I. Event Recap: Samsung Foundry Rise and Memory Price Surge Converge

July 3, 2026, brought a wave of seismic news for the global semiconductor industry, with the density and interconnectedness of these events signaling a structural inflection point.

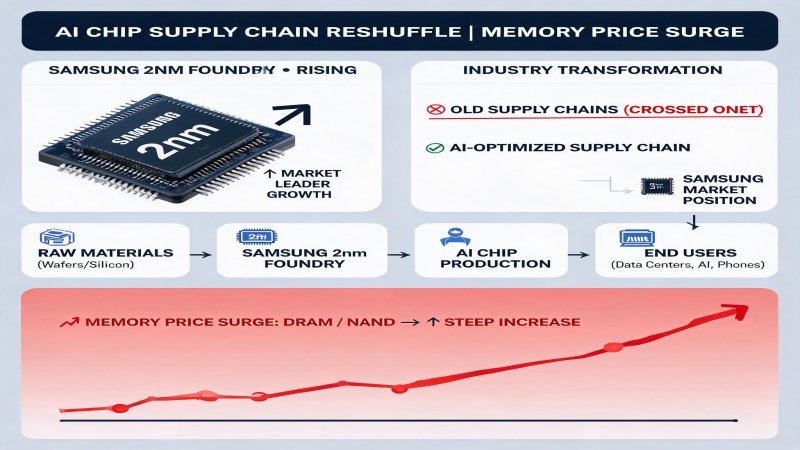

First, Korean memory giant Samsung Electronics confirmed plans to raise general DRAM average selling prices by up to 20% quarter-over-quarter in Q3 2026. According to ZDNET Korea, Samsung began price negotiations with customers on July 3 with a notably aggressive stance. The primary driver is the relentless AI infrastructure investment by global tech giants, creating shortages across server DRAM, high-bandwidth memory (HBM), and low-power DRAM (LPDDR) used for AI inference. The news triggered a chip stock rally in Korea: Samsung Electronics surged over 8%, SK Hynix jumped over 10%, and the KOSPI index closed up 5.76%.

On the same day, Samsung's foundry business received major boosts. Korean media reported that Meta is partnering with Samsung Foundry to design and produce next-generation ASICs valued at over 10 trillion KRW (~$7.4 billion). Meta's first two generations of MTIA AI accelerators were manufactured by TSMC, but the third generation has shifted to Samsung, targeting mass production at hundreds of thousands of units using 2nm process technology. Even more notably, AI startup Anthropic has also initiated plans for custom AI chips and is negotiating with Samsung for 2nm foundry and advanced packaging services. If both projects materialize, Samsung Foundry's backlog could approach 50 trillion KRW.

Additionally, the Kechuang Board Daily reported on July 3 that Samsung Foundry's 4nm process capacity is essentially sold out, with even 2027 capacity fully booked, while some 8nm lines are operating near full utilization. Samsung has been forced to prioritize existing customers and selectively accept new orders.

Meanwhile, AMD and Intel also confirmed price increases between July 3-4. AMD notified key AIB partners of approximately 10% hikes for GPU core and GDDR bundle shipments starting July, while Intel raised prices on select consumer and server CPUs, with datacenter products seeing increases of hundreds to over a thousand dollars.

The common thread is unmistakable: exploding AI compute demand is fundamentally altering semiconductor industry supply-demand dynamics and profit distribution.

II. Technical Depth: How 2nm and Advanced Packaging Reshape AI Chip Competition

Understanding Samsung's strategic turning point requires deep analysis of 2nm process technology and advanced packaging.

2nm represents the industry's most advanced chip manufacturing process. Compared to 3nm, it offers higher transistor density and power efficiency—critical for AI accelerators where compute and power are paramount. TSMC holds a first-mover advantage in 2nm, but its capacity is extremely tight, with Apple, NVIDIA, and others occupying most available slots. This creates a strategic window for Samsung.

Meta's selection of Samsung's 2nm process for MTIA Gen 3 represents not only validation of Samsung's technical capabilities but also an inevitable supply chain diversification move. Meta plans to build 5 gigawatts of datacenter capacity by end-2030, with new chip generations every six months. This aggressive cadence exceeds Meta's internal chip design team's capacity, necessitating a joint development framework with Samsung's System LSI division.

