I. Event Recap

On July 6, 2026, the global semiconductor supply chain witnessed a wave of concentrated price and expectation adjustments, signaling that the AI-driven semiconductor supercycle has entered a full-scale price surge phase. On that single day, Intel officially confirmed CPU price hikes, with some products increasing by thousands of dollars; AMD publicly advised enterprises to optimize memory allocation to cope with the AI server super price cycle, with Q2 DRAM contract prices rising nearly 60% quarter-over-quarter; the Semiconductor Equipment Association of Japan (SEAJ) sharply raised its FY2026 Japanese semiconductor equipment sales forecast to 6.55 trillion yen, representing 26% year-over-year growth; Goldman Sachs simultaneously raised its TSMC ADR price target to $600, while Citigroup lifted TSMC's target price to NT$38,005; Samsung's foundry business, meanwhile, reported its first monthly profit in three years.

These events were not isolated occurrences but rather simultaneous projections of exploding AI computing demand across every link of the supply chain. From upstream equipment to midstream manufacturing and downstream end products, the entire semiconductor ecosystem is being redefined by AI. SEAJ's forecast report shows that driven by investment enthusiasm for AI server advanced logic chips, combined with massive DRAM production line expansion centered on HBM, Japanese semiconductor equipment sales will exceed 6 trillion yen for the first time, marking a third consecutive year of record highs. Even more notably, SEAJ sharply raised its FY2027 forecast from 5.6104 trillion yen to 7.4017 trillion yen, demonstrating strong confidence in long-term AI infrastructure investment.

On the timeline, Q2 2026 became a critical inflection point. Samsung's foundry had accumulated losses of nearly 14 trillion won (approximately 61.6 billion yuan) since 2023, but finally achieved monthly profitability in June. Intel and AMD's price increase announcements further confirmed the severity of supply-demand imbalances. Server configurations that previously cost $25,000 now quote at $35,000-$40,000, with single-server costs rising over 100,000 yuan. For TSMC, its CoWoS advanced packaging capacity remains severely constrained, with order backlogs extending into 2027, making it impossible to ease the demand-supply gap in the near term.

II. Technical Depth

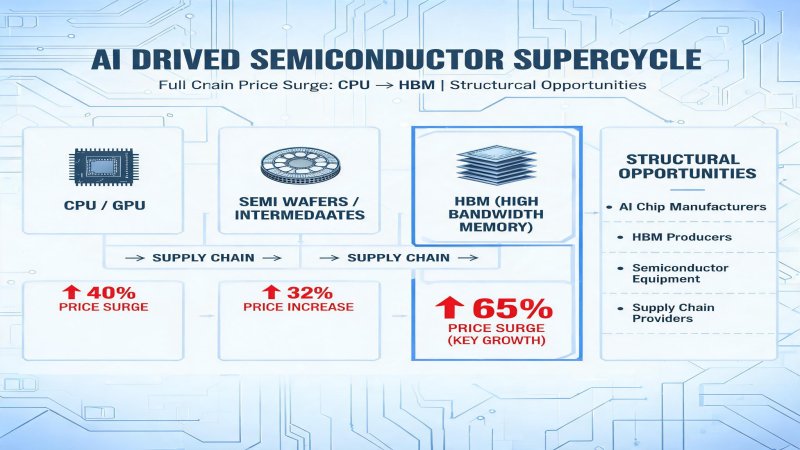

The technical roots of this price surge lie in the disruptive demand that AI large model training and inference place on computing infrastructure. Traditional data centers were CPU-centric, while the AI era is GPU/ASIC cluster-centric, creating unprecedented resource competition for high-bandwidth memory (HBM), advanced packaging (CoWoS), and high-end CPUs.

HBM technology is one of the core bottlenecks driving this price cycle. HBM3E and the upcoming HBM4 increase memory bandwidth to multiple TB per second, becoming essential for AI training clusters. Samsung's DS division memory business has made positive progress on HBM4, securing large base die orders that have become an important driver in turning around its foundry business. Meanwhile, comprehensive DRAM production line expansion has pushed up overall memory prices, with AMD noting that Q2 DRAM contract prices rose nearly 60% quarter-over-quarter, placing severe cost pressure on enterprise customers.

In advanced packaging, TSMC's CoWoS technology integrates logic chips with HBM in a 2.5D configuration, now the standard for high-end AI chips. However, CoWoS capacity expansion significantly lags demand growth, leading to extended delivery cycles for major customers including NVIDIA and AMD. TSMC is expanding production in both Taiwan and Arizona, but equipment lead times of 12-18 months create noticeable delays in capacity ramp.

