Chapter 1: Event Overview

In the early hours of July 13, 2026, OpenAI Codex engineering lead Thibaut Sottioux announced three updates on X: the temporary removal of the 5-hour usage limit for all Plus, Business, and Pro plans; inference optimization for GPT-5.6 Sol with an estimated 10% quota increase; and the milestone of 6 million active Codex and ChatGPT Work users, accompanied by an immediate quota reset. This sudden quota relaxation was not an isolated product update but a direct signal of the intensifying competition in the AI coding assistant market.

Earlier the same day, Anthropic announced a further 7-day extension of Claude Fable 5 access across all paid tiers until July 19. This marked Anthropic's third delay of Fable 5's paid transition, previously pushed from July 7 to July 12, and now to July 19. Each extension served as both user appeasement and suspense—users had no certainty about continued access.

The quota war was triggered by massive user backlash. Fable 5 priced at $10 per million input tokens and $50 per million output tokens meant even simple queries could rapidly deplete quotas. More critically, security policy flaws caused normal coding and debugging tasks to be frequently flagged as high-risk, downgrading processing to Opus 4.8—users paid for Fable but often received Opus. Widespread sharing of high credit bills and subscription cancellation threats pressured Anthropic to act.

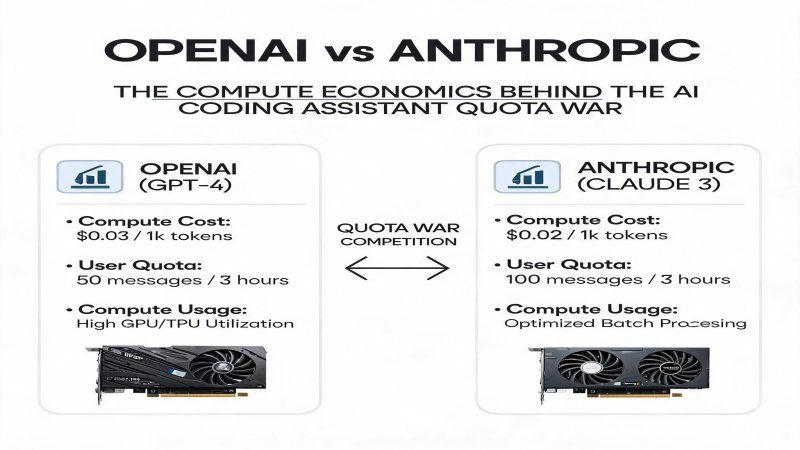

OpenAI's counter was precise and aggressive. Sol pricing at $5 input and $30 output per million tokens is half of Fable 5. On SWE-Bench Verified, Sol scored 88.8% in standard mode versus Fable 5's 88.0%, reaching 91.9% in Ultra mode. Matching capability at half price is a classic undercutting strategy. But OpenAI went further by eliminating the 5-hour rolling limit entirely, allowing users to burn through weekly quotas in hours.

Chapter 2: Technical Depth

Understanding this quota war requires examining the technical architecture differences. OpenAI's GPT-5.6 Sol employs an improved MoE (Mixture of Experts) architecture with an estimated 1.8 trillion total parameters but only approximately 320 billion activated per forward pass. This sparse activation design reduces inference costs by roughly 40% compared to dense models, providing the core technical foundation for Sol's pricing advantage.

Anthropic's Claude Fable 5 follows a fundamentally different approach based on Constitutional AI, using self-criticism and revision mechanisms to enhance safety and reliability. Fable 5's context window reaches 500K tokens, 2.5x Sol's approximately 200K tokens, providing natural advantages for large codebase processing. However, long context implies higher inference costs—Fable 5's cost for 100K token input is approximately 1.8x Sol's.

On SWE-Bench Verified, the standard mode gap is minimal (88.8% vs 88.0%), but Sol's Ultra mode at 91.9% demonstrates OpenAI's deep optimization investment. Core capabilities in code generation, debugging, and refactoring have converged; true differentiation lies in inference efficiency and cost structure.

OpenAI's optimizations include dynamic batching, speculative decoding, and customized CUDA kernels, reducing Sol's per-token latency to roughly 75% of Fable 5's while increasing throughput by approximately 35%. Anthropic's substantial safety investments haven't been matched by equivalent inference efficiency optimization, directly reflected in higher pricing.

Chapter 3: Financial Logic

Financially, this quota war exposes a core tension in AI inference: the trade-off between gross margin and market share. Analyst Benedict Evans notes current AI inference gross margins range from 40% to 50%. OpenAI's removal of the 5-hour limit and free quota resets essentially exchange short-term profit for market share.

For a heavy developer consuming 500M input and 100M output tokens monthly, Fable 5 costs $6,000 while Sol costs $2,800. For enterprise clients with tens of thousands of developers, annual cost differences reach tens of millions. This price sensitivity is amplified by tightening macroeconomic conditions.