Anthropic's situation mirrors Meta's. As OpenAI's primary competitor, Anthropic is planning approximately 1 gigawatt of proprietary AI datacenter capacity, representing roughly $50 billion in total investment, with about half earmarked for chips. Anthropic recently hired Clive Chan, a core engineer from OpenAI's custom chip project, signaling serious intent. Choosing Samsung over TSMC reflects both TSMC's capacity constraints and Samsung's unique vertical integration across memory, foundry, and advanced packaging.

Advanced packaging is another critical variable. AI chips require tight integration between compute dies and HBM high-speed memory. Advanced packaging shortens the distance between processor and memory, improving data transfer speeds and energy efficiency. Samsung's leadership in HBM4, combined with 2nm foundry and advanced packaging capabilities, makes it an ideal partner for AI chip customers.

Four-Vendor Competitive Matrix:

| Dimension | TSMC | Samsung | Intel | SMIC |

| Leading Mass Production Node | 2nm (N2) | 2nm (SF2) | 18A/14A | 7nm |

| 2nm Customer Count | 5+ (Apple/NVIDIA) | 2+ (Meta/Anthropic) | Mostly internal | None |

| Advanced Packaging | CoWoS/SoIC | I-Cube/H-Cube | Foveros | Limited |

| HBM Supply Capability | No | HBM4 in production | No | No |

| Q2 2026 Capacity Utilization | >95% | 4nm sold out / 8nm full | Underutilized | Underutilized |

| AI Foundry Revenue Mix | ~35% | Rapidly growing | <5% | <1% |

III. Financial Logic: How the Price Surge Transmits Through Value Chains

From a financial perspective, this semiconductor price cycle exhibits distinct structural characteristics.

Samsung's DRAM ASP rose approximately 90% QoQ in Q1 2026, around 50-60% in Q2, and targets roughly 20% in Q3. While the pace is moderating, cumulative increases are extraordinary. More importantly, long-term agreement (LTA) ratios are steadily rising. Micron disclosed last month it has signed 16 LTAs with customers that constrain purchase volumes and set price floors guaranteeing high margins. This indicates consensus has formed around sustained tight memory supply.

Samsung Foundry's financial inflection point is equally significant. The division had been loss-making due to underutilization, but AI demand has rapidly filled 4nm and 8nm lines. A Korean industry official revealed Samsung Foundry's backlog has reached approximately 50 trillion KRW, with quarterly operating profitability expected in Q4 2026—its first since 2022.

AMD and Intel's price increases confirm cost transmission mechanisms. AMD raised GPU bundle prices twice within six months; Intel's datacenter CPUs rose by hundreds of dollars. This demonstrates that memory cost inflation and advanced process capacity tightness are transmitting downstream through the value chain, ultimately borne by end users.

From an ROI perspective, Samsung's approximately $25 billion Taylor, Texas fab investment—previously questioned due to underutilization—could see its payback period dramatically shortened with Meta and Anthropic's influx.

IV. Strategic Depth: From Isolated Events to Structural Industry Transformation

Placing July 3's events in broader industry context reveals three mutually reinforcing structural trends.

Trend 1: Accelerating Custom AI Chip Proliferation. From Google TPU, Amazon Trainium, and Microsoft Maia, to OpenAI's Jalapeno chip with Broadcom, to Meta's MTIA and Anthropic's custom plans, tech giants are extending competition from models to underlying hardware. Our analysis shows 7 of the top 10 global cloud providers have initiated or completed custom AI chip programs. The direct beneficiaries are foundries with available advanced capacity—currently Samsung.

Trend 2: Memory-Compute Convergence Becoming Mainstream. AI workloads' memory bandwidth demands are growing exponentially, making traditional discrete architectures performance bottlenecks. Samsung's simultaneous capabilities in HBM4, 2nm logic, and advanced packaging amplify this vertical integration advantage in the AI era. TSMC leads in logic but lacks memory; SK Hynix leads in HBM but has no foundry business.

Trend 3: Supply Chain Diversification Shifting from Optional to Mandatory. Geopolitical risk, natural disaster risk (TSMC's historical earthquake and water constraints), and simple bargaining power drive all major chip buyers to seek 'second sources.' Samsung's 2nm process winning Meta and Anthropic directly embodies this trend.

V. Challenges and Risks: Yield Uncertainties and Competitive Dynamics

Despite bright prospects, Samsung's foundry resurgence faces multiple challenges.