CPU price increases reflect another dimension of technical substitution logic. Intel Xeon and AMD EPYC processors remain indispensable for AI inference and data preprocessing. AI server configurations have evolved from traditional 1:1 CPU-to-GPU ratios to 1:4 or even 1:8, but absolute CPU demand continues rising. When GPU supply is constrained, customers tend to stack more CPUs and memory in available configurations, further exacerbating CPU and DRAM supply-demand imbalances.

| Vendor | Core Product | Process/Tech | AI Revenue | Key Bottleneck ||--------|-------------|--------------|------------|----------------|| TSMC | Foundry/CoWoS | 3nm/2nm | 35%+ of revenue | CoWoS capacity shortage || Samsung | Foundry/HBM | 4nm improved/HBM4 | DS turning around | Advanced process yield || Intel | CPU/Foundry svc | Intel 18A | Data center growth | Process catch-up || AMD | CPU/GPU | 4nm/3nm | 60%+ data center | Memory cost pass-through |

III. Financial Logic

From a financial perspective, this supercycle displays classic 'volume and price rising together' characteristics. As an industry bellwether, TSMC's price target was raised by Goldman Sachs to $600 because AI-related revenue already exceeds 35% of total revenue, and gross margins remain above 55% due to advanced process pricing power. Citigroup's even more aggressive NT$38,005 target implies the market is beginning to value TSMC as an 'AI era computing infrastructure operator' rather than a traditional manufacturer.

Samsung Electronics' financial inflection point is equally noteworthy. Its foundry and system LSI businesses had accumulated losses of nearly 14 trillion won since 2023. While June's monthly profit does not indicate quarterly turnaround, it confirms an improving operational trend. On the customer front, Tesla's AI5/AI6 and LPU foundry contracts, along with partial order transfers from NVIDIA, provide valuable advanced process capacity utilization channels. If HBM4 achieves smooth mass production in H2, Samsung's DS division could achieve quarterly profitability in Q3 2026, with full-year operating profit market expectations around 300 trillion won (approximately $200 billion), far exceeding 2025's 43.6 trillion won.

On the equipment side, SEAJ raised its FY2026 sales forecast to 6.55 trillion yen (26% YoY growth), driven by dual momentum from AI server chip investment and HBM production line expansion. Tokyo Electron, Screen Holdings, and Advantest are direct beneficiaries. Notably, equipment sales typically lead foundry revenue by 3-6 months, and the FY2027 forecast was further raised to 7.4017 trillion yen, indicating this capex cycle will extend at least through mid-2027.

Cost analysis shows that in AI server BOM costs, GPU/ASIC accounts for roughly 60%, HBM about 20%, and CPU/motherboard/other components about 20%. When HBM and CPU prices rise simultaneously, total system cost increases are more dramatic. Configurations that previously cost $25,000 now reach $35,000-$40,000, a 40-60% increase far exceeding single-component price rises, demonstrating a 'cost stacking effect.' For cloud service providers and AI companies, this means capex plans must be substantially raised, or they must seek self-developed chips to reduce costs.

IV. Strategic Depth

This semiconductor supercycle is reshaping the competitive landscape of the global technology industry. From a strategic matrix perspective, major players show clear positioning and strategy divergence.

TSMC maintains its 'neutral foundry' strategy, becoming the biggest 'shovel seller' of the AI era. Its customers include nearly all top chip design companies: NVIDIA, AMD, Apple, Qualcomm, Amazon, and others. The deep meaning behind Goldman Sachs' $600 price target is that TSMC's pricing power is evolving from 'process leadership' to 'computing infrastructure monopoly.' As long as AI model parameters continue expanding, demand for advanced processes and packaging will not weaken.

Samsung Electronics pursues a 'memory + foundry' dual-wheel drive strategy, with HBM4 and 4nm yield improvement as its two main levers. Securing Tesla's AI6 chip contract represents a key breakthrough for its foundry business, but challenging TSMC remains a distant goal. Samsung's strategy is to secure a 'second supplier' position in the AI chip foundry market through aggressive pricing and capacity expansion.

Intel is struggling through its 'IDM 2.0' transformation. CPU price hikes may improve profitability in the short term, but in the long run, Intel must prove itself in advanced processes (Intel 18A) while its foundry business (IFS) needs to win more external customers. Excessive price increases could accelerate customer migration to AMD EPYC.

AMD is one of the beneficiaries of this cycle, with EPYC processors and Instinct accelerators gaining share in the AI server market. However, AMD also faces upstream cost pressure, hence its advice to customers to 'optimize memory configuration based on actual workloads'—practical customer guidance that also reflects AMD's helplessness in the face of memory price surges.

Cloud providers' self-developed chip trend (Amazon Trainium, Google TPU) represents a structural challenge to traditional semiconductor supply chains. While they cannot replace NVIDIA GPUs in the short term, they have demonstrated cost advantages in inference workloads. AWS's decision to raise Trainium 3 shipment expectations by 20-30% indicates self-developed chips have moved from 'experimental projects' to 'large-scale deployment.'

| Vendor | Strategic Position | Core Advantage | Main Risk | 2026 Key Metric ||--------|-------------------|----------------|-----------|-----------------|| TSMC | Neutral foundry leader | Process + packaging lead | Geopolitics/over-concentration | 2nm mass production || Samsung | Memory + foundry dual | HBM vertical integration | Advanced process yield | Foundry quarterly profit || Intel | IDM 2.0 transformation | x86 ecosystem/US gov support | Process catch-up failure | 18A customer adoption || AMD | Data center full stack | CPU + GPU combination | Upstream cost pass-through | Data center revenue share |

V. Challenges and Concerns

Despite the bright supercycle outlook, the industry faces multiple challenges.