Anthropic's dilemma stems from its cost structure. Fable 5's high safety standards and long-context design mean higher computational overhead. Estimated single-inference costs are approximately 60% higher than Sol's. Pricing at Sol's level would compress gross margins from approximately 45% to below 15%, unsustainable for a heavily loss-making startup.

OpenAI enjoys scale advantages. Its $122 billion funding round and $85.2 billion valuation enable longer subsidy wars. Deep Microsoft Azure collaboration provides priority GPU supply and lower compute costs. Industry estimates suggest OpenAI's inference costs are 20-30% lower than Anthropic's, enabling aggressive pricing.

Chapter 4: Strategic Depth

This quota war is fundamentally a customer acquisition battle in the AI coding assistant market. With user stickiness still developing—approximately 35% of developers use multiple AI coding tools—price and convenience become critical levers.

The competitive landscape features OpenAI, Anthropic, Google, and xAI. Google Gemini Code Assist holds approximately 18% enterprise market share through Google Cloud and Workspace integration. xAI's Grok 4.5, though technically inferior, leverages Musk's brand and X platform traffic for rapid independent developer growth.

OpenAI's strategy builds ecosystem lock-in through Codex. Six million active users is a critical milestone—when enough developers integrate Codex into daily workflows, switching costs rise significantly. The Banked Reset feature increases stickiness while preventing resource waste.

Anthropic's counter focuses on differentiation. Fable 5's safety, long-context, and complex reasoning advantages attract financial and healthcare verticals with strict regulatory requirements. Anthropic actively promotes Claude Code's Agentic capabilities for multi-step autonomous tasks, a direction Sol hasn't fully matched.

Chapter 5: Challenges and Risks

What is the endgame? Evans offers a pessimistic analogy: over 20 years, cellular data traffic grew orders of magnitude to trillion-dollar annual revenue and $200 billion CapEx, yet operator stocks barely rose. All value was captured upstream. By this logic, once AI compute scarcity eases, foundation models trend toward low-margin commodity infrastructure.

For OpenAI, short-term risk is subsidy war financial drain. Despite ample funding, over $1 trillion in data center CapEx is in the pipeline with uncertain supply-demand equilibrium. A subsidy war lasting over a year could force dilutive fundraising.

For Anthropic, risks are more immediate. Lower valuation and limited funding reserves mean failure to maintain user scale during price wars could trigger a growth stagnation and fundraising difficulty cycle. The safety-first strategy wins premium clients but limits mass-market expansion.

The broader industry risk is compute bottlenecks. Evans notes that 2026 H1 compute scarcity stems from software development alone achieving product-market fit—a relatively small domain. If a consumer scenario serving hundreds of millions of DAU achieves similar fit, current global infrastructure cannot support it at any price.

Chapter 6: Conclusion

For technology decision-makers, this is a window to evaluate and lock in AI coding tool suppliers. A multi-vendor strategy avoids over-reliance on single models: Sol for daily coding and rapid iteration (optimal cost-effectiveness), Fable 5 for security-sensitive and long-context tasks (broader capability coverage), while monitoring Google Gemini Code Assist's enterprise integration progress.

For investors, OpenAI's aggressive subsidies will short-term suppress industry margins but long-term build ecosystem moats. Anthropic's challenge is maintaining technical differentiation while improving cost structure. Monitor breakthroughs in inference efficiency optimization and vertical solution deployment.

For developers, the current quota war is a红利期. Maximize free/low-quota policies from both vendors while building cross-platform workflow capabilities. Beware vendor lock-in risks—avoid deep binding of core codebases to single-tool proprietary formats. Over the next 6-12 months, as compute supply improves and price wars subside, the market will return to rational pricing where tools with cost efficiency and multi-scenario coverage will prevail.

Why it Matters

The AI coding assistant market is transitioning from capability to price competition. OpenAI's MoE architecture and Azure compute advantages yield 20-30% lower inference costs than Anthropic, enabling sustainable price wars. Anthropic's high safety standards win premium clients but a 60% inference cost premium creates structural disadvantage in mass markets. This competition's outcome will determine the developer tools landscape over the next 18 months.

DECISION

Tech decision-makers: Adopt multi-vendor strategy—Sol for daily coding (cost-optimal), Fable 5 for security-sensitive tasks (broader coverage).

Developers: Exploit current free/low-quota红利期, build cross-platform workflows, avoid vendor lock-in.

Investors: Monitor OpenAI subsidy burn rate and Anthropic cost structure improvements; market returns to rational pricing in 6-12 months.

PREDICT

Next 3 months: Anthropic will be forced to launch Fable 5 Lite or reduce pricing to stem user churn.

Next 6 months: Google will leverage Gemini Code Assist's enterprise integration to capture 15%+ share among Fortune 500.

Next 12 months: The AI coding assistant market will complete its first shakeout, with no more than 4 surviving players.

Next 18 months: Inference costs will drop 50%+, and current price wars will be replaced by standardized subscription models.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)