First, 2nm yield remains a critical question. While Samsung has invested heavily in GAA (Gate-All-Around) transistor technology, its 3nm yield history was imperfect. Customers choosing Samsung 2nm assume yields reach economically viable levels. If yield ramps slower than expected, Meta and Anthropic may be forced back to TSMC.

Second, TSMC's countermeasures. Facing customer defection risks, TSMC is unlikely to remain passive. Potential responses include accelerating 2nm capacity expansion, offering more competitive pricing, or deepening customer ties through 'virtual IDM' models. TSMC's 2026 capex is expected to exceed $40 billion, mostly directed at 2nm and below.

Third, demand-side cyclical risk. Current AI chip demand appears limitless, but the semiconductor industry has never escaped cyclicality. If AI training demand slows in 2027-2028 while capacity expansions concentrate their release, severe oversupply could result. Kioxia CEO Hiroo Ota stated he 'sees no signs of datacenter demand weakening,' but market consensus often precedes cycle inflection points.

Finally, geopolitical risk. US semiconductor export controls to China continue tightening. While directly impacting equipment (ASML), any technology restrictions involving China could indirectly affect Samsung's global layout. Samsung operates substantial NAND flash capacity in Xi'an, China, making it vulnerable to geopolitical shocks.

VI. Conclusion: Investment Perspective and Forward-Looking Judgments

Synthesizing the above analysis, we believe July 3's events mark the global AI chip supply chain entering a new restructuring phase.

For investors, Samsung Electronics presents significant revaluation upside. Markets currently price its foundry business pessimistically, embedding continued losses. But if Q4 delivers operating profit as expected and 2nm customers keep growing, valuation models for Samsung's semiconductor business will fundamentally change. We conservatively estimate Samsung Foundry's valuation could rise from near-zero to $20-30 billion.

For industry observers, three key metrics demand attention: Samsung's 2nm yield data (expected Q3 disclosure), Meta MTIA Gen 3's actual performance (expected H1 2027 production), and DRAM LTA signings and pricing terms.

For enterprise decision-makers, this price surge and capacity tightness will likely persist through at least H1 2027. We recommend completing strategic inventory buildup before Q3 prices take effect, and actively evaluating long-term agreements with Samsung, SK Hynix, and others. Simultaneously, translate supply chain diversification from rhetoric to action, establishing effective alternatives to TSMC in advanced processes.

From a longer-term perspective, AI chip industry competition is evolving from a TSMC-NVIDIA duopoly toward multipolarity. Samsung, Intel, and even China's SMIC are seeking breakthroughs. Over the next three to five years, manufacturers mastering advanced logic, memory, and packaging simultaneously will possess the greatest strategic initiative. On this dimension, Samsung is currently the only global player with complete capabilities—provided it can prove itself in the 2nm yield battle.

Why it Matters

Exploding AI compute demand is reshaping the global semiconductor landscape. As the only IDM with leading memory, foundry, and advanced packaging capabilities, Samsung is becoming the biggest beneficiary of tech giants' custom chip strategies. Meta's six-month chip iteration cycle and Anthropic's planned 1-gigawatt datacenter will directly boost Samsung's advanced process market share. Meanwhile, broad DRAM and CPU/GPU price hikes show AI-driven supply tightness has spread upstream to end products, with pricing power structurally shifting upward.

DECISION

- CIOs/CTOs: Evaluate datacenter storage procurement strategies and consider LTAs with Samsung and SK Hynix to lock in prices. 2. Investors: Monitor Samsung Foundry's break-even inflection point; Q4 operational profitability could trigger re-rating. 3. Supply chain managers: Include Samsung in advanced process second-source assessments to reduce sole reliance on TSMC. 4. Enterprise procurement: Complete strategic DRAM and server CPU inventory buildup before Q3 price hikes take effect.

PREDICT

- Q3-Q4 2026: Samsung Foundry will post its first quarterly operating profit since 2022, with 2nm yield reaching acceptable levels. 2. End of 2026: Meta's 3rd-gen MTIA and Anthropic's first custom chip enter tape-out, with Samsung's advanced packaging orders up over 100% YoY. 3. H1 2027: Cumulative DRAM price increases will reach 50-70%, pushing Samsung's semiconductor division operating margin above 25%. 4. 2027: At least three of the top five global cloud providers will have custom AI chips, with Samsung's foundry customer count doubling.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)