First, geopolitical risk. US-China tech competition continues escalating, and US export controls on chips to China may tighten further, affecting equipment, materials, and EDA tool flows. Microsoft's Azure China layoffs indicate multinational cloud providers have begun rebalancing between geopolitics and market demand. If controls escalate, the global semiconductor supply chain could face new fracture points.

Second, capex cyclical risk. SEAJ forecasts record equipment sales for 2026-2027, but historical experience shows semiconductor capex is highly cyclical. Once AI model training demand slows, or inference efficiency improves substantially (through model compression, quantization advances), excess capacity could trigger rapid price declines. The frenzied expansion of 2025-2026 may translate into overcapacity in 2027-2028.

Third, technology route uncertainty. Current AI chips are dominated by NVIDIA GPUs, but ASICs (Amazon Trainium, Google TPU), new memory-compute integrated architectures, and potential long-term quantum computing alternatives all introduce uncertainty into traditional semiconductor investments. If a leapfrog technological shift occurs, current massive investments in CMOS and HBM could face impairment risks.

Fourth, cost transmission limits. Server configurations have risen from $25,000 to $35,000-$40,000, and some SME customers may delay or cancel AI infrastructure investments. If AI applications' commercial returns cannot cover rapidly rising computing costs, demand-side 'price suppression' effects could interrupt the price cycle's continuation.

VI. Conclusion

From an investment perspective, this AI-driven semiconductor supercycle is in the 'volume and price rising together' main upswing phase, and the supply-demand tightness is unlikely to fundamentally change in the short term (6-12 months). TSMC, Samsung's HBM business, and Japanese equipment makers are the highest-certainty beneficiaries. AMD and Intel's competition in data center CPUs will continue, but upstream cost pressure may erode some margins.

Forward-looking judgments:

- In H2 2026, TSMC's CoWoS capacity expansion will partially ease packaging bottlenecks, but 2nm wafer capacity will become the new constraint.

- Samsung Electronics is likely to achieve quarterly foundry profitability in Q3 2026, with full-year DS division operating profit improving dramatically, though challenging TSMC remains a long-term endeavor.

- If Intel's 18A process achieves smooth tape-out in H2, it will lay the foundation for regaining process leadership in 2027; conversely, if delayed again, its data center market share could accelerate erosion.

- Rising AI server costs will accelerate cloud providers' self-developed chip investments, with Amazon Trainium, Google TPU, and Microsoft Maia potentially capturing 20-30% of the inference market by 2027.

For CIOs and CTOs, the key decision in the current environment is how to optimize TCO (total cost of ownership) for AI infrastructure amid rapidly rising computing costs. AMD's advice—to precisely configure memory based on actual workloads—is a pragmatic starting point, but longer-term strategies should include evaluating cloud providers' self-developed chips, considering hybrid cloud deployment to diversify supplier risk, and closely monitoring AI model efficiency improvements' medium-to-long-term impact on computing demand.

Why it Matters

This price surge is not a short-term fluctuation of a single product but a simultaneous mapping of structurally explosive AI computing demand across the entire semiconductor supply chain. From HBM, CPU, GPU to foundry and packaging testing, all segments are experiencing supply shortages simultaneously—rare in semiconductor history. For CIOs/CTOs, this means AI infrastructure TCO will continue rising for 6-12 months, requiring reassessment of procurement strategies. For investors, TSMC, Samsung HBM, and Japanese equipment makers offer highest certainty, but vigilance is needed for potential capex cyclical correction after 2027.

DECISION

【CIO/CTO Recommendations】

- Short-term (0-6 months): Precisely configure memory and CPU based on actual AI workloads; lock in 6-12 month price agreements with suppliers to hedge further increases.

- Medium-term (6-12 months): Evaluate cloud providers' self-developed chips (AWS Trainium, Google TPU) for inference workloads; consider hybrid deployment to reduce NVIDIA GPU dependency.

- Long-term (12+ months): Establish dynamic AI infrastructure TCO monitoring; closely track model compression and quantization advances.

【Investor Recommendations】

- Overweight TSMC and Tokyo Electron, benefiting from pricing power in tight supply and capex upcycle.

- Monitor Samsung Electronics DS division profit inflection; HBM4 mass production progress is the key catalyst.

- Remain cautiously optimistic on Intel; 18A process tape-out results are the critical variable for 2027 competitive position.

PREDICT

【3 months】TSMC CoWoS capacity utilization remains 100%+, 2nm wafers begin trial production, foundry prices rise another 5-10%.

【6 months】Samsung HBM4 mass production begins, DS division achieves quarterly profitability in Q3, full-year operating profit expectations raised to 350 trillion won.

【12 months】Cloud providers' self-developed AI chips (Trainium/TPU/Maia) collectively exceed 15% inference market share, prompting NVIDIA to launch lower-cost inference-specific GPUs.

【18 months】If AI model parameter growth slows, semiconductor equipment orders may decline quarter-over-quarter, industry enters 'post-supercycle' adjustment phase.

Get 3-5 key AI infrastructure signals weekly →

💬 Comments (0)