sell security products directly — it embeds security into global network infrastructure. When 95% of enterprises deploy AI in mobile apps but 37% lack AI behavior monitoring, Cloudflare's network-layer security becomes "default infrastructure." The advantage is low customer acquisition cost — enterprises gain AI security simply by using Cloudflare's network services.

Fortinet: The "Operational Efficiency" Play. Fortinet's strategy is "trade hardware cost advantage for market share." Proprietary ASIC chips (NP7/SP5) deliver hardware costs far below competitors at equivalent performance, while FortiSOC pushes security operations automation to new heights. Fortinet targets mid-market enterprises with "limited budgets but rigid security needs."

V. Challenges and Concerns: Three Contradictions Facing AI Security

Despite the bright outlook, the four vendors' divergence reveals deep industry contradictions.

Contradiction 1: The AI Black Box Dilemma. AI model decision processes are difficult to explain — a critical weakness in security. When AI security systems misclassify legitimate business traffic as attacks, enterprises cannot understand the rationale, causing operational disruptions. Both PANW and Zscaler are investing in explainable AI, but no perfect solution exists yet.

Contradiction 2: Data Sovereignty vs. Global Operations. PANW's "Sovereign Cortex" addresses European compliance but requires independent AI model training infrastructure in each country/region, significantly increasing operational costs. For resource-constrained smaller vendors, such compliance costs could become market exit barriers.

Contradiction 3: Unsustainable AI Arms Race. Security vendors are pouring increasing AI compute into threat detection, but attackers are also using AI to generate more sophisticated attacks. This "AI vs. AI" arms race could drive costs up for both sides, ultimately squeezing industry margins. Zscaler's 30% crash partly reflects market skepticism about the sustainability of "unlimited AI security R&D investment."

Fortinet faces a specific challenge: while its hardware+SaaS hybrid model generates steady cash flow, it may gradually fall behind in AI-native security architecture evolution. As competitors deploy AI inference to the cloud, Fortinet's ASIC hardware path may lose its cost advantage.

VI. Conclusion: Future Scenarios and Investment Perspective

The simultaneous June 30 movements of four cybersecurity giants mark AI security's entry into a "differentiation phase." PANW's platform expansion, Cloudflare's infrastructure premium, Fortinet's steady monetization, and Zscaler's valuation correction together paint a comprehensive picture of industry transformation.

Investment Perspective:

- Palo Alto Networks (Hold/Overweight): Clear AI security platform strategy; "Sovereign Cortex" opens European enterprise/government markets. The 65% YTD gain reflects market recognition of its valuation framework shift. Key risk: platform integration complexity and intensifying competition.

- Zscaler (Watch): Fundamentals intact but valuation framework under pressure. Monitor whether AI Protect revenue share can consistently improve. If ARR growth stabilizes above 20%, current valuation may offer attractive entry points.

- Cloudflare (Overweight): Unique "AI infrastructure" valuation positioning. AI workload growth on its global edge network is the long-term growth engine.

- Fortinet (Hold): Steady cash flow but limited growth momentum. Suitable for value investors. Monitor FortiSOC market adoption and AI product revenue contribution.

Forward-Looking Outlook:

- Accelerated Consolidation: AI security platforms require massive R&D investment and data accumulation. Expect 3-5 billion-dollar security M&A deals in H2 2026.

- "AI Security Revenue Share" Becomes Core KPI: Investors will demand separate disclosure of AI-related product revenue, not just overall ARR growth.

- Behavioral Analytics Replaces Rule Engines: By 2027, AI behavior anomaly detection products will capture over 40% of enterprise security spending.

- Sovereign Compliance Spurs Regional Leaders: Data sovereignty requirements in Europe, Middle East, and Asia-Pacific will create regional AI security leaders rather than a single global dominant player.

Why it Matters

AI security is becoming the most certain growth track in tech for 2026. Gartner projects global information security spending of $244.2 billion in 2026 (+13.3% YoY), with the AI cybersecurity market expected to reach $133 billion by 2030 at a 29% CAGR. The divergence among the four giants signals that AI agent proliferation (projected to exceed 50% enterprise deployment by end-2026) is creating entirely new attack surfaces that rule-based defenses cannot address. Data sovereignty compliance (GDPR/NIS2/DORA) is further accelerating regional security platform growth. For CIOs and CTOs, AI security is no longer optional but foundational to AI strategy. For investors, industry consolidation and valuation framework shifts will create significant alpha opportunities.

DECISION

- For enterprise security buyers: Prioritize AI behavioral analytics capabilities over threat database size. Require vendors to provide concrete AI agent behavior monitoring solutions.

- For CIOs/CTOs: Reclassify AI security budgets from IT cost centers to AI strategic infrastructure investments, targeting 15-20% of total IT budget.

- For multinational enterprises: Immediately initiate data sovereignty compliance audits. Prioritize vendors with localized AI security operations in target markets (e.g., PANW's Sovereign Cortex).

- For investors: Focus on "AI security revenue share" as a new KPI rather than overall ARR growth alone. Overweight platform-ecosystem players with global compliance footprints.

PREDICT

- Within 12 months: At least 3 billion-dollar AI security M&A deals will occur as consolidation accelerates. If Zscaler stabilizes ARR growth above 20%, its stock could recover to 70% of pre-crash levels.

- Within 2 years: AI behavior anomaly detection products will capture over 40% of enterprise security spending, while traditional signature-based tools shrink below 30% market share. PANW's Cortex platform is likely to become the de facto "security operating system" standard.

- Within 3 years: Regional AI security leaders will emerge in Europe, Asia-Pacific, and the Middle East, shifting the global cybersecurity market from "US-dominated" to "multi-polar." Data sovereignty compliance costs will represent 15-20% of security vendor operating costs.